You might also like

- Negotiable InstrumentsDocument5 pagesNegotiable InstrumentsDhruv LawaniyaNo ratings yet

- What Is A Negotiable InstrumentDocument17 pagesWhat Is A Negotiable InstrumentRodolfo CorpuzNo ratings yet

- Commercial Law Group WorkDocument60 pagesCommercial Law Group WorkesmuraguNo ratings yet

- Material 214Document22 pagesMaterial 214AmbroseNo ratings yet

- Business Law Cat..Document21 pagesBusiness Law Cat..jimkuria90No ratings yet

- Baf 2105 CatDocument21 pagesBaf 2105 Catjimkuria90No ratings yet

- Negotiable InstrumentsDocument2 pagesNegotiable InstrumentsDESMOND EZIEKENo ratings yet

- ML Unit-3Document11 pagesML Unit-3AkshayNo ratings yet

- Jannel Yza S. Gunida Bsba - Iv Negotiation Lecture I. Preliminary Subject - Matter On Negotiation A. Most Common Forms of Negotiable InstrumentDocument6 pagesJannel Yza S. Gunida Bsba - Iv Negotiation Lecture I. Preliminary Subject - Matter On Negotiation A. Most Common Forms of Negotiable Instrumentyza gunidaNo ratings yet

- Credit Collection Module 2Document9 pagesCredit Collection Module 2Crystal Jade Apolinario RefilNo ratings yet

- Chapter 5 Bank Credit InstrumentsDocument5 pagesChapter 5 Bank Credit InstrumentsMariel Crista Celda Maravillosa100% (2)

- Credit InstrumentsDocument39 pagesCredit InstrumentsRevanth Nannapaneni100% (1)

- Chapter 9: Credit Instruments ObjectivesDocument43 pagesChapter 9: Credit Instruments ObjectiveskatlicNo ratings yet

- Bank of America Matter Banking ConceptsDocument8 pagesBank of America Matter Banking ConceptsJithendar ReddyNo ratings yet

- Banking Law AssignmentDocument16 pagesBanking Law AssignmentAmbrose YollahNo ratings yet

- Chapter 5 - Bank Credit InstrumentsDocument5 pagesChapter 5 - Bank Credit InstrumentsMhaiNo ratings yet

- Adverse Selection & Moral HazardDocument4 pagesAdverse Selection & Moral HazardAJAY KUMAR SAHUNo ratings yet

- Letter of Credit UpdatedDocument17 pagesLetter of Credit UpdatedKobir HasanNo ratings yet

- Credit Instruments Power PointDocument11 pagesCredit Instruments Power PointEd Leen Ü80% (10)

- Methods of Payment in Export ImportDocument10 pagesMethods of Payment in Export Importkaran singlaNo ratings yet

- Difference Between Bill of Exchange and Letter of CreditDocument2 pagesDifference Between Bill of Exchange and Letter of CreditShirleyNo ratings yet

- Import Export Policy Procedure Assignment 2Document6 pagesImport Export Policy Procedure Assignment 2TsinatNo ratings yet

- Instruments of Exchange and PaymentDocument3 pagesInstruments of Exchange and PaymentAnnika liburdNo ratings yet

- Instruments of Dddexchange (Payment Methods)Document1 pageInstruments of Dddexchange (Payment Methods)Monique McfarlaneNo ratings yet

- Bank Funds SourcesDocument8 pagesBank Funds Sourceskhairul1286No ratings yet

- BOE Vs LOCDocument3 pagesBOE Vs LOCIndraneel GurjarNo ratings yet

- Promises To Pay Versus Order To PayDocument1 pagePromises To Pay Versus Order To Paylou merphy castilloNo ratings yet

- Research Letter of CreditDocument15 pagesResearch Letter of Creditefaf007No ratings yet

- Banking Law - Negotiable Instruments & It's TypesDocument3 pagesBanking Law - Negotiable Instruments & It's TypesAmogha Gadkar100% (1)

- Introduction of Banking InstrumentsDocument15 pagesIntroduction of Banking InstrumentstriratnacomNo ratings yet

- CheckDocument3 pagesCheckGerman CastillaNo ratings yet

- Bankingtheorylawpracticeunitiiippt 240307181015 7e5977faDocument29 pagesBankingtheorylawpracticeunitiiippt 240307181015 7e5977fadharshan0425No ratings yet

- International TradeDocument2 pagesInternational TradeSheikh SadiNo ratings yet

- Module 2 Credit - CollectionDocument14 pagesModule 2 Credit - CollectionAicarl JimenezNo ratings yet

- Bank Credit Instruments-Fm122Document27 pagesBank Credit Instruments-Fm122Jade Solante Cervantes100% (1)

- Credit Department: The Nature of CreditDocument5 pagesCredit Department: The Nature of CreditFahadNo ratings yet

- CC Chap 5Document9 pagesCC Chap 520100131No ratings yet

- 112.CCE - Definition of CCE ItemsDocument2 pages112.CCE - Definition of CCE ItemsAngeliePanerioGonzagaNo ratings yet

- 6th ChapterDocument21 pages6th ChapterFizza Masroor - 64No ratings yet

- Itab RevieweerDocument13 pagesItab RevieweerAra PanganibanNo ratings yet

- School of Civil Engineering: Construction Costing and Finance Management Topic - Letter of CreditDocument10 pagesSchool of Civil Engineering: Construction Costing and Finance Management Topic - Letter of CreditTaimoor NasserNo ratings yet

- Credit Instrument - It Is A Document That Proves The Existence of A Credit Obligation ThatDocument3 pagesCredit Instrument - It Is A Document That Proves The Existence of A Credit Obligation ThatKlester Kim Sauro ZitaNo ratings yet

- Assignment in Credit TransactionsDocument17 pagesAssignment in Credit TransactionsNica09_forever100% (1)

- Types of Negotiable InstrumentDocument3 pagesTypes of Negotiable Instrumentanon_919197283No ratings yet

- New Microsoft Office Word DocumentDocument12 pagesNew Microsoft Office Word DocumentKamran ButtNo ratings yet

- What Are Cheques ReportDocument7 pagesWhat Are Cheques ReportROMMIL BALLENOSNo ratings yet

- Assignment 2 LC, CAD and Documentation.Document12 pagesAssignment 2 LC, CAD and Documentation.TaddesseNo ratings yet

- Definition of 'Underwriting ': Payment Card PaymentDocument4 pagesDefinition of 'Underwriting ': Payment Card PaymentDu JonNo ratings yet

- Instruments of PaymentsDocument3 pagesInstruments of Paymentsninamekdad09No ratings yet

- Credit and Collection Week 11Document47 pagesCredit and Collection Week 11ephesians320laiNo ratings yet

- Negotiation and EndorsementDocument23 pagesNegotiation and EndorsementpatriciaNo ratings yet

- Importants of Letter of CreditDocument3 pagesImportants of Letter of CreditUnEeb WaSeemNo ratings yet

- Import Export Policy Procedure Assignment 22Document5 pagesImport Export Policy Procedure Assignment 22TsinatNo ratings yet

- Letter of Credit (Notes)Document2 pagesLetter of Credit (Notes)Alisha TiuNo ratings yet

- Trade - Intermediate LevelDocument202 pagesTrade - Intermediate Levelsnigdha biswasNo ratings yet

- Credit and Collection PrelimsDocument7 pagesCredit and Collection PrelimsMeloy ApiladoNo ratings yet

- Letter of CreditDocument35 pagesLetter of CreditYash AdukiaNo ratings yet

- The Payment System and Financial InstrumentsDocument27 pagesThe Payment System and Financial InstrumentsAllen GonzagaNo ratings yet

- Presentation On Financial InstrumentsDocument20 pagesPresentation On Financial InstrumentsMehak BhallaNo ratings yet

- Cryptography SlidesDocument14 pagesCryptography Slidesdeepalisharma100% (4)

- 21 870 Campbelltown To Liverpool Via Glenfield 20230925 20231007 1Document6 pages21 870 Campbelltown To Liverpool Via Glenfield 20230925 20231007 1Neng RegsNo ratings yet

- TosDocument2 pagesTosamjad khanNo ratings yet

- E BankingDocument19 pagesE BankingramyaNo ratings yet

- Bath & Body Works Gift Card PageDocument1 pageBath & Body Works Gift Card Pageviswa tejNo ratings yet

- UntitledDocument8 pagesUntitledPreeti SinghNo ratings yet

- Codes Xtream IPTV - 2023-2024 VIP Premium Date 12-2023 Group - 21Document197 pagesCodes Xtream IPTV - 2023-2024 VIP Premium Date 12-2023 Group - 21kamelbh956No ratings yet

- RQCV HUBo Z4681 J EZDocument8 pagesRQCV HUBo Z4681 J EZSACHNo ratings yet

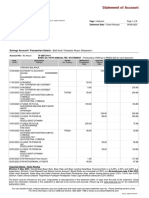

- Transaction HistoryDocument3 pagesTransaction HistorysomeshleocolaNo ratings yet

- Water Bill P1Document1 pageWater Bill P1Yu FengNo ratings yet

- FormatDocument4 pagesFormatPriya AswaniNo ratings yet

- Screenshot 2023-06-16 at 10.17.17 AMDocument12 pagesScreenshot 2023-06-16 at 10.17.17 AMPatel KevalNo ratings yet

- Victor Owusu: Account StatementDocument2 pagesVictor Owusu: Account Statementploteg66No ratings yet

- Sbi StatementDocument5 pagesSbi Statement321910303040 gitamNo ratings yet

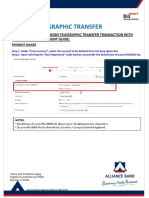

- How To Perform Foreign Telegraphic TransferDocument33 pagesHow To Perform Foreign Telegraphic TransferBerney RyxlerNo ratings yet

- AcevedoBeltinvoice 1545 PDFDocument3 pagesAcevedoBeltinvoice 1545 PDFAndres Felipe Briceño RodriguezNo ratings yet

- 1 Aug 22 - 27 Jan 22Document42 pages1 Aug 22 - 27 Jan 22Anurag SinghNo ratings yet

- Digi1: M/S. Digi1 Electronics Pvt. LTDDocument1 pageDigi1: M/S. Digi1 Electronics Pvt. LTDpratik.upadhyay950No ratings yet

- Epayment SeminarDocument5 pagesEpayment Seminardheeraj_ddNo ratings yet

- Bob SsaDocument1 pageBob Ssaranbir9drNo ratings yet

- Bank StatementsDocument12 pagesBank Statementsahisah azizan2000No ratings yet

- RRB Technician PapersDocument10 pagesRRB Technician PapersHaripriya VuyyalaNo ratings yet

- Estatement20230609 000350816Document8 pagesEstatement20230609 000350816Dila WwfNo ratings yet

- Banking Terminology - 1Document2 pagesBanking Terminology - 1Nayanshri NishadNo ratings yet

- IGNOU - Examination Form AcknowledgementDocument2 pagesIGNOU - Examination Form AcknowledgementPrashant BNo ratings yet

- NAB Statement X0256 10-Sep-2021Document6 pagesNAB Statement X0256 10-Sep-2021mkilfoyle11No ratings yet

- EStatement 2021 06 25 56667Document6 pagesEStatement 2021 06 25 56667Keith HollyNo ratings yet

- Payment ConfirmationDocument1 pagePayment ConfirmationcyrilpjoodNo ratings yet

- Bill Overview: Jlb9Rcm79Vkgxfivcivc Ykpfivcu5Kywcvxmvc56Hvcaxga2K7FDocument5 pagesBill Overview: Jlb9Rcm79Vkgxfivcivc Ykpfivcu5Kywcvxmvc56Hvcaxga2K7FAzri JamariNo ratings yet

- R902603450总成替代件8个Document1 pageR902603450总成替代件8个Luis Sanchez VeraNo ratings yet