You might also like

- Law of Insurance AsignmentDocument12 pagesLaw of Insurance AsignmentDheeraj KumarNo ratings yet

- Literature Review of Sbi Life InsuranceDocument8 pagesLiterature Review of Sbi Life Insurancec5qz47sm100% (1)

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- Irda - Hand Book On Life InsuranceDocument12 pagesIrda - Hand Book On Life InsuranceRajesh SinghNo ratings yet

- Life Insurance HandbookDocument12 pagesLife Insurance HandbookChi MnuNo ratings yet

- Life Insurance ProjectDocument11 pagesLife Insurance ProjectDarshana MathurNo ratings yet

- Term Paper of BankingDocument22 pagesTerm Paper of BankingnidhijunejaNo ratings yet

- Insurance Types, Calculators & PlansDocument21 pagesInsurance Types, Calculators & PlansanannyamukherejeeNo ratings yet

- What Is Life Insurance?Document11 pagesWhat Is Life Insurance?Ratul BanerjeeNo ratings yet

- Product & ServiceDocument11 pagesProduct & ServicefarrukhNo ratings yet

- Bbmf2083 Insurance Management Chapter 5 Understand Life Insurance Policy Contracts (Answers)Document7 pagesBbmf2083 Insurance Management Chapter 5 Understand Life Insurance Policy Contracts (Answers)Eileen WongNo ratings yet

- Child Insurance PlanDocument6 pagesChild Insurance PlanAditya MoreNo ratings yet

- DOODHWAALADocument5 pagesDOODHWAALAShubham SardaNo ratings yet

- Financial PlanningDocument21 pagesFinancial PlanningCma Saurabh AroraNo ratings yet

- Week 9 Exercises Suggested Answers (Financial Planning Components Part III - Group A - Sem B 2019 - 20)Document2 pagesWeek 9 Exercises Suggested Answers (Financial Planning Components Part III - Group A - Sem B 2019 - 20)tanning zhuNo ratings yet

- SBI ProjectDocument82 pagesSBI Projectchandan sharmaNo ratings yet

- Assignment On Postal Life InsuranceDocument5 pagesAssignment On Postal Life Insurancesabbir HossainNo ratings yet

- Life Insurance in India - 4Document7 pagesLife Insurance in India - 4Himansu S MNo ratings yet

- Insurance - deciding best insurance for familyDocument3 pagesInsurance - deciding best insurance for familyHarris ArifinNo ratings yet

- Banking LawDocument7 pagesBanking LawElsa ShaikhNo ratings yet

- Need For Life InsuranceDocument9 pagesNeed For Life InsuranceDeepak NayakNo ratings yet

- Introduction of Life InsuranceDocument23 pagesIntroduction of Life InsuranceManwinder Singh GillNo ratings yet

- Summer Internship Sales Report for Shriram Life InsuranceDocument7 pagesSummer Internship Sales Report for Shriram Life InsuranceShakTi SînghNo ratings yet

- Smart Scholar Brochure_V04 (1)Document20 pagesSmart Scholar Brochure_V04 (1)jalligangadhararaoNo ratings yet

- Postal Life InsuranceDocument29 pagesPostal Life InsuranceBratanu Das100% (1)

- Literature Review On Sbi Life InsuranceDocument4 pagesLiterature Review On Sbi Life Insurancefvgneqv8100% (1)

- Presented By: Mr. Rashmi Ranjan PanigrahiDocument35 pagesPresented By: Mr. Rashmi Ranjan PanigrahiRashmi Ranjan PanigrahiNo ratings yet

- Banking and Insurance Needs AnalysisDocument16 pagesBanking and Insurance Needs AnalysisMathew KanichayNo ratings yet

- Handbook On Third Party Products FinalDocument23 pagesHandbook On Third Party Products FinalraghuviltapuramNo ratings yet

- Life Insurance Exam Questions and Answers PDFDocument13 pagesLife Insurance Exam Questions and Answers PDFDairo GaniyatNo ratings yet

- Group Assignment G-12Document25 pagesGroup Assignment G-12sauravNo ratings yet

- Life InsuranceDocument26 pagesLife Insurancevivek kant100% (1)

- Importance of Life Insurance in IndiaDocument10 pagesImportance of Life Insurance in IndiaYogesh Karekar100% (1)

- Financial Retirement PlanDocument2 pagesFinancial Retirement PlansscalNo ratings yet

- Presentation: State Life Insurance Corporation of PakistanDocument16 pagesPresentation: State Life Insurance Corporation of PakistanAlee HulioNo ratings yet

- Wa0006.Document3 pagesWa0006.Sonu AnandNo ratings yet

- Need of InsuranceDocument4 pagesNeed of InsuranceNAISHADH DESAINo ratings yet

- Health InsuranceDocument11 pagesHealth InsurancedishaNo ratings yet

- TESTDocument3 pagesTESTSurekhaNo ratings yet

- Case 2Document3 pagesCase 2angeliaNo ratings yet

- Module 13 Life InsuranceDocument6 pagesModule 13 Life InsuranceDonna Mae FernandezNo ratings yet

- Report Income Protection and Educational PlanningDocument4 pagesReport Income Protection and Educational PlanningSyai GenjNo ratings yet

- Tips While Buying A Child Education PlanDocument7 pagesTips While Buying A Child Education PlanJyotsana SachdevaNo ratings yet

- Finance Case AnalysisDocument6 pagesFinance Case AnalysisJane OmbrosaNo ratings yet

- 3.7 Who Should Buy Life Insurance?: 1. Begining FamiliesDocument10 pages3.7 Who Should Buy Life Insurance?: 1. Begining FamiliesFarhana Foysal SatataNo ratings yet

- How Rs 3.2 Lacs Became Rs 11,678 in 6 Years?Document8 pagesHow Rs 3.2 Lacs Became Rs 11,678 in 6 Years?Ishita AgrawalNo ratings yet

- Protect Your Family with Life InsuranceDocument8 pagesProtect Your Family with Life InsuranceJennieNo ratings yet

- Private Insurance CompaniesDocument11 pagesPrivate Insurance CompaniesclytemnestraNo ratings yet

- Asse T Revi Ew: Activi Ty Centr e Educa Tion Plann ErDocument13 pagesAsse T Revi Ew: Activi Ty Centr e Educa Tion Plann ErkvijayasokNo ratings yet

- Risk & EstateDocument7 pagesRisk & Estatekamal prajapatNo ratings yet

- Smart Scholar Brochure BRDocument21 pagesSmart Scholar Brochure BRshabeer123No ratings yet

- Application of Portfolio Theory in Real LifeDocument13 pagesApplication of Portfolio Theory in Real LifeVaibhav DayalNo ratings yet

- Social Science (2021-22)Document9 pagesSocial Science (2021-22)KshitijNo ratings yet

- Barbeque Nation 1234Document111 pagesBarbeque Nation 1234KshitijNo ratings yet

- The Making of The National MovementDocument3 pagesThe Making of The National MovementKshitijNo ratings yet

- Lupin Ltd Equity Research AnalysisDocument14 pagesLupin Ltd Equity Research AnalysisRohan AgrawalNo ratings yet

- CK Kshitij CBR COUUNTRY ANALYSIS ECONOMICS - (22018)Document18 pagesCK Kshitij CBR COUUNTRY ANALYSIS ECONOMICS - (22018)KshitijNo ratings yet

- MultibaggerDocument14 pagesMultibaggerHirenNo ratings yet

- 9 - Future and Confirm FutureDocument4 pages9 - Future and Confirm FutureMatangi DaveNo ratings yet

- SSS Law: A Guide to the Social Security SystemDocument21 pagesSSS Law: A Guide to the Social Security SystemMarlyn Dizon Manalad100% (1)

- Leave Rule 7Document1 pageLeave Rule 7sivaramakumarNo ratings yet

- A Dissertation Report ON Employee'S Pension OF Tata Steel LimitedDocument19 pagesA Dissertation Report ON Employee'S Pension OF Tata Steel LimitedSimran SrivastavaNo ratings yet

- Pension RulesDocument7 pagesPension RulesVivek Pal SinghNo ratings yet

- Employee Benefits and Defined Benefit Plans AnalysisDocument5 pagesEmployee Benefits and Defined Benefit Plans AnalysisNacelleNo ratings yet

- Toaz - Info Cfas Quiz PRDocument9 pagesToaz - Info Cfas Quiz PRASHERAH ENGKONGNo ratings yet

- Audit Report - Massachusetts State Retirement BoardDocument29 pagesAudit Report - Massachusetts State Retirement BoardShira SchoenbergNo ratings yet

- Pensions Glossary 2004Document22 pagesPensions Glossary 2004camiladiasmanoelNo ratings yet

- June 21, 2014Document16 pagesJune 21, 2014The Delphos HeraldNo ratings yet

- 2.4.4 Office Manual Iv - Vol. 4Document391 pages2.4.4 Office Manual Iv - Vol. 4KuldipSonowalNo ratings yet

- Latest NPS Sunny Dogra - RemovedDocument1 pageLatest NPS Sunny Dogra - Removeddinesh makwanaNo ratings yet

- Bashir Ahmad SO Yar Muhammad, PPO MC, BWNDocument1 pageBashir Ahmad SO Yar Muhammad, PPO MC, BWNTao TmaNo ratings yet

- Basic Questions To Answer-: The Asset Allocation DecisionDocument52 pagesBasic Questions To Answer-: The Asset Allocation DecisionKazi FahimNo ratings yet

- India Gratuity Policy SummaryDocument7 pagesIndia Gratuity Policy SummarynivasshaanNo ratings yet

- Income Tax Act Cap 470 Revised 2021-3-1Document224 pagesIncome Tax Act Cap 470 Revised 2021-3-1danielNo ratings yet

- AGI-IPP 1-17 Financial-Literacy FINAL PDFDocument32 pagesAGI-IPP 1-17 Financial-Literacy FINAL PDFmrandres1725No ratings yet

- P&A - Taxation of Retirement BenefitsDocument2 pagesP&A - Taxation of Retirement BenefitsCkey ArNo ratings yet

- Financial Literacy Among The YoungDocument23 pagesFinancial Literacy Among The YoungJulio César SilvaNo ratings yet

- The Benefits Determination Process: Mcgraw-Hill/IrwinDocument23 pagesThe Benefits Determination Process: Mcgraw-Hill/IrwinPrriyankhaMuddamNo ratings yet

- Dayworks - January 2013Document2 pagesDayworks - January 2013swamydceNo ratings yet

- Ageing Baby BoomersDocument118 pagesAgeing Baby Boomersstephloh100% (1)

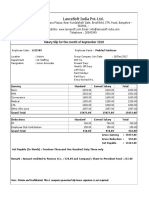

- LanceSoft September Salary SlipDocument1 pageLanceSoft September Salary SlipPRAHLAD VAISHNAV100% (1)

- P. D 1638Document9 pagesP. D 1638Ann SCNo ratings yet

- Government of Telangana Form of Application For Service Pension/ Family Pension/Retirement Gratuity/Service Gratuity/CommutationDocument12 pagesGovernment of Telangana Form of Application For Service Pension/ Family Pension/Retirement Gratuity/Service Gratuity/Commutationvenkat swamyNo ratings yet

- Leave and Joining Time Rules: National Seeds Corporation Limited (A Government of India Undertaking)Document26 pagesLeave and Joining Time Rules: National Seeds Corporation Limited (A Government of India Undertaking)Rojan MathewNo ratings yet

- Quirico D. Aniñon vs. Government Service Insurance System April 10, 2019, G.R. No. 190410Document2 pagesQuirico D. Aniñon vs. Government Service Insurance System April 10, 2019, G.R. No. 190410WaRynbeth MaljatoNo ratings yet

- RA 8551-Philippine National Police Reform and Reorganization Act of 1998Document29 pagesRA 8551-Philippine National Police Reform and Reorganization Act of 1998Rocky MarcianoNo ratings yet

- In The High Court of Sindh at Karachi: Constitutional Petition No. D - 1497 of 2020Document9 pagesIn The High Court of Sindh at Karachi: Constitutional Petition No. D - 1497 of 2020Salman AhmedNo ratings yet

- NAPOLCOM Welfare Benefits For Uniformed Members of TheDocument62 pagesNAPOLCOM Welfare Benefits For Uniformed Members of TheFrancis Brion100% (1)