You might also like

- Winding UpDocument9 pagesWinding UpJedaiah CruzNo ratings yet

- AFM NotesDocument110 pagesAFM NotesNguyen NhanNo ratings yet

- Damodaran, A. - Capital Structure and Financing DecisionsDocument107 pagesDamodaran, A. - Capital Structure and Financing DecisionsJohnathan Fitz KennedyNo ratings yet

- QUESTION 6-17 Multiple Choice (Conceptual Framework) : A. RecognitionDocument9 pagesQUESTION 6-17 Multiple Choice (Conceptual Framework) : A. RecognitionJanine CamachoNo ratings yet

- Financial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsFrom EverandFinancial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsNo ratings yet

- Fixed Income Attribution WhitepaperDocument24 pagesFixed Income Attribution WhitepaperreviurNo ratings yet

- 395 33 Powerpoint Slides 1 Financial Management Overview CHAPTER 1Document25 pages395 33 Powerpoint Slides 1 Financial Management Overview CHAPTER 1Ravi Pratap Singh TomarNo ratings yet

- Math WD Solns 3Document23 pagesMath WD Solns 3Chemuel Mardie G. Obedencio100% (6)

- Financial Analysis InsDocument21 pagesFinancial Analysis InsTadele DandenaNo ratings yet

- Microsoft Word - F3 - Revision SummariesDocument45 pagesMicrosoft Word - F3 - Revision SummariesAnonymous keHdP6roNo ratings yet

- List of Charities For People in Need PDFDocument21 pagesList of Charities For People in Need PDFAttie7613No ratings yet

- 17 09 12 Tastytrade ResearchDocument9 pages17 09 12 Tastytrade ResearchMarcus OngNo ratings yet

- Fintech Start-Ups IndonesiaDocument69 pagesFintech Start-Ups IndonesiaRea Emerald100% (1)

- Debit and Credit MemoDocument2 pagesDebit and Credit MemoRabin DebnathNo ratings yet

- Chap 5Document23 pagesChap 5selva0% (1)

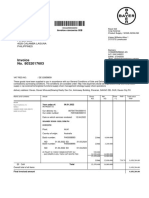

- Invoice No. 8032017603: Bayer Cropscience Inc. 3rd Flr. Bayer House PO Box 4600 4028 Calamba Laguna PhilippinesDocument2 pagesInvoice No. 8032017603: Bayer Cropscience Inc. 3rd Flr. Bayer House PO Box 4600 4028 Calamba Laguna PhilippinesGlezilda LoberianoNo ratings yet

- Fin622 Mid Term Enjoy PDFDocument7 pagesFin622 Mid Term Enjoy PDFAtteique AnwarNo ratings yet

- Topic: Portfolio Management: Presented By: Akshi Chandyoke Manohar Gupta Pooja Shukla Vinod PanigrahiDocument22 pagesTopic: Portfolio Management: Presented By: Akshi Chandyoke Manohar Gupta Pooja Shukla Vinod PanigrahiRavikant ShuklaNo ratings yet

- Lesson 5: Measuring and Evaluating The Performance of BanksDocument31 pagesLesson 5: Measuring and Evaluating The Performance of BanksDevica UditramNo ratings yet

- MCQ's TreasureDocument144 pagesMCQ's TreasureAmmad HassanNo ratings yet

- Chapter 21 - Capital Structure DecisionsDocument107 pagesChapter 21 - Capital Structure Decisionsanon_955424412No ratings yet

- 8 Responsibility AccountingDocument8 pages8 Responsibility AccountingXyril MañagoNo ratings yet

- SFM Last Day Revision Notes by CA Dinesh Jain SirDocument74 pagesSFM Last Day Revision Notes by CA Dinesh Jain SirVaibhav GandhiNo ratings yet

- RiskDocument10 pagesRiskSanath FernandoNo ratings yet

- An Overview of Financial ManagementDocument37 pagesAn Overview of Financial ManagementTrang312No ratings yet

- F3 - Summary Notes - Ultimate AccessDocument148 pagesF3 - Summary Notes - Ultimate AccessRecruit guideNo ratings yet

- Pricing, Loans, AmmarDocument2 pagesPricing, Loans, AmmarAmmarNo ratings yet

- Op Risk MGTDocument64 pagesOp Risk MGTDrAkhilesh TripathiNo ratings yet

- CAMELS ApproachDocument12 pagesCAMELS ApproachAreeb AsifNo ratings yet

- Capital ManagementDocument29 pagesCapital Managementproximastar100% (1)

- Chapter 06Document25 pagesChapter 06Farjana Hossain DharaNo ratings yet

- Chapter 2 Capital Structure and Financial LeverageDocument59 pagesChapter 2 Capital Structure and Financial Leverageabdirahman mohamedNo ratings yet

- Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsDocument46 pagesMeasuring and Evaluating The Performance of Banks and Their Principal CompetitorsyeehawwwwNo ratings yet

- Fundamental Analysis Chaper 1Document19 pagesFundamental Analysis Chaper 1Mukesh YadavNo ratings yet

- MAN Annual Report 2011Document138 pagesMAN Annual Report 2011Daniele Del MonteNo ratings yet

- Report TTDocument24 pagesReport TTvaibhavagrawal04102003No ratings yet

- MGT201 Finalterm GoldenFileDocument230 pagesMGT201 Finalterm GoldenFilemaryamNo ratings yet

- Chapter 5 - Part 1Document50 pagesChapter 5 - Part 1Kiều PhươngNo ratings yet

- CFA FinalDocument180 pagesCFA FinalJazmin Vidalon ParionaNo ratings yet

- MGT201 MEGAMIDTERMSOLVEDPAPERSby FaisalDocument320 pagesMGT201 MEGAMIDTERMSOLVEDPAPERSby FaisalmaryamNo ratings yet

- Baf 361 Introduction To Corporate Finance and Banking: Lecture 2-Financial Planning and Raising of FundsDocument28 pagesBaf 361 Introduction To Corporate Finance and Banking: Lecture 2-Financial Planning and Raising of FundsRevivalist Arthur - GeomanNo ratings yet

- Lec 1Document35 pagesLec 1Mohamed AliNo ratings yet

- Aviva PLC Investor and Analyst Update 5 July 2012Document45 pagesAviva PLC Investor and Analyst Update 5 July 2012Aviva GroupNo ratings yet

- Ratios & Trend Analysis: Week 7Document65 pagesRatios & Trend Analysis: Week 7Zuhaib AhmedNo ratings yet

- Bank Administration: Ratio AnalysisDocument33 pagesBank Administration: Ratio AnalysisSharma AmitNo ratings yet

- Multinational Corporations and Global Financial Environment: Facilities in More Than One CountryDocument11 pagesMultinational Corporations and Global Financial Environment: Facilities in More Than One CountryANH NGUYEN DANG QUENo ratings yet

- MCqs Financial ManagementDocument30 pagesMCqs Financial ManagementMohsin KhanNo ratings yet

- Introduction To Financial ManagementDocument41 pagesIntroduction To Financial Managementamits3989No ratings yet

- Lending - Unit 6 - Monitoring and Control of LendingDocument33 pagesLending - Unit 6 - Monitoring and Control of LendingKevin Us-LazPreces TimetoshineNo ratings yet

- Mgt201 Mega Midterm Solved Papers 321 PagesDocument328 pagesMgt201 Mega Midterm Solved Papers 321 Pageszahidwahla1100% (1)

- Chapter TWO FM I1Document65 pagesChapter TWO FM I1Embassy and NGO jobsNo ratings yet

- Corporate Finance Assignment 1 July To Sep BatchDocument9 pagesCorporate Finance Assignment 1 July To Sep BatchMadhu Patil G TNo ratings yet

- Principles of FinanceDocument19 pagesPrinciples of FinanceAvijit Dutta ShaonNo ratings yet

- Fin622 Solved Mcqs For Exam PreparationDocument9 pagesFin622 Solved Mcqs For Exam PreparationLareb ShaikhNo ratings yet

- Measuring and Evaluating Bank PerformanceDocument45 pagesMeasuring and Evaluating Bank PerformancepavithragowthamnsNo ratings yet

- Corporate Rating Methodology - FSADocument13 pagesCorporate Rating Methodology - FSAArsalan RafiqueNo ratings yet

- Midterm Examination Spring 2010 FIN622-Corporate Finance (Session - 6)Document4 pagesMidterm Examination Spring 2010 FIN622-Corporate Finance (Session - 6)Zeeshan AhamdNo ratings yet

- Chapter 1-OverviewDocument28 pagesChapter 1-OverviewAnanya SinghNo ratings yet

- Non-Performing Assets Asset and Liability Management by The: BanksDocument15 pagesNon-Performing Assets Asset and Liability Management by The: BanksCeline StuartNo ratings yet

- AMM 2008 LawrenceDocument18 pagesAMM 2008 LawrenceSoujanya NagarajaNo ratings yet

- Rethinking The Credit Liquidity Continuum - Neuberger Berman (2022)Document4 pagesRethinking The Credit Liquidity Continuum - Neuberger Berman (2022)sherNo ratings yet

- Working Capital Management in Reliance Industries LimitedDocument5 pagesWorking Capital Management in Reliance Industries LimitedVurdalack666No ratings yet

- The Most Boring Stock Investment Book FrameworkDocument16 pagesThe Most Boring Stock Investment Book FrameworkScorchNo ratings yet

- The Importance of DividendsDocument4 pagesThe Importance of Dividendssmartravian007No ratings yet

- MPAC604 Segments STUDENTSDocument51 pagesMPAC604 Segments STUDENTSKanokporn TangthamvanichNo ratings yet

- Credit Analysis and Distress PredictionDocument16 pagesCredit Analysis and Distress PredictionTarunima TabassumNo ratings yet

- mgt602 Solved MCQ - 'S From Final PapersDocument20 pagesmgt602 Solved MCQ - 'S From Final PapersMajid Shahzaad Kharral0% (1)

- Soal UTS Audit 1 19042021-1Document2 pagesSoal UTS Audit 1 19042021-1riski kilayNo ratings yet

- Tuca Zbarcea & Asociatii's Just in Case No. 5Document24 pagesTuca Zbarcea & Asociatii's Just in Case No. 5Tuca Zbarcea and AsociatiiNo ratings yet

- 02 F6 LRP Questions FA2009 PDFDocument44 pages02 F6 LRP Questions FA2009 PDFJino JoseNo ratings yet

- International Debt Statistics 2017Document199 pagesInternational Debt Statistics 2017Josue Antonio TrejoNo ratings yet

- Basis For Qualified OpinionDocument1 pageBasis For Qualified OpinionannNo ratings yet

- 3rd Sem MBADocument13 pages3rd Sem MBAmanju666666No ratings yet

- G.R. No. 130886Document6 pagesG.R. No. 130886Julian DubaNo ratings yet

- Palepu 3e - SM - Ch01 Class Exercise QuestionDocument2 pagesPalepu 3e - SM - Ch01 Class Exercise Questionnur zakirah0% (1)

- Examiners' Commentaries 2014: FN3092 Corporate FinanceDocument19 pagesExaminers' Commentaries 2014: FN3092 Corporate FinanceBianca KangNo ratings yet

- Income Tax Act Cap 470 Revised 2021-3-1Document224 pagesIncome Tax Act Cap 470 Revised 2021-3-1danielNo ratings yet

- Kba C. Guide English PDFDocument17 pagesKba C. Guide English PDFfelixmuyoveNo ratings yet

- Tenancy AgreementDocument4 pagesTenancy AgreementTamanna RanaNo ratings yet

- BBA 4year Termsystem PDFDocument44 pagesBBA 4year Termsystem PDFMuhammad SaadNo ratings yet

- Maar I MuthuDocument10 pagesMaar I MuthusamaadhuNo ratings yet

- PricelistDocument162 pagesPricelistNIT TEKSTILNo ratings yet

- Tax AssignmentDocument5 pagesTax AssignmentDiwakar AnandNo ratings yet

- Problems in Hypothesis TestingDocument8 pagesProblems in Hypothesis TestingsjaswanthNo ratings yet

- Accounting For Raw MaterialsDocument6 pagesAccounting For Raw MaterialsCorinne GohocNo ratings yet

- Accounting Professional: Corporate - Insolvency - CharteredDocument2 pagesAccounting Professional: Corporate - Insolvency - Charteredsamwilson0501No ratings yet

- Case Study - Nike Vs Adidas, Market and Comprehensive Competition AnalysisDocument12 pagesCase Study - Nike Vs Adidas, Market and Comprehensive Competition AnalysisHarris LuiNo ratings yet

- Indian Banking Sector ReformsDocument131 pagesIndian Banking Sector Reformsanikettt50% (2)

- Constitution Ya Mutungo Community AssociationDocument9 pagesConstitution Ya Mutungo Community AssociationRobert Baguma MwesigwaNo ratings yet