You might also like

- ISO 22301: 2019 - An introduction to a business continuity management system (BCMS)From EverandISO 22301: 2019 - An introduction to a business continuity management system (BCMS)Rating: 4 out of 5 stars4/5 (1)

- Form 04 CNV-TNCN - enDocument2 pagesForm 04 CNV-TNCN - enBao Trung Dang100% (1)

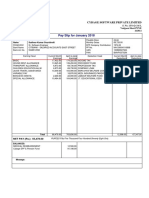

- Pay Slip For January 2018: Cybage Software Private LimitedDocument1 pagePay Slip For January 2018: Cybage Software Private LimitedSudheer0% (1)

- PR - 08 - 2019 Changes Basis PeriodDocument42 pagesPR - 08 - 2019 Changes Basis PeriodAnis RoslanNo ratings yet

- Kotak Mahindra Bank Limited FY22 23Document197 pagesKotak Mahindra Bank Limited FY22 23prabhatkumarrock27No ratings yet

- Inland Revenue Board Malaysia: Public Ruling No. 2/2011Document23 pagesInland Revenue Board Malaysia: Public Ruling No. 2/2011Ken ChiaNo ratings yet

- SAC Statement 214th SAC Meeting - EngDocument7 pagesSAC Statement 214th SAC Meeting - EngSyafiiq HishamNo ratings yet

- Chapter 4 Employment IncomeDocument29 pagesChapter 4 Employment IncomeLOO YU HUANGNo ratings yet

- PR 8 2022Document29 pagesPR 8 2022cheechuen999No ratings yet

- Audit of CFSDocument30 pagesAudit of CFSDhivyaNo ratings yet

- PR 2 2017 Amended 12072017 PDFDocument27 pagesPR 2 2017 Amended 12072017 PDFZTNo ratings yet

- ASC Group - Budget 2021 HighlightsDocument32 pagesASC Group - Budget 2021 Highlightssaurav royNo ratings yet

- Directors Report As Per Section 134 (3) - 31122021Document4 pagesDirectors Report As Per Section 134 (3) - 31122021SHIKHA SHARMANo ratings yet

- Malom Foods 2022Document13 pagesMalom Foods 2022Samuel kwateiNo ratings yet

- 67409bos54195 cp8Document30 pages67409bos54195 cp8IntrovertNo ratings yet

- Annual Compliance Calendar - Companies Act, 2013 LISTED COMPANY - Series 527 PDFDocument13 pagesAnnual Compliance Calendar - Companies Act, 2013 LISTED COMPANY - Series 527 PDFGaurav SharmaNo ratings yet

- Annual Report of IOCL 126Document1 pageAnnual Report of IOCL 126NikunjNo ratings yet

- Board'S Report: To The Members, Review of OperationsDocument74 pagesBoard'S Report: To The Members, Review of OperationsSudha Swayam PravaNo ratings yet

- UntitledDocument303 pagesUntitledHarismithaNo ratings yet

- New IFRS Pronouncements Q4 2022Document6 pagesNew IFRS Pronouncements Q4 2022zprincewantonxNo ratings yet

- Inland Revenue Board of Malaysia: Unit Trust Funds Part Ii - Taxation of Unit TrustsDocument18 pagesInland Revenue Board of Malaysia: Unit Trust Funds Part Ii - Taxation of Unit TrustsKen ChiaNo ratings yet

- 325224-2022-Clarification On Transitory Provision For20220412-12-1en6j3qDocument1 page325224-2022-Clarification On Transitory Provision For20220412-12-1en6j3qRen Mar CruzNo ratings yet

- Tutorial 2 (1) Q1 - Q4Document8 pagesTutorial 2 (1) Q1 - Q4Shan JeefNo ratings yet

- Bangladesh Tax PlanningDocument22 pagesBangladesh Tax PlanningRobiulNo ratings yet

- Withholding Tax CertificateDocument46 pagesWithholding Tax CertificateJen OshNo ratings yet

- Set OffDocument9 pagesSet OffAditya MehtaniNo ratings yet

- Annual Report 2021-22 PDFDocument179 pagesAnnual Report 2021-22 PDFMohnish KhianiNo ratings yet

- Audit NotesDocument11 pagesAudit NotesNavjyoti SinghNo ratings yet

- Overview of Income Tax 2017 by Masum PDFDocument44 pagesOverview of Income Tax 2017 by Masum PDFAl-Muzahid EmuNo ratings yet

- Solicitor Exam Materials (Pages 185 To 515)Document331 pagesSolicitor Exam Materials (Pages 185 To 515)bobjones1111No ratings yet

- Annual Report 2022 23Document176 pagesAnnual Report 2022 23Avinash ChauhanNo ratings yet

- Allowable Pre-Operational and Pre-Commencement Business Expenses - PR 2-2010 (030610)Document15 pagesAllowable Pre-Operational and Pre-Commencement Business Expenses - PR 2-2010 (030610)daydayNo ratings yet

- Directors Report 2022 - Dynasty BuildwellDocument9 pagesDirectors Report 2022 - Dynasty Buildwellprachika29No ratings yet

- Inland Revenue Board of Malaysia: Date of Publication: 6 December 2019Document22 pagesInland Revenue Board of Malaysia: Date of Publication: 6 December 2019abhishekmath123No ratings yet

- Consolidated Financial Statement 2019 q4 25 Feb 2020 PDFDocument83 pagesConsolidated Financial Statement 2019 q4 25 Feb 2020 PDFOtta Muhammad TarregaNo ratings yet

- RSM India Union Budget 2021 HighlightsDocument132 pagesRSM India Union Budget 2021 HighlightsSunil KumarNo ratings yet

- AFA 4e PPT Chap03Document26 pagesAFA 4e PPT Chap03Oh SehunNo ratings yet

- Deloitte Budget Update - 2019Document24 pagesDeloitte Budget Update - 2019Carol PereiraNo ratings yet

- CH8 Audit of CFSDocument30 pagesCH8 Audit of CFSkarthiksalapu2040No ratings yet

- Consolidated Financial Statement Q4 2020Document79 pagesConsolidated Financial Statement Q4 2020Edo AgusNo ratings yet

- rp2022 23Document24 pagesrp2022 23nihalNo ratings yet

- IND ASyear-end-consideration-tl - EYDocument56 pagesIND ASyear-end-consideration-tl - EYDilip ChoudharyNo ratings yet

- Annual Report FY2020Document424 pagesAnnual Report FY2020SAGAR KASERANo ratings yet

- Tax Memorandum 2012 FinalDocument58 pagesTax Memorandum 2012 FinalAzka KhalidNo ratings yet

- Company Law Dec 2023 SupplementDocument47 pagesCompany Law Dec 2023 Supplementsuraj music channelNo ratings yet

- FIN408 Assignment 1Document34 pagesFIN408 Assignment 1Ahnaf RaselNo ratings yet

- Chapter 5 and 6 (PaPoT)Document41 pagesChapter 5 and 6 (PaPoT)dua tanveerNo ratings yet

- GSL Annual Report 2021-22Document159 pagesGSL Annual Report 2021-22Mayank SinhaNo ratings yet

- Conceptual Framework: Amendments To IFRS 3 - Reference To TheDocument3 pagesConceptual Framework: Amendments To IFRS 3 - Reference To TheteguhsunyotoNo ratings yet

- Overview of Income Tax 2014Document40 pagesOverview of Income Tax 2014masumidbNo ratings yet

- Abridged Directors' Report: Financial ResultsDocument2 pagesAbridged Directors' Report: Financial ResultsYOGESH AGRAWALNo ratings yet

- Audit of CFSDocument30 pagesAudit of CFSkaran kapadiaNo ratings yet

- Company Law Cs ExecutiveDocument57 pagesCompany Law Cs ExecutiveEISHAN PATELNo ratings yet

- 2cjvoeqflu7sw8 Yid1o4pb 6cvddrcbdeqj Kz6clyDocument24 pages2cjvoeqflu7sw8 Yid1o4pb 6cvddrcbdeqj Kz6clySuzlonNo ratings yet

- AR201920Document185 pagesAR201920utkarsh tripathiNo ratings yet

- Setoff Carry Forward - UnlockedDocument30 pagesSetoff Carry Forward - Unlockedsohamdivekar9867No ratings yet

- Solution Manual For South Western Federal Taxation 2020 Corporations Partnerships Estates and Trusts 43rd Edition William A RaabeDocument19 pagesSolution Manual For South Western Federal Taxation 2020 Corporations Partnerships Estates and Trusts 43rd Edition William A RaabeCourtneyCollinsntwex100% (40)

- 18-Winter 2018 - BT - SADocument7 pages18-Winter 2018 - BT - SApabloescobar11yNo ratings yet

- Maven Minds Budget Brief 2022Document24 pagesMaven Minds Budget Brief 2022Salman AhmedNo ratings yet

- Joaxjill NotesDocument6 pagesJoaxjill NotesAlliah Czyrielle Amorado PersinculaNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- T2 Belief in AllahDocument19 pagesT2 Belief in AllahJeffrey YeeNo ratings yet

- SPM Biology P1+P2Document13 pagesSPM Biology P1+P2Jeffrey YeeNo ratings yet

- SPM Chemistry P1+P2Document17 pagesSPM Chemistry P1+P2Jeffrey YeeNo ratings yet

- 2022 2023 Flexible MSC Programme Module ScheduleDocument2 pages2022 2023 Flexible MSC Programme Module ScheduleJeffrey YeeNo ratings yet

- Jan Payslip PDFDocument2 pagesJan Payslip PDFKumar VarunNo ratings yet

- VAT LetterDocument2 pagesVAT Letterrhea CabillanNo ratings yet

- Invoice 5182Document1 pageInvoice 5182Aimee GonzalezNo ratings yet

- Payslip For The Month of Mar 2021Document1 pagePayslip For The Month of Mar 2021Loan LoanNo ratings yet

- Estimate Calling Script 2023 Financial YearDocument4 pagesEstimate Calling Script 2023 Financial Yearapril jean ondoyNo ratings yet

- Central Sales Tax ActDocument4 pagesCentral Sales Tax Actdiwakaritm2674No ratings yet

- 121 521727755 P I PDFDocument3 pages121 521727755 P I PDFMuhammad kabir jamilNo ratings yet

- Alliance Broadband Services PVT LTD: Tax InvoiceDocument1 pageAlliance Broadband Services PVT LTD: Tax InvoiceacctsagarwalNo ratings yet

- Resident Status For IndividualDocument24 pagesResident Status For IndividualMalabaris Malaya Umar SiddiqNo ratings yet

- Income Tax Bba 5 Sem QuestionDocument18 pagesIncome Tax Bba 5 Sem QuestionArun GuptaNo ratings yet

- Purchase Order: QuantityDocument2 pagesPurchase Order: QuantityNhan NguyentrongNo ratings yet

- F6 InterimDocument7 pagesF6 InterimSad AnwarNo ratings yet

- A Critical Review of The Tax Structure of BangladeshDocument4 pagesA Critical Review of The Tax Structure of BangladeshSumaiya IslamNo ratings yet

- Avtex W270TSDocument1 pageAvtex W270TSAre GeeNo ratings yet

- Tax Review Cases (Digested)Document41 pagesTax Review Cases (Digested)Tokie TokiNo ratings yet

- The Plain Bagel Budgeting SpreadsheetDocument2 pagesThe Plain Bagel Budgeting Spreadsheetshunt18No ratings yet

- PDF 923744260220722Document1 pagePDF 923744260220722Ashish SinghNo ratings yet

- Reagan Vs CIRDocument1 pageReagan Vs CIRemmaniago08No ratings yet

- Loan ConfirmationDocument1 pageLoan Confirmationkrishnajhawar100% (4)

- Ae23 Capital Budgeting 2Document2 pagesAe23 Capital Budgeting 2Hanielyn TagupaNo ratings yet

- Act370 QuizDocument3 pagesAct370 Quizshamim islam limonNo ratings yet

- Chapter 15 & 17 Q & SDocument7 pagesChapter 15 & 17 Q & Sgabie stgNo ratings yet

- Accounting For Income TaxDocument3 pagesAccounting For Income TaxDaniel Kahn GillamacNo ratings yet

- Chapter 1 - Basis Period and Change in Accounting DatesDocument7 pagesChapter 1 - Basis Period and Change in Accounting DatesNURKHAIRUNNISA100% (3)

- Oman Income TaxDocument84 pagesOman Income TaxsoumenNo ratings yet

- BPI vs. CA, GR#122480, April 12, 2000Document7 pagesBPI vs. CA, GR#122480, April 12, 2000Khenlie VillaceranNo ratings yet

- CTIM Professional ExaminationDocument23 pagesCTIM Professional Examination刘宝英No ratings yet

- In The Central Family Court Case No: Bv18D31762 Between:-David Brocklesby Applicant - and - Munkhtuya Dashzeveg RespondentDocument3 pagesIn The Central Family Court Case No: Bv18D31762 Between:-David Brocklesby Applicant - and - Munkhtuya Dashzeveg RespondentTuya DashzevegNo ratings yet