You might also like

- Tax and MSMEs in the Digital Age: Why Do We Need To Pay Taxes And What Are The Benefits For Us As MSME Entrepreneurs And How To Build Regulations That Are Empathetic And Proven To Encourage Tax Revenue In The Informal SectorFrom EverandTax and MSMEs in the Digital Age: Why Do We Need To Pay Taxes And What Are The Benefits For Us As MSME Entrepreneurs And How To Build Regulations That Are Empathetic And Proven To Encourage Tax Revenue In The Informal SectorNo ratings yet

- Exploring China's Tax Path Setting in The Context of Digital EconomyDocument11 pagesExploring China's Tax Path Setting in The Context of Digital EconomyInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Tool Kit for Tax Administration Management Information SystemFrom EverandTool Kit for Tax Administration Management Information SystemRating: 1 out of 5 stars1/5 (1)

- 2.what Challenges Does The Digital Economy Bring To AccountingDocument5 pages2.what Challenges Does The Digital Economy Bring To AccountingCarolNo ratings yet

- Ideas and Measures For Promoting Modernization ofDocument11 pagesIdeas and Measures For Promoting Modernization ofGeorgie SankoNo ratings yet

- Advantages and Disadvantages of Digitalisation in AccountingDocument6 pagesAdvantages and Disadvantages of Digitalisation in AccountingHannoun NouhailaNo ratings yet

- RetrieveDocument7 pagesRetrieveEsinam AdukpoNo ratings yet

- The Effectiveness of Tax Administration Digitalization To Reduce Compliance Cost Taxpayers of Micro Small, and Medium EnterprisesDocument8 pagesThe Effectiveness of Tax Administration Digitalization To Reduce Compliance Cost Taxpayers of Micro Small, and Medium EnterprisesElychia Roly PutriNo ratings yet

- Tax Issues On Digital EconomyDocument39 pagesTax Issues On Digital Economyjade100% (1)

- Tax Law, SubhamDocument9 pagesTax Law, SubhamSugam AgrawalNo ratings yet

- Reaction PaperDocument10 pagesReaction PaperpriyaNo ratings yet

- 2.+performance+and+risks 38Document5 pages2.+performance+and+risks 38Ionela RoscaNo ratings yet

- The Digital Economy in Developing Countries - Challenges and OpportunitiesDocument6 pagesThe Digital Economy in Developing Countries - Challenges and OpportunitiesTrần Thị Mai AnhNo ratings yet

- Seminar 11 Introduction and Demonstration of Finance and Taxation System& Discussion 5 The Best Practice Case of Tax DigitizationDocument51 pagesSeminar 11 Introduction and Demonstration of Finance and Taxation System& Discussion 5 The Best Practice Case of Tax DigitizationPoun GerrNo ratings yet

- Ey Tax Technology TransformationDocument32 pagesEy Tax Technology TransformationTejas SodhaNo ratings yet

- Seminar 9 The Best Practice Case of Tax DigitizationDocument87 pagesSeminar 9 The Best Practice Case of Tax DigitizationPoun GerrNo ratings yet

- Optimizing Income Tax and Value Added Tax On E-Commerce TransactionDocument10 pagesOptimizing Income Tax and Value Added Tax On E-Commerce TransactionHanyfah ArifiaNo ratings yet

- Digital IndiaDocument4 pagesDigital IndiaGamers N2No ratings yet

- Tax FinalDocument3 pagesTax FinalMohammad AliNo ratings yet

- WS 6Document11 pagesWS 6Luis DiasNo ratings yet

- The Impact of Information Technology On Accounting and Finance 1Document12 pagesThe Impact of Information Technology On Accounting and Finance 1Samsung IphoneNo ratings yet

- TAXATION MANAGEMENT IN THE DIGITAL ECONOMIC ERA (Submit)Document10 pagesTAXATION MANAGEMENT IN THE DIGITAL ECONOMIC ERA (Submit)Multi BudiNo ratings yet

- Using Information Technology To Improve Tax and Revenue CollectionDocument35 pagesUsing Information Technology To Improve Tax and Revenue Collectionalex_603530016No ratings yet

- Challenges and Solutions of Digital Assets To China's Tax SystemDocument5 pagesChallenges and Solutions of Digital Assets To China's Tax SystemaijbmNo ratings yet

- Pajak EcommerceDocument15 pagesPajak EcommerceAlvin JeremiaNo ratings yet

- Tax Administration Indonesia IJMSSSR00616Document13 pagesTax Administration Indonesia IJMSSSR00616Ayu ChotibahNo ratings yet

- SSRN-id3467998Document27 pagesSSRN-id3467998apple pastaNo ratings yet

- A Study of B2B E-Market in ChinaDocument7 pagesA Study of B2B E-Market in ChinaVinothNo ratings yet

- Blockchain Technology Application For Value-Added Tax SystemsDocument27 pagesBlockchain Technology Application For Value-Added Tax SystemsGeysa Pratama EriatNo ratings yet

- 22 - IJEFI9071tambunanokeyDocument7 pages22 - IJEFI9071tambunanokeyapple pastaNo ratings yet

- Vietnam National Strategy For Development of Digital EconomyDocument6 pagesVietnam National Strategy For Development of Digital Economythanhthuytruongngoc121No ratings yet

- 1 SMDocument12 pages1 SMAngela Fye LlagasNo ratings yet

- The Pandemic Era Digital Economy Youth Challenges in Social Media MarketingDocument7 pagesThe Pandemic Era Digital Economy Youth Challenges in Social Media MarketingFarah LimNo ratings yet

- Informatics 09 00019Document17 pagesInformatics 09 00019nqa1994No ratings yet

- Kofler, Georg and Sinning, Julia - Equalization Taxes and The EU DSTDocument25 pagesKofler, Georg and Sinning, Julia - Equalization Taxes and The EU DSTJenny NatividadNo ratings yet

- Towards The Digitisation of The Nigerian Tax Administration Challenges and Prospects-1Document7 pagesTowards The Digitisation of The Nigerian Tax Administration Challenges and Prospects-1Rasheed LawalNo ratings yet

- Fostering Tax Compliance in RDC: Lesson From Korean Case StudyDocument13 pagesFostering Tax Compliance in RDC: Lesson From Korean Case StudyInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- GST ProjectDocument80 pagesGST ProjectBalaram DharaNo ratings yet

- Mullis Taxing Developing Asias deDocument44 pagesMullis Taxing Developing Asias deFredy LlaqueNo ratings yet

- Position Paper On Internet Transactions Act - As of 12 Feb 2021 (v3)Document26 pagesPosition Paper On Internet Transactions Act - As of 12 Feb 2021 (v3)BlogWatchNo ratings yet

- Management Accounting in The Era of Big Data: Yutong YanDocument6 pagesManagement Accounting in The Era of Big Data: Yutong YanFeri HarnandoNo ratings yet

- Digital Accounting Implementation and Audit Performance - An Empirical Research of Tax Auditors in ThailandDocument11 pagesDigital Accounting Implementation and Audit Performance - An Empirical Research of Tax Auditors in ThailandChaima LejriNo ratings yet

- Written SampleDocument2 pagesWritten Sampleayankhan1294No ratings yet

- Dani's TaxDocument5 pagesDani's TaxNatnhael WondafrashNo ratings yet

- Ime James Sawyer Digitalisation of Tax PaperDocument25 pagesIme James Sawyer Digitalisation of Tax PaperSue AnneNo ratings yet

- 29 29 Project Report On e Commerce Digital SignatureDocument69 pages29 29 Project Report On e Commerce Digital Signaturesushantchauhan24No ratings yet

- Mobile World Congress 2014Document2 pagesMobile World Congress 2014Ahmad AbbaNo ratings yet

- Digitalization and Efficiency of The Beninese Tax AdministrationDocument7 pagesDigitalization and Efficiency of The Beninese Tax AdministrationInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- WEF Accelerating Digital Payments in Latin America and The Caribbean 2022Document28 pagesWEF Accelerating Digital Payments in Latin America and The Caribbean 2022Fernando HernandezNo ratings yet

- Dissertation Draft - 1Document15 pagesDissertation Draft - 1Mahima DoshiNo ratings yet

- FIM ReportDocument16 pagesFIM Reportmanhal siddiquiNo ratings yet

- 8 Tax Science DirectDocument15 pages8 Tax Science DirectMehrinigorNo ratings yet

- The Factors Affecting Digital Transformation in Vietnam Logistics EnterprisesDocument19 pagesThe Factors Affecting Digital Transformation in Vietnam Logistics EnterprisestuanNo ratings yet

- Step 2: Collaborative Work Valuation and Negotiation of Technology 212032 - 8Document10 pagesStep 2: Collaborative Work Valuation and Negotiation of Technology 212032 - 8maikolNo ratings yet

- Technology, Media and Telecom (TMT) : Online Businesses and Disruptive Technologies - Key India Tax and Regulatory AspectsDocument33 pagesTechnology, Media and Telecom (TMT) : Online Businesses and Disruptive Technologies - Key India Tax and Regulatory AspectsSunny KhavleNo ratings yet

- RSM India White Paper - Taxation of Businesses in Digital EraDocument13 pagesRSM India White Paper - Taxation of Businesses in Digital EraanandarchayaNo ratings yet

- Digitalisation and Trade: What Hope For Lower Income Countries?Document33 pagesDigitalisation and Trade: What Hope For Lower Income Countries?Dr Nidhi GoyalNo ratings yet

- E-Commerce: A New Tool in Tax EvasionDocument8 pagesE-Commerce: A New Tool in Tax Evasionsohalsingh1No ratings yet

- AGI Technology-Impact On Asian Finance 2013Document34 pagesAGI Technology-Impact On Asian Finance 2013sdenkaspNo ratings yet

- Varshitha (1HK19IS082) Online MoneyDocument22 pagesVarshitha (1HK19IS082) Online MoneyS VarshithaNo ratings yet

- Introduction To DerivativesDocument14 pagesIntroduction To Derivativesking410No ratings yet

- Mid-Term Review of The ASEAN Strategic Action Plan For SME Development 2016 - 2025Document33 pagesMid-Term Review of The ASEAN Strategic Action Plan For SME Development 2016 - 2025ducvaNo ratings yet

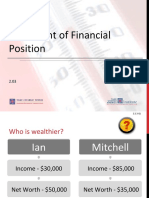

- Financial PositionDocument31 pagesFinancial PositionhaftamuNo ratings yet

- 06 Calculating NPV ShellDocument1 page06 Calculating NPV ShellSyed TabrezNo ratings yet

- Buy Verified CashApp AccountDocument7 pagesBuy Verified CashApp AccountSchmidt Christina100% (2)

- Annual Income Statement Report Name: Laporan Laba Rugi / Nama / Ery Abd Nasir PelupessyDocument2 pagesAnnual Income Statement Report Name: Laporan Laba Rugi / Nama / Ery Abd Nasir PelupessyErry Abdul Nasir PelupessyNo ratings yet

- World Map: Middle East Europe Africa Asia North America Central, South America South West PacificDocument32 pagesWorld Map: Middle East Europe Africa Asia North America Central, South America South West Pacificvenkat100% (1)

- R&P 1983 Rules Wise & GAR FormsDocument8 pagesR&P 1983 Rules Wise & GAR FormsSebastian Mangneo KukiNo ratings yet

- Baby Doge: WhitepaperDocument14 pagesBaby Doge: WhitepaperReezQeyNo ratings yet

- Methods of International Trade and Payments: The Nigerian Perspective Dr. AGBONIKA Josephine Aladi AchorDocument40 pagesMethods of International Trade and Payments: The Nigerian Perspective Dr. AGBONIKA Josephine Aladi AchorYesyit BerhanuNo ratings yet

- Baf2102 Cost Accounting Cat I and II DibelDocument2 pagesBaf2102 Cost Accounting Cat I and II DibelcyrusNo ratings yet

- Case BoilotDocument9 pagesCase BoilotTara HastuNo ratings yet

- Modular Costing - Rev 2Document2 pagesModular Costing - Rev 2Muhammad ZulfamiNo ratings yet

- ContempDocument3 pagesContempJeko Betguen PalangiNo ratings yet

- Muhammad Qaiser HBL ReportDocument21 pagesMuhammad Qaiser HBL Reportm qaiserNo ratings yet

- Employee's Information FormDocument1 pageEmployee's Information FormLyle RabasanoNo ratings yet

- BRS Sample Card FormatDocument50 pagesBRS Sample Card FormatJezreel FlotildeNo ratings yet

- 13 - Kotak Mahindra Bank - Banking IndustryDocument3 pages13 - Kotak Mahindra Bank - Banking IndustryDivyanshu JoshiNo ratings yet

- 0708 Valentine's Day Online Problem SetDocument2 pages0708 Valentine's Day Online Problem SetVăn Luân VũNo ratings yet

- 3-Statement Model (Complete)Document16 pages3-Statement Model (Complete)James BondNo ratings yet

- SG 2602Document86 pagesSG 2602Violet PurpleNo ratings yet

- Problems Chapter 3Document5 pagesProblems Chapter 3trangnha1505No ratings yet

- Ard 140Document2 pagesArd 140Rakhimane67% (3)

- Globalization Is The Word Used To Describe The Growing Interdependence of The World's Economies, CulturesDocument17 pagesGlobalization Is The Word Used To Describe The Growing Interdependence of The World's Economies, CulturesKiandumaNo ratings yet

- Resilient PreppingDocument157 pagesResilient PreppingLIBRERIA GRNo ratings yet

- Section VII Form of Bid, Appendix To Bid and Bid Security (ERA 2012 EC V .1)Document16 pagesSection VII Form of Bid, Appendix To Bid and Bid Security (ERA 2012 EC V .1)Solomon MehariNo ratings yet

- 2016 Ghana Club 100 ListDocument4 pages2016 Ghana Club 100 ListSamuel Bruce Rockson0% (1)

- Ewb 1738 20222023 24addpt2610d1z3Document1 pageEwb 1738 20222023 24addpt2610d1z3Aashish TibrewalNo ratings yet

- Function ConvertCurrencyToEnglishDocument8 pagesFunction ConvertCurrencyToEnglishAmit Kumar PaulNo ratings yet

- ACB (India) LimitedDocument2 pagesACB (India) LimitedSurajPandeyNo ratings yet