You might also like

- Whitepaper Roic Rs InvestmentsDocument12 pagesWhitepaper Roic Rs InvestmentsmdorneanuNo ratings yet

- Suggested Solutions Assignment 03: Operational Risk ManagementDocument7 pagesSuggested Solutions Assignment 03: Operational Risk ManagementDigong SmazNo ratings yet

- Conduct Effective Quantitative Risk Assessment (QRA) - StepsDocument14 pagesConduct Effective Quantitative Risk Assessment (QRA) - Stepsamal118No ratings yet

- Asset Liability ManagementDocument18 pagesAsset Liability Managementmahesh19689No ratings yet

- M12 Titman 2544318 11 FinMgt C12Document80 pagesM12 Titman 2544318 11 FinMgt C12marjsbarsNo ratings yet

- Ghana Stock Exchange CourseDocument7 pagesGhana Stock Exchange CoursePrinceNo ratings yet

- CGAP Technical Guide Due Diligence Guidelines For The Review of Microcredit Loan Portfolios Dec 2009Document58 pagesCGAP Technical Guide Due Diligence Guidelines For The Review of Microcredit Loan Portfolios Dec 2009assefamenelik1No ratings yet

- Gathering Data For Environmental Due DiligenceDocument13 pagesGathering Data For Environmental Due DiligenceSt_LairNo ratings yet

- Experiment-8: Identify, Control and Mitigate Risks To The Project (RMMM)Document7 pagesExperiment-8: Identify, Control and Mitigate Risks To The Project (RMMM)Man UtdNo ratings yet

- Guide To Risk Appetite v2Document14 pagesGuide To Risk Appetite v2Ndangano RavhuraNo ratings yet

- 3048 - Week 5 Tute 4 Risk AssessmentDocument21 pages3048 - Week 5 Tute 4 Risk AssessmentXuân NhiNo ratings yet

- Solution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atDocument35 pagesSolution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atmichelle100% (1)

- Chapter 6Document11 pagesChapter 6jetowi8867No ratings yet

- Due Diligence TechGuide ENGDocument58 pagesDue Diligence TechGuide ENGWulan Daryoco BetrisNo ratings yet

- Reducing The Cost of AML Compliance PDFDocument24 pagesReducing The Cost of AML Compliance PDFahmedzafarNo ratings yet

- CPS Effective Project ControlDocument24 pagesCPS Effective Project ControlSom HuntNo ratings yet

- SM Ch05Document27 pagesSM Ch05Tu T Tran100% (1)

- Standard On Asset Liability Management PDFDocument13 pagesStandard On Asset Liability Management PDFHoàng Trần HữuNo ratings yet

- Credit Risk ManagementDocument3 pagesCredit Risk Managementamrut_bNo ratings yet

- Deepika CRM FDocument14 pagesDeepika CRM FkhayyumNo ratings yet

- Internal Controls and Subcontract RiskDocument5 pagesInternal Controls and Subcontract RiskMike KarlinsNo ratings yet

- The Importance of Risk Assessment and Forensic Testing For Investment AdvisersDocument12 pagesThe Importance of Risk Assessment and Forensic Testing For Investment AdvisersSEC Compliance Consultants0% (1)

- Mortgage Originations BrochureDocument16 pagesMortgage Originations Brochuremoshe3636No ratings yet

- Creating An Effective Aml Audit / Review ProgramDocument20 pagesCreating An Effective Aml Audit / Review ProgramEmin SaftarovNo ratings yet

- Manage Risk in BankingDocument26 pagesManage Risk in Bankinghossain alviNo ratings yet

- Operational RiskDocument25 pagesOperational RiskAngela ChuaNo ratings yet

- Auditing Overview and Financial Statement AuditsDocument8 pagesAuditing Overview and Financial Statement AuditsjhienellNo ratings yet

- Risk Analysis & Mgt Plan SummaryDocument3 pagesRisk Analysis & Mgt Plan SummaryPatricia BorbeNo ratings yet

- Risk Management of Financial Derivatives: Comptroller's HandbookDocument190 pagesRisk Management of Financial Derivatives: Comptroller's HandbookMoses R. M ChipuluNo ratings yet

- Ontario Municipal Employees Retirement Board: Peter S. Jarvis, CFADocument94 pagesOntario Municipal Employees Retirement Board: Peter S. Jarvis, CFAAndrés CamposNo ratings yet

- Ava Trade EU Limited Pillar 3 Disclosure 2020Document7 pagesAva Trade EU Limited Pillar 3 Disclosure 2020OlopoloNo ratings yet

- 1.7 Risk Data Aggregation and Reporting Principles-1607080143883Document21 pages1.7 Risk Data Aggregation and Reporting Principles-1607080143883ashutosh malhotraNo ratings yet

- Audit Planning and Materiality: Concept Checks P. 209Document37 pagesAudit Planning and Materiality: Concept Checks P. 209hsingting yuNo ratings yet

- Preliminary Auditing Planning: Understanding The Auditee's BusinessDocument27 pagesPreliminary Auditing Planning: Understanding The Auditee's BusinessGilang RamadhanNo ratings yet

- Actuarial AnalysisDocument12 pagesActuarial AnalysisNikita MalhotraNo ratings yet

- Guide To Risk Appetite 3Document17 pagesGuide To Risk Appetite 3Trieu NamNo ratings yet

- Solutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsDocument26 pagesSolutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsStefany Mie MosendeNo ratings yet

- Research Papers On Financial Risk ManagementDocument5 pagesResearch Papers On Financial Risk Managementgz9g97ha100% (1)

- IAA Risk Book Chapter 4 - Operational Risk Peter Boller Caroline Grégoire Toshihiro Kawano Executive SummaryDocument17 pagesIAA Risk Book Chapter 4 - Operational Risk Peter Boller Caroline Grégoire Toshihiro Kawano Executive SummaryAlexanderHFFNo ratings yet

- Operational Risk NewDocument22 pagesOperational Risk NewMahdi MaahirNo ratings yet

- UK FSA Guidance Consultation - Review of Implementation of Systems and Controls Requirements in Liquidity RegimeDocument7 pagesUK FSA Guidance Consultation - Review of Implementation of Systems and Controls Requirements in Liquidity RegimeMarketsWikiNo ratings yet

- CCRA Training Session 11Document21 pagesCCRA Training Session 11VISHAL PATILNo ratings yet

- Research Risk App Link ReportDocument57 pagesResearch Risk App Link ReportValerio ScaccoNo ratings yet

- Risk BanksDocument8 pagesRisk BanksShahed DabbasNo ratings yet

- Appendix 2 Writeup From ASIC and ACRADocument4 pagesAppendix 2 Writeup From ASIC and ACRADarren LowNo ratings yet

- Chapter 10 -Operational Risk ManagementDocument28 pagesChapter 10 -Operational Risk ManagementVishwajit GoudNo ratings yet

- Actuarial and Technical Aspects of TakafulDocument22 pagesActuarial and Technical Aspects of TakafulCck CckweiNo ratings yet

- OFS or ReportsDocument12 pagesOFS or ReportsSaratNo ratings yet

- Financial Risk Management 2007-2008 Subprime CrysisDocument11 pagesFinancial Risk Management 2007-2008 Subprime CrysisDiinShahrunNo ratings yet

- This Report Is On Assets and Liability Management of Different BanksDocument22 pagesThis Report Is On Assets and Liability Management of Different BanksPratik_Gupta_3369No ratings yet

- 6.12 Explain Each of The Seven Generally Accepted Objectives of Internal Control ActivitiesDocument4 pages6.12 Explain Each of The Seven Generally Accepted Objectives of Internal Control ActivitiesRashi ParwaniNo ratings yet

- Sen MPDocument13 pagesSen MPPushkar rane 1oth,B,ROLL NO.47No ratings yet

- AMLReportDocument33 pagesAMLReportprabu2125No ratings yet

- Cap Market MIDTERM REVIEWERDocument13 pagesCap Market MIDTERM REVIEWERMargaux Julienne CastilloNo ratings yet

- Decoding Compliance Buzzwords: The Practical Application of Risk Assessment & Forensic TestingDocument12 pagesDecoding Compliance Buzzwords: The Practical Application of Risk Assessment & Forensic TestingSEC Compliance ConsultantsNo ratings yet

- Telecommunications 2012-01-01Document28 pagesTelecommunications 2012-01-01STEVENo ratings yet

- Operational Risk Factors and Management TechniquesDocument9 pagesOperational Risk Factors and Management TechniquesTwinkal chakradhariNo ratings yet

- Research Paper of Risk ManagementDocument4 pagesResearch Paper of Risk Managementtgkeqsbnd100% (1)

- Supply Chain Risk ManagementDocument8 pagesSupply Chain Risk ManagementWandere LusteNo ratings yet

- XIV Paper 38Document11 pagesXIV Paper 38Zenon KociubaNo ratings yet

- Liquidity Risk Management Practices in Banking and Corporate WorldDocument5 pagesLiquidity Risk Management Practices in Banking and Corporate WorldmohasNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19From EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19No ratings yet

- Module 5: What You Will LearnDocument54 pagesModule 5: What You Will Learn刘宝英No ratings yet

- National Shelter ProgramDocument43 pagesNational Shelter ProgramLara CayagoNo ratings yet

- VanShop rental (1 year)Total:39,300Document51 pagesVanShop rental (1 year)Total:39,300Abdullah Muhammad0% (1)

- Evaluating A Firm's Financial PerformanceDocument47 pagesEvaluating A Firm's Financial PerformanceAhmed El KhateebNo ratings yet

- Foreign Currency Translation RulesDocument1 pageForeign Currency Translation Rulesronnelson pascual100% (1)

- Financial statements and analysis guideDocument5 pagesFinancial statements and analysis guideStars2323No ratings yet

- ETF Screener - JustETF A2Document4 pagesETF Screener - JustETF A2fish0123No ratings yet

- Harpoon Pricing Strategies PDFDocument37 pagesHarpoon Pricing Strategies PDFAmith SoyzaNo ratings yet

- Dusty R BouthilletteDocument16 pagesDusty R Bouthillettedanw5646No ratings yet

- Accounting Officers Memo 2011 Revision Final January 2012 PDFDocument37 pagesAccounting Officers Memo 2011 Revision Final January 2012 PDFRosetta RennerNo ratings yet

- Nationalisation of Banks in IndiaDocument5 pagesNationalisation of Banks in IndiaPravish Lionel DcostaNo ratings yet

- Lower-of-Cost-or-Market Valuation IssuesDocument31 pagesLower-of-Cost-or-Market Valuation Issuesalice123h21No ratings yet

- Chapter 11 HWDocument2 pagesChapter 11 HWVinícius AlvesNo ratings yet

- Submitted From:-Shampa Dhali (06) Priyanka Dhoot (07) Neeraj Gupta (14) Hardik Joshi (18) Jitendra MishraDocument24 pagesSubmitted From:-Shampa Dhali (06) Priyanka Dhoot (07) Neeraj Gupta (14) Hardik Joshi (18) Jitendra MishraShompa Dhali NandiNo ratings yet

- Hedge AccountingDocument8 pagesHedge AccountingDilip YadavNo ratings yet

- Volume Profile TradingDocument8 pagesVolume Profile TradingSimon Tin Hann Pyng100% (2)

- Quiz Number One Without AnswerDocument8 pagesQuiz Number One Without AnswerKpop updates 24/7No ratings yet

- APC Training Guide - QSDocument41 pagesAPC Training Guide - QSAinobushoborozi AntonyNo ratings yet

- Underwriting SOPDocument5 pagesUnderwriting SOPChris JacksonNo ratings yet

- 2006-07 - GrasimDocument117 pages2006-07 - GrasimrNo ratings yet

- Pisa Pizza healthier pizza sales projectionsDocument6 pagesPisa Pizza healthier pizza sales projectionskarol nicole valero melo100% (1)

- FAC MCQs UnitwiseDocument7 pagesFAC MCQs UnitwiseSamNo ratings yet

- FIN 735 IntroductionDocument23 pagesFIN 735 IntroductionKetki PatilNo ratings yet

- Master Budget Case: Toyworks Ltd. (A)Document4 pagesMaster Budget Case: Toyworks Ltd. (A)RIKUDO SENNIN100% (1)

- Valuation of Tata SteelDocument3 pagesValuation of Tata SteelNishtha Mehra100% (1)

- HSBC Premier Savings Terms & Charges Disclosure: EligibilityDocument3 pagesHSBC Premier Savings Terms & Charges Disclosure: EligibilityAndi PrabowoNo ratings yet

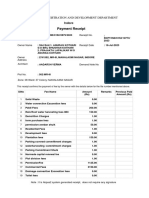

- Payment Receipt: Urban Administration and Development DepartmentDocument2 pagesPayment Receipt: Urban Administration and Development Departmentaadarsh vermaNo ratings yet