You might also like

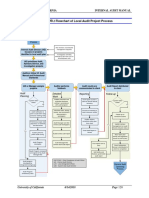

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- CIA - Wiley & Vallabhaneni Part 2Document80 pagesCIA - Wiley & Vallabhaneni Part 2Kay Cee TangalinNo ratings yet

- QMS Internal Auditor TrainingDocument43 pagesQMS Internal Auditor TrainingJan Francis Wilson MapacpacNo ratings yet

- At.3206-Planning An Audit of Financial StatementsDocument6 pagesAt.3206-Planning An Audit of Financial StatementsDenny June CraususNo ratings yet

- Internal Quality Audit ProcessDocument4 pagesInternal Quality Audit ProcessJennylyn Favila MagdadaroNo ratings yet

- Session 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsDocument55 pagesSession 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsRheneir Mora100% (1)

- Introduction To Internal AuditingDocument59 pagesIntroduction To Internal AuditingPaviththira sivaNo ratings yet

- II - Audit Strategy, PlanningDocument8 pagesII - Audit Strategy, PlanningAlphy maria cherianNo ratings yet

- Audit PlanningDocument21 pagesAudit Planningablay logeneNo ratings yet

- Destination Agile AuditingDocument19 pagesDestination Agile AuditingJason TangNo ratings yet

- Unit 2 Audit Planning and ProgrammeDocument37 pagesUnit 2 Audit Planning and ProgrammeDeepanshu PorwalNo ratings yet

- Auditing PlanningDocument15 pagesAuditing PlanningDarren R. RoaringNo ratings yet

- Lesson 2 - Audit PlanningDocument24 pagesLesson 2 - Audit PlanningrylNo ratings yet

- Quality AuditDocument10 pagesQuality Audit1984subbulakshmiNo ratings yet

- Audit Planning & Consideration of Internal Control PDFDocument33 pagesAudit Planning & Consideration of Internal Control PDFVRNo ratings yet

- Audit PlanningDocument17 pagesAudit PlanningMathew P. VargheseNo ratings yet

- At 05 - Auditor PlanningDocument8 pagesAt 05 - Auditor PlanningRei-Anne ReaNo ratings yet

- LectureNote AudiImpl UjiKompre 2022Document87 pagesLectureNote AudiImpl UjiKompre 2022ANDI MUHAMMAD RAYHANNo ratings yet

- Auditing-Techniques-Audit Performance 2022Document50 pagesAuditing-Techniques-Audit Performance 2022kyawNo ratings yet

- Project On Audit Plan and Programme & Special AuditDocument11 pagesProject On Audit Plan and Programme & Special AuditPriyank SolankiNo ratings yet

- The Risk-Based Audit Process - Phase 1-BDocument15 pagesThe Risk-Based Audit Process - Phase 1-BJoseph LomboyNo ratings yet

- Day 2 - IAI-Effective - Technique - For - Internal - AuditDocument65 pagesDay 2 - IAI-Effective - Technique - For - Internal - AuditArdiFarazNo ratings yet

- Chapter 3 - Audit Planning Startegy and Execution - QRDocument9 pagesChapter 3 - Audit Planning Startegy and Execution - QRAnkita SharmaNo ratings yet

- Audit PlanningDocument4 pagesAudit PlanningLoo Bee YeokNo ratings yet

- Planning and Risk AssessmentDocument13 pagesPlanning and Risk AssessmentLakmal KaushalyaNo ratings yet

- Fam Chapter 6 21092005Document15 pagesFam Chapter 6 21092005Humayoun Ahmad FarooqiNo ratings yet

- How To Perform An ISO Internal Audit Webinar Presentation DeckDocument23 pagesHow To Perform An ISO Internal Audit Webinar Presentation DeckJorge D. Zunini C.No ratings yet

- AT.3405 - Audit Planning and MaterialityDocument10 pagesAT.3405 - Audit Planning and MaterialityMonica GarciaNo ratings yet

- Chapter 2 Audit Strategy, Planning and Programme - ScannerDocument44 pagesChapter 2 Audit Strategy, Planning and Programme - ScannerRanjisi chimbanguNo ratings yet

- Overview of Working Papers in RAMDocument21 pagesOverview of Working Papers in RAMIsha PopNo ratings yet

- Week 13 Report: Presented By: Aileen M. Manangan Joebert S. RoderosDocument24 pagesWeek 13 Report: Presented By: Aileen M. Manangan Joebert S. RoderosKim SeokjinNo ratings yet

- Internal Audits: 1. PurposeDocument4 pagesInternal Audits: 1. PurposesumanNo ratings yet

- Audit Notes Ca BosDocument30 pagesAudit Notes Ca BosBijay AgrawalNo ratings yet

- Audit Plan Includes A Description ofDocument9 pagesAudit Plan Includes A Description of03LJNo ratings yet

- Chapter 5 - Audit ProcessDocument60 pagesChapter 5 - Audit ProcessThị Hải Yến TrầnNo ratings yet

- 3 Audit PlanningDocument15 pages3 Audit Planningarc chanukaNo ratings yet

- ACAUDDocument40 pagesACAUDchxrlttxNo ratings yet

- Audit Strategy, Audit Planning and Audit Programme: Learning OutcomesDocument31 pagesAudit Strategy, Audit Planning and Audit Programme: Learning OutcomesMayank JainNo ratings yet

- Aa CH15Document41 pagesAa CH15Thuỳ DươngNo ratings yet

- SA-MAGE-PQP - Internal AuditsDocument21 pagesSA-MAGE-PQP - Internal Auditssajidazmi.amuNo ratings yet

- Audit ProcessDocument30 pagesAudit ProcesspradeepNo ratings yet

- Audit Process - Risk Assesment Kel 4Document33 pagesAudit Process - Risk Assesment Kel 4MylaNo ratings yet

- Udemy Course CIA Part 2 Focus MaterialsDocument77 pagesUdemy Course CIA Part 2 Focus MaterialsLayar KayarNo ratings yet

- Audit Strategy, Audit Planning and Audit ProgrammeDocument9 pagesAudit Strategy, Audit Planning and Audit ProgrammePrachi GuptaNo ratings yet

- Aud Agile Eng m01 Pnotes Background Terms and DefinitionsDocument5 pagesAud Agile Eng m01 Pnotes Background Terms and DefinitionsMohamed ElsawyNo ratings yet

- Chapter 4 - Overview of Audit Process and Preliminary ActivitiesDocument42 pagesChapter 4 - Overview of Audit Process and Preliminary ActivitiesCarlos Miguel MendozaNo ratings yet

- Materi Test of ControlDocument66 pagesMateri Test of ControlIntan100% (1)

- Bos 34430 SMCP 2Document12 pagesBos 34430 SMCP 2remtluangachhangte7No ratings yet

- Session - 4 - Planning - An - Audit - of - Financial - StatementDocument12 pagesSession - 4 - Planning - An - Audit - of - Financial - StatementIrandi UthpalaaNo ratings yet

- CH 2 - Audit StrategyDocument10 pagesCH 2 - Audit StrategyvedthkNo ratings yet

- How To Perform An ISO Internal Audit Presentation DeckDocument17 pagesHow To Perform An ISO Internal Audit Presentation DeckMARK CASANOVANo ratings yet

- EICC VAP AuditOperationsManualv5 01 Ch07 PDFDocument24 pagesEICC VAP AuditOperationsManualv5 01 Ch07 PDFYusuf Bayu AjiNo ratings yet

- Software Process Reviews/Audits Process OverviewDocument22 pagesSoftware Process Reviews/Audits Process OverviewVipendra SinghNo ratings yet

- Overview of Auditing Process: Planning and Preparation Opening Meeting Follow-Up and ClosureDocument129 pagesOverview of Auditing Process: Planning and Preparation Opening Meeting Follow-Up and ClosureRAM KUMARNo ratings yet

- Aa CH10Document26 pagesAa CH10Thuỳ DươngNo ratings yet

- Effective IQA Report Writing Workshop-9001-2015Document50 pagesEffective IQA Report Writing Workshop-9001-2015ianalleahNo ratings yet

- QCPR08 - Internal Audit Rev 7Document3 pagesQCPR08 - Internal Audit Rev 7FAIRUZ IZYAN BINTI IBRAHIMNo ratings yet

- Section 1 - Planification Des AuditsDocument22 pagesSection 1 - Planification Des AuditsPhilippe RoeschNo ratings yet

- Lecture Notes: Auditing Theory AT.1808-Audit Planning-An Overview MAY 2015Document8 pagesLecture Notes: Auditing Theory AT.1808-Audit Planning-An Overview MAY 2015Misa AmaneNo ratings yet