You might also like

- Ohada Accounting PlanDocument72 pagesOhada Accounting PlanNchendeh Christian100% (3)

- Advanced Accounting Chapter 1Document11 pagesAdvanced Accounting Chapter 1Nellie Panedy80% (15)

- Government Accounting TheoriesDocument6 pagesGovernment Accounting TheoriesHazel Jumaquio100% (7)

- Ch4 SolutionsDocument23 pagesCh4 SolutionsFahad Batavia100% (1)

- CH 4Document12 pagesCH 4Miftahudin Miftahudin0% (1)

- Imperial Administrative Records, Part IDocument323 pagesImperial Administrative Records, Part IHECTOR ORTEGANo ratings yet

- Adam Ltd Financial AnalysisDocument3 pagesAdam Ltd Financial AnalysisRegina AtkinsNo ratings yet

- Accounts Financial Ratios of KFCDocument20 pagesAccounts Financial Ratios of KFCMalathi Sundrasaigaran91% (11)

- Chapter 1 - Excercises Solutions Part ADocument8 pagesChapter 1 - Excercises Solutions Part AHECTOR ORTEGANo ratings yet

- Dev Financial Analysis-2Document8 pagesDev Financial Analysis-2Adam BelmekkiNo ratings yet

- CH 1 - End of Chapter Exercises SolutionsDocument37 pagesCH 1 - End of Chapter Exercises SolutionssaraNo ratings yet

- Financial ReportsDocument36 pagesFinancial ReportsbehanzinlufrancheNo ratings yet

- Accounting..... All Questions & Answer.Document13 pagesAccounting..... All Questions & Answer.MehediNo ratings yet

- FABM2 Module 5 Cash Flow StatementDocument12 pagesFABM2 Module 5 Cash Flow StatementLoriely De GuzmanNo ratings yet

- Financial Statements: An OverviewDocument34 pagesFinancial Statements: An OverviewMUSTAFA KAMAL BIN ABD MUTALIP / BURSAR100% (1)

- Chapters 1 and 2Document36 pagesChapters 1 and 2Qing ShiNo ratings yet

- Chapter 1 Lecture Notes: I. Forms of Business OrganizationDocument8 pagesChapter 1 Lecture Notes: I. Forms of Business OrganizationvirtualtadNo ratings yet

- jp02 Financial-Statements - BWDocument2 pagesjp02 Financial-Statements - BWJinwon KimNo ratings yet

- 2024 - Week 3 - Comm 217 Notes - Ch03Student 1to UploadDocument13 pages2024 - Week 3 - Comm 217 Notes - Ch03Student 1to Uploadsamuelrodriguezch12No ratings yet

- Mod4 Part 1 Essence of Financial StatementsDocument16 pagesMod4 Part 1 Essence of Financial StatementsAngeline de SagunNo ratings yet

- AccountingDocument34 pagesAccountingdr.a.youssryNo ratings yet

- CHAPTER 11 - AnswerDocument16 pagesCHAPTER 11 - Answernash100% (1)

- Module 2 - Assessing Financial Health of The Firm - Week 2 4Document14 pagesModule 2 - Assessing Financial Health of The Firm - Week 2 4maelyn calindongNo ratings yet

- Income Statement To The NetDocument26 pagesIncome Statement To The NetOman SherNo ratings yet

- Chapter IXDocument3 pagesChapter IXCleo IlaoNo ratings yet

- Topic 4rev StudentsDocument31 pagesTopic 4rev StudentsNemalai VitalNo ratings yet

- Topic 4rev (Students)Document30 pagesTopic 4rev (Students)RomziNo ratings yet

- Chapter IXDocument3 pagesChapter IXCleo IlaoNo ratings yet

- Fabm 2Document7 pagesFabm 2Akaashi KeijiNo ratings yet

- Interpreting and Analyzing Financial Statements 6th Edition Schoenebeck Solutions ManualDocument36 pagesInterpreting and Analyzing Financial Statements 6th Edition Schoenebeck Solutions Manualbobsilvaka0el100% (24)

- Supplementary Exercises Chapter 1-3Document4 pagesSupplementary Exercises Chapter 1-3Smey MNo ratings yet

- Financial Statements: An OverviewDocument41 pagesFinancial Statements: An OverviewGaluh Boga Kuswara100% (1)

- CF Lecture 0 Working With FS v1Document51 pagesCF Lecture 0 Working With FS v1Tâm NhưNo ratings yet

- Learn key financial statementsDocument36 pagesLearn key financial statementsNemalai VitalNo ratings yet

- Wealth Managment 1Document73 pagesWealth Managment 1dashashutosh87No ratings yet

- Understanding Financial Statements For Non-AccountantsDocument5 pagesUnderstanding Financial Statements For Non-AccountantsAngella RiveraNo ratings yet

- Week 2 Lesson in Business Finance.2Document36 pagesWeek 2 Lesson in Business Finance.2jane caranguianNo ratings yet

- Chapter 11 Capital N SurplusDocument12 pagesChapter 11 Capital N SurplusCiciNo ratings yet

- Unit 2 Uderstanding Financial StatementsDocument23 pagesUnit 2 Uderstanding Financial StatementsSG dNo ratings yet

- Chapter 9 - BookDocument6 pagesChapter 9 - BookCheskaNo ratings yet

- Balance SheetDocument32 pagesBalance SheetJanine padronesNo ratings yet

- Chapter 5Document8 pagesChapter 5Jimmy LojaNo ratings yet

- Outcome. 3Document24 pagesOutcome. 3Sohel MemonNo ratings yet

- Important Points 1. 2. 3. 4. 5. 6. 7Document15 pagesImportant Points 1. 2. 3. 4. 5. 6. 7RAVI KUMARNo ratings yet

- Bus 103 AccountingDocument3 pagesBus 103 AccountingDyne Morte0% (1)

- accounting(分享版)Document7 pagesaccounting(分享版)Siyang QuNo ratings yet

- Dwnload Full Interpreting and Analyzing Financial Statements 6th Edition Schoenebeck Solutions Manual PDFDocument36 pagesDwnload Full Interpreting and Analyzing Financial Statements 6th Edition Schoenebeck Solutions Manual PDFphumilorlyna100% (12)

- ch1 HandoutDocument6 pagesch1 HandoutPaolo TipoNo ratings yet

- Exercises For Chapter 23 EFA2Document13 pagesExercises For Chapter 23 EFA2tuananh leNo ratings yet

- FM Testbank Ch03Document18 pagesFM Testbank Ch03David LarryNo ratings yet

- ACCOUNTING PROCESS and CLASSIFICATIONDocument26 pagesACCOUNTING PROCESS and CLASSIFICATIONvdhanyamrajuNo ratings yet

- 7 The Accounting Equation (4 Pages)Document4 pages7 The Accounting Equation (4 Pages)Danica MamontayaoNo ratings yet

- Q- CHAPTER 2Document11 pagesQ- CHAPTER 2phuonganh020804No ratings yet

- Acct CH1Document10 pagesAcct CH1j8noelNo ratings yet

- Funds Flow Theory PDFDocument7 pagesFunds Flow Theory PDFLalrinfela RalteNo ratings yet

- The Five Financial Statements Based On IFRSDocument12 pagesThe Five Financial Statements Based On IFRSAngel GraceNo ratings yet

- Exercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotDocument15 pagesExercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotCherry Doong CuantiosoNo ratings yet

- Chapter 2 Basic Financial StatementsDocument34 pagesChapter 2 Basic Financial StatementsZemene HailuNo ratings yet

- Understanding Balance SheetsDocument26 pagesUnderstanding Balance SheetsAli AhmedNo ratings yet

- Chapter 1 Introduction To FSADocument11 pagesChapter 1 Introduction To FSALuu Nhat MinhNo ratings yet

- 12TH CH-7 Not For Profit Organisation - 123Document55 pages12TH CH-7 Not For Profit Organisation - 123LalitKukrejaNo ratings yet

- Exercises For Chapter 23 EFA2Document16 pagesExercises For Chapter 23 EFA2Thu LoanNo ratings yet

- Cfs - Lecture Notes - Updated 2023Document49 pagesCfs - Lecture Notes - Updated 2023Thanh Uyên100% (1)

- Unit 4 Understanding Financial Statements: StructureDocument32 pagesUnit 4 Understanding Financial Statements: StructureTushar SharmaNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- Small Change in Hellenistic Roman GalileDocument18 pagesSmall Change in Hellenistic Roman GalileHECTOR ORTEGANo ratings yet

- MALIK The Corrections of Codex Sinaiticus and The Textual Transmission of Revelation Josef Schmid Revisited RevisedDocument27 pagesMALIK The Corrections of Codex Sinaiticus and The Textual Transmission of Revelation Josef Schmid Revisited RevisedHECTOR ORTEGANo ratings yet

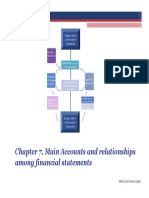

- 6 ELE Chapter 7. Relationships Among Financial StatementsDocument39 pages6 ELE Chapter 7. Relationships Among Financial StatementsHECTOR ORTEGANo ratings yet

- 4 ELE Chapter 6 y 4. Profitability and Return Ratios (B)Document28 pages4 ELE Chapter 6 y 4. Profitability and Return Ratios (B)HECTOR ORTEGANo ratings yet

- Chapter 1 - Exercises Part BDocument7 pagesChapter 1 - Exercises Part BHECTOR ORTEGANo ratings yet

- The Jewish People Jesus ChristDocument312 pagesThe Jewish People Jesus ChristHECTOR ORTEGA100% (1)

- 1 Timothy 4, Photo Companion BiblePlacesDocument67 pages1 Timothy 4, Photo Companion BiblePlacesHECTOR ORTEGANo ratings yet

- Paul's Teachings on Spiritual PowersDocument201 pagesPaul's Teachings on Spiritual PowersHECTOR ORTEGA100% (3)

- Textual Resarch On The Bible (Pruebas de Investigación Sobre La Biblia) PDFDocument32 pagesTextual Resarch On The Bible (Pruebas de Investigación Sobre La Biblia) PDFIng. Bendryx BelloNo ratings yet

- History of the Babylonians and AssyriansDocument242 pagesHistory of the Babylonians and AssyriansHECTOR ORTEGANo ratings yet

- 369441-Text de L'article-532360-1-10-20200602Document40 pages369441-Text de L'article-532360-1-10-20200602HECTOR ORTEGANo ratings yet

- 2018 The Nude at The Entrance ContextualDocument23 pages2018 The Nude at The Entrance ContextualHECTOR ORTEGANo ratings yet

- 279 The Use of The Earliest Greek ScriptDocument20 pages279 The Use of The Earliest Greek ScriptHECTOR ORTEGANo ratings yet

- Greek Biblical Manuscripts from the Judean Desert CavesDocument28 pagesGreek Biblical Manuscripts from the Judean Desert CavesHECTOR ORTEGANo ratings yet

- The Correspondence of Sargon II, Part IIDocument319 pagesThe Correspondence of Sargon II, Part IIHECTOR ORTEGANo ratings yet

- Harry: Parallels,&dquo Religious UniversityDocument1 pageHarry: Parallels,&dquo Religious UniversityHECTOR ORTEGANo ratings yet

- Kosher Fat: Mony Almalech (NBU)Document47 pagesKosher Fat: Mony Almalech (NBU)HECTOR ORTEGANo ratings yet

- First Paperback!: Must' For Christian Alike. - Tin: York Times Celebration The Stories, Traditions, LegendsDocument548 pagesFirst Paperback!: Must' For Christian Alike. - Tin: York Times Celebration The Stories, Traditions, LegendsHECTOR ORTEGANo ratings yet

- S ChaserDocument329 pagesS ChaserHECTOR ORTEGANo ratings yet

- BM Finance Notes PDFDocument10 pagesBM Finance Notes PDFApurva SunejaNo ratings yet

- 1 CombinedDocument405 pages1 CombinedMansi aggarwal 171050No ratings yet

- EC029 - A - Fixed Assets Setup & Common Data - v11.00Document14 pagesEC029 - A - Fixed Assets Setup & Common Data - v11.00Ariel SpallettiNo ratings yet

- Afar ReviewDocument7 pagesAfar Reviewhos hiNo ratings yet

- F7.2 - Mock Test 1Document5 pagesF7.2 - Mock Test 1huusinh2402No ratings yet

- Cash To Accrual ProblemsDocument10 pagesCash To Accrual ProblemsAmethystNo ratings yet

- Financial Analysis of Hòa Phát Group Joint Stock CompanyDocument36 pagesFinancial Analysis of Hòa Phát Group Joint Stock CompanySang NguyễnNo ratings yet

- Financial analysis of Deepak Fertilizers and Petrochemicals Corporation Limited (DFPCLDocument13 pagesFinancial analysis of Deepak Fertilizers and Petrochemicals Corporation Limited (DFPCLSiddharth Rohilla (M22MS074)No ratings yet

- L5 DipBM - Assignment Briefs - September 2021Document24 pagesL5 DipBM - Assignment Briefs - September 2021Umar AliNo ratings yet

- Horton Building Supplies: Final ProjectDocument11 pagesHorton Building Supplies: Final ProjectIbrah YusalNo ratings yet

- BCIBF-103 Financial AccountingDocument423 pagesBCIBF-103 Financial AccountingS.M Documents SolutionsNo ratings yet

- Marketing PlanDocument15 pagesMarketing PlanMichael HardingNo ratings yet

- Financial Analysis Spreadsheet From The Kaplan GroupDocument4 pagesFinancial Analysis Spreadsheet From The Kaplan GroupPrince AdyNo ratings yet

- Topic 1 Introduction To Corporate FinanceDocument26 pagesTopic 1 Introduction To Corporate FinancelelouchNo ratings yet

- Chapter 5Document47 pagesChapter 5Aira Nhaira MecateNo ratings yet

- Difference Between Capital Expenditure and Revenue ExpenditureDocument6 pagesDifference Between Capital Expenditure and Revenue ExpenditureRoopkishore SharmaNo ratings yet

- Parle GDocument112 pagesParle Gdeepak Gupta100% (1)

- Morgan Marie Leasing Company Signs An Agreement On January 1Document1 pageMorgan Marie Leasing Company Signs An Agreement On January 1M Bilal SaleemNo ratings yet

- Balance Sheet of State Bank of IndiaDocument8 pagesBalance Sheet of State Bank of IndiaJyoti VijayNo ratings yet

- J.Karthik Receivables ManagementDocument93 pagesJ.Karthik Receivables Managementpeter sumanthNo ratings yet

- On GoodwillDocument23 pagesOn GoodwillNabanita GhoshNo ratings yet

- Trial Balance Home Office DR (CR) Branch Office DR (CR)Document2 pagesTrial Balance Home Office DR (CR) Branch Office DR (CR)Adriana CarinanNo ratings yet

- IBM's capital structure and financing policiesDocument17 pagesIBM's capital structure and financing policiesJenny Zulay SUAREZ SOLANONo ratings yet

- CH 11 Practice MCQ - S Financial Management by BrighamDocument49 pagesCH 11 Practice MCQ - S Financial Management by BrighamShahmir AliNo ratings yet

- 17 Answers To All ProblemsDocument25 pages17 Answers To All ProblemsRaşitÖnerNo ratings yet