You might also like

- Report of Al Capone for the Bureau of Internal RevenueFrom EverandReport of Al Capone for the Bureau of Internal RevenueNo ratings yet

- Rico Conspiracy Law and the Pinkerton Doctrine: Judicial Fusing Symmetry of the Pinkerton Doctrine to Rico Conspiracy Through Mediate CausationFrom EverandRico Conspiracy Law and the Pinkerton Doctrine: Judicial Fusing Symmetry of the Pinkerton Doctrine to Rico Conspiracy Through Mediate CausationNo ratings yet

- Surface Transit, Inc. v. Saxe, Bacon & O'shea, in Re Allowances in Estate of Third Avenue Transit Corporation, Debtor, 266 F.2d 862, 2d Cir. (1959)Document8 pagesSurface Transit, Inc. v. Saxe, Bacon & O'shea, in Re Allowances in Estate of Third Avenue Transit Corporation, Debtor, 266 F.2d 862, 2d Cir. (1959)Scribd Government DocsNo ratings yet

- Consummation Order and Final Decree Penn Central BankruptcyDocument52 pagesConsummation Order and Final Decree Penn Central BankruptcyJanetLindenmuthNo ratings yet

- Ohio Bell Tel. Co. v. Public Utilities Comm'n., 301 U.S. 292 (1937)Document11 pagesOhio Bell Tel. Co. v. Public Utilities Comm'n., 301 U.S. 292 (1937)Scribd Government DocsNo ratings yet

- Competitive Impact StatementDocument64 pagesCompetitive Impact StatementlegalmattersNo ratings yet

- Ultra Mares V Touche vT08Document11 pagesUltra Mares V Touche vT08Steve DarociNo ratings yet

- United States District Court Northern District of Texas Lubbock DivisionDocument5 pagesUnited States District Court Northern District of Texas Lubbock DivisionlegalmattersNo ratings yet

- SEC v. Zouvas - Pump and Dump Complaint PDFDocument26 pagesSEC v. Zouvas - Pump and Dump Complaint PDFMark JaffeNo ratings yet

- Gpo-Conan-1992 The Constitution Analysis and InterpretationDocument2,466 pagesGpo-Conan-1992 The Constitution Analysis and InterpretationAlex VaubelNo ratings yet

- Lithium Company Facing Lawsuits Over MiningDocument37 pagesLithium Company Facing Lawsuits Over MiningEmma KoryntaNo ratings yet

- Request To ProduceDocument3 pagesRequest To Produceapi-506330375No ratings yet

- United States Court of Appeals, Tenth CircuitDocument12 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- United States v. Lester Genser and Lawrence Forman, 582 F.2d 292, 3rd Cir. (1978)Document28 pagesUnited States v. Lester Genser and Lawrence Forman, 582 F.2d 292, 3rd Cir. (1978)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Third CircuitDocument21 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Brief History of AuditingDocument7 pagesBrief History of AuditingAna-Maria Zaiceanu100% (2)

- In The Matter of The Search of The Premises Known As 6455 South Yosemite, Englewood, Colorado. Blinder, Robinson & Co., Inc., and Meyer Blinder v. United States, 897 F.2d 1549, 10th Cir. (1990)Document14 pagesIn The Matter of The Search of The Premises Known As 6455 South Yosemite, Englewood, Colorado. Blinder, Robinson & Co., Inc., and Meyer Blinder v. United States, 897 F.2d 1549, 10th Cir. (1990)Scribd Government DocsNo ratings yet

- Ecclesiastes 9:10-11 v. LMC Holding Company, 10th Cir. (2007)Document35 pagesEcclesiastes 9:10-11 v. LMC Holding Company, 10th Cir. (2007)Scribd Government DocsNo ratings yet

- Comstock v. Group of Institutional Investors, 335 U.S. 211 (1948)Document29 pagesComstock v. Group of Institutional Investors, 335 U.S. 211 (1948)Scribd Government DocsNo ratings yet

- SEC v. Spencer Pharmaceutical Inc Et Al Doc 191 Filed 30 Jan 15Document9 pagesSEC v. Spencer Pharmaceutical Inc Et Al Doc 191 Filed 30 Jan 15scion.scionNo ratings yet

- John J. Tigue, JR., Morvillo, Abramowitz, Grand, Iason & Silberberg, P.C. v. United States Department of Justice, Internal Revenue Service, 312 F.3d 70, 2d Cir. (2002)Document13 pagesJohn J. Tigue, JR., Morvillo, Abramowitz, Grand, Iason & Silberberg, P.C. v. United States Department of Justice, Internal Revenue Service, 312 F.3d 70, 2d Cir. (2002)Scribd Government DocsNo ratings yet

- Marie McDonnell Affidavit REDocument8 pagesMarie McDonnell Affidavit REJohn ReedNo ratings yet

- Transfer Tax Case DigestDocument30 pagesTransfer Tax Case DigestErneylou RanayNo ratings yet

- LYMAN v. The Bank of The United States, 53 U.S. 225 (1852)Document24 pagesLYMAN v. The Bank of The United States, 53 U.S. 225 (1852)Scribd Government DocsNo ratings yet

- Fed. Sec. L. Rep. P 95,471 United States of America v. Lloyd Dixon, JR., 536 F.2d 1388, 2d Cir. (1976)Document19 pagesFed. Sec. L. Rep. P 95,471 United States of America v. Lloyd Dixon, JR., 536 F.2d 1388, 2d Cir. (1976)Scribd Government DocsNo ratings yet

- 2nd Examiners Report On Enron BankruptcyDocument138 pages2nd Examiners Report On Enron BankruptcyAaron MonkNo ratings yet

- Ballard v. CIR, 522 F.3d 1229, 11th Cir. (2003)Document13 pagesBallard v. CIR, 522 F.3d 1229, 11th Cir. (2003)Scribd Government DocsNo ratings yet

- Blodgett v. Silberman, 277 U.S. 1 (1928)Document13 pagesBlodgett v. Silberman, 277 U.S. 1 (1928)Scribd Government DocsNo ratings yet

- Morris Koscove v. Commissioner of Internal Revenue, Sam Koscove v. Commissioner of Internal Revenue, 225 F.2d 85, 10th Cir. (1955)Document4 pagesMorris Koscove v. Commissioner of Internal Revenue, Sam Koscove v. Commissioner of Internal Revenue, 225 F.2d 85, 10th Cir. (1955)Scribd Government DocsNo ratings yet

- Cape Ann Investors v. Lepone, 305 F.3d 1, 1st Cir. (2002)Document20 pagesCape Ann Investors v. Lepone, 305 F.3d 1, 1st Cir. (2002)Scribd Government DocsNo ratings yet

- Topolobampo Terminal Company PlansDocument5 pagesTopolobampo Terminal Company PlansEdson_MarkNo ratings yet

- American AssemblyDocument32 pagesAmerican Assemblyflorinab2010No ratings yet

- Federal Maritime Commission v. New York Terminal Conference, 373 F.2d 424, 2d Cir. (1967)Document6 pagesFederal Maritime Commission v. New York Terminal Conference, 373 F.2d 424, 2d Cir. (1967)Scribd Government DocsNo ratings yet

- 2020-04-30 Upstream Addicks - Doc 283 Reported OrderDocument6 pages2020-04-30 Upstream Addicks - Doc 283 Reported OrderDaniel CharestNo ratings yet

- Contracting Reform: Expert Recommendations and Pending BillsDocument190 pagesContracting Reform: Expert Recommendations and Pending BillsScribd Government DocsNo ratings yet

- In Re Public Service Corp. of New Jersey. Drinker Biddle & Reath v. Securities and Exchange Commission. United Corp. v. Securities and Exchange Commission, 211 F.2d 231, 3rd Cir. (1954)Document5 pagesIn Re Public Service Corp. of New Jersey. Drinker Biddle & Reath v. Securities and Exchange Commission. United Corp. v. Securities and Exchange Commission, 211 F.2d 231, 3rd Cir. (1954)Scribd Government DocsNo ratings yet

- Maritime Overseas Corporation v. Puerto Rico Drydock & Marine Terminals, Inc., Libelant, 391 F.2d 1010, 1st Cir. (1968)Document9 pagesMaritime Overseas Corporation v. Puerto Rico Drydock & Marine Terminals, Inc., Libelant, 391 F.2d 1010, 1st Cir. (1968)Scribd Government DocsNo ratings yet

- Download The Federalization Of Corporate Governance Steinberg full chapterDocument67 pagesDownload The Federalization Of Corporate Governance Steinberg full chaptergwen.clark725100% (4)

- Uniform Fradulent Transfer ActDocument37 pagesUniform Fradulent Transfer ActpouhkaNo ratings yet

- US Department of Justice Antitrust Case Brief - 01869-217830Document4 pagesUS Department of Justice Antitrust Case Brief - 01869-217830legalmattersNo ratings yet

- United States Bankruptcy Court Central District of California Riverside DivisionDocument6 pagesUnited States Bankruptcy Court Central District of California Riverside DivisionChapter 11 DocketsNo ratings yet

- United States Bankruptcy Court Central District of California Riverside DivisionDocument69 pagesUnited States Bankruptcy Court Central District of California Riverside DivisionChapter 11 DocketsNo ratings yet

- Carl Thetford, Mamie Thetford, Charles Phelps, Irene Phelps and Sooner State Securities, Inc. v. United States, 404 F.2d 301, 10th Cir. (1968)Document4 pagesCarl Thetford, Mamie Thetford, Charles Phelps, Irene Phelps and Sooner State Securities, Inc. v. United States, 404 F.2d 301, 10th Cir. (1968)Scribd Government DocsNo ratings yet

- Finn v. Childs Co, 181 F.2d 431, 2d Cir. (1950)Document16 pagesFinn v. Childs Co, 181 F.2d 431, 2d Cir. (1950)Scribd Government DocsNo ratings yet

- United States Court of Appeals Second Circuit.: No. 294, Docket 30180Document6 pagesUnited States Court of Appeals Second Circuit.: No. 294, Docket 30180Scribd Government DocsNo ratings yet

- JSC First Amended Complaint For Wrongful ForeclosureDocument22 pagesJSC First Amended Complaint For Wrongful Foreclosurejsconrad12100% (1)

- Appdzme.: T6 ) Q, 1TlDocument5 pagesAppdzme.: T6 ) Q, 1TlChapter 11 DocketsNo ratings yet

- 4924 PDFDocument33 pages4924 PDFBen GreensteinNo ratings yet

- St. Bernard Parish Gov't v. United States, No. 05-1119L (Fed. Cl. May 4, 2016)Document44 pagesSt. Bernard Parish Gov't v. United States, No. 05-1119L (Fed. Cl. May 4, 2016)RHTNo ratings yet

- Gemini Shipping, Inc. v. Foreign Trade Organization For Chemicals and Foodstuffs and Syrian General Organization For Maritime Transport, 647 F.2d 317, 2d Cir. (1981)Document5 pagesGemini Shipping, Inc. v. Foreign Trade Organization For Chemicals and Foodstuffs and Syrian General Organization For Maritime Transport, 647 F.2d 317, 2d Cir. (1981)Scribd Government DocsNo ratings yet

- In The United States Bankruptcy Court Eastern District of Michigan Southern DivisionDocument3 pagesIn The United States Bankruptcy Court Eastern District of Michigan Southern DivisionChapter 11 DocketsNo ratings yet

- United States Court of Appeals, Second Circuit.: Nos. 137-140, Dockets 33119-33122Document13 pagesUnited States Court of Appeals, Second Circuit.: Nos. 137-140, Dockets 33119-33122Scribd Government DocsNo ratings yet

- King v. United States, 379 U.S. 329 (1964)Document10 pagesKing v. United States, 379 U.S. 329 (1964)Scribd Government DocsNo ratings yet

- United States Bankruptcy Court Central District of California Riverside DivisionDocument22 pagesUnited States Bankruptcy Court Central District of California Riverside DivisionChapter 11 DocketsNo ratings yet

- United States Court of Appeals First CircuitDocument10 pagesUnited States Court of Appeals First CircuitScribd Government DocsNo ratings yet

- United States Bankruptcy Court Southern District of New YorkDocument26 pagesUnited States Bankruptcy Court Southern District of New YorkChapter 11 DocketsNo ratings yet

- Evidencia de Fiscalía Federal Caso Tata CharbonierDocument9 pagesEvidencia de Fiscalía Federal Caso Tata CharbonierVictor Torres MontalvoNo ratings yet

- Henry G. Vickers v. Securities and Exchange Commission, 383 F.2d 343, 2d Cir. (1967)Document2 pagesHenry G. Vickers v. Securities and Exchange Commission, 383 F.2d 343, 2d Cir. (1967)Scribd Government DocsNo ratings yet

- clp11 09Document22 pagesclp11 09Charlton ButlerNo ratings yet

- United States Court of Appeals, Third CircuitDocument4 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- ALU 202 Sample QuestionsDocument4 pagesALU 202 Sample QuestionsShabihe FatimaNo ratings yet

- Finance 335 Exam 1 ReviewDocument5 pagesFinance 335 Exam 1 ReviewThùy DươngNo ratings yet

- Venn DiagramDocument7 pagesVenn DiagramDimitri SaundersNo ratings yet

- Financial Management: Interest RatesDocument12 pagesFinancial Management: Interest RatesArif SharifNo ratings yet

- Last Time Tips by CA Ankit PatwariDocument41 pagesLast Time Tips by CA Ankit PatwariSundarNo ratings yet

- Internal assignment on mutual fund law, fees, worth and ethical concernsDocument3 pagesInternal assignment on mutual fund law, fees, worth and ethical concernsShashwat ShuklaNo ratings yet

- Wealth Management Assignment 8: 1. What Are Mutual Funds?Document2 pagesWealth Management Assignment 8: 1. What Are Mutual Funds?Darshan ShahNo ratings yet

- Gen Math 11 Exam 2nd FINALDocument4 pagesGen Math 11 Exam 2nd FINALBill VillonNo ratings yet

- Risk AssignmentDocument4 pagesRisk AssignmentMd. Asifujjaman JoyNo ratings yet

- Amortization MethodDocument6 pagesAmortization MethodCy BathanNo ratings yet

- (Surekha S Yadav BAF) Black Book ProjectDocument61 pages(Surekha S Yadav BAF) Black Book ProjectArun SinghNo ratings yet

- Sana Oil Medical Clinic financial recordsDocument2 pagesSana Oil Medical Clinic financial recordsMharva Mae Ilagan LiwanagNo ratings yet

- Reading List: Solvency IIDocument30 pagesReading List: Solvency IIObideoNo ratings yet

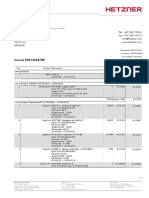

- Hetzner 2021-06-22 R0013604788Document2 pagesHetzner 2021-06-22 R0013604788Vitaliy PodobaNo ratings yet

- 6.2 Due Diligence Checklist Template V2 3Document3 pages6.2 Due Diligence Checklist Template V2 3Fábio Miguel AzedoNo ratings yet

- Chase Quickpay® With Zelle Service Agreement and Privacy NoticeDocument18 pagesChase Quickpay® With Zelle Service Agreement and Privacy NoticeRELOJERIANo ratings yet

- Senior Risk Manager in Cincinnati OH Resume David RussellDocument2 pagesSenior Risk Manager in Cincinnati OH Resume David RussellDavidRussell1100% (1)

- 6.revised Galvanized Iron Sheet Product Producing PlantDocument23 pages6.revised Galvanized Iron Sheet Product Producing PlantaschalewNo ratings yet

- Credit Analysis of Large Borrowers and SMEsDocument106 pagesCredit Analysis of Large Borrowers and SMEsPriya SaraswatNo ratings yet

- Date: 26/11/2018 FILE No.: 875146: Instrument Type Instrument No. Instrument Date Amount (INR) Infavour ofDocument21 pagesDate: 26/11/2018 FILE No.: 875146: Instrument Type Instrument No. Instrument Date Amount (INR) Infavour ofYogesh WadhwaNo ratings yet

- Assets, Liabilities & Equity StatementDocument41 pagesAssets, Liabilities & Equity StatementVILLENA, CHARL ISAR RONELL F.No ratings yet

- Qdoc - Tips Internship Report On MCBDocument50 pagesQdoc - Tips Internship Report On MCBRaza AliNo ratings yet

- Financial Institutions & Financial Markets Module - 1: by Sanjeev TamhaneDocument35 pagesFinancial Institutions & Financial Markets Module - 1: by Sanjeev TamhaneSwagatJagtapNo ratings yet

- Financial & Managerial Accounting MbasDocument40 pagesFinancial & Managerial Accounting MbasHồng Long100% (1)

- FSCM Digest Incl AdditionalDocument194 pagesFSCM Digest Incl AdditionalCA Kuldeep Pandya100% (1)

- Acct Statement XX0667 11102022Document8 pagesAcct Statement XX0667 11102022Mantasha Financial servicesNo ratings yet

- Startup Valuation ExplorerDocument22 pagesStartup Valuation Explorershandhin.malviya07No ratings yet

- Unadjusted Trial Balance Adjustments Account Titles Debit Credit DebitDocument6 pagesUnadjusted Trial Balance Adjustments Account Titles Debit Credit DebitAllen CarlNo ratings yet

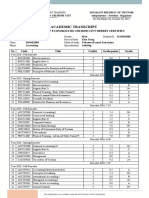

- Bảng Điểm Học Tập Tiếng Anh Sinh Viên ĐHCQ-VLVH PDFDocument2 pagesBảng Điểm Học Tập Tiếng Anh Sinh Viên ĐHCQ-VLVH PDFLoki LukeNo ratings yet

- Lecture 9 Monetary Policy Decision Making 2022Document40 pagesLecture 9 Monetary Policy Decision Making 2022Onyee FongNo ratings yet