Professional Documents

Culture Documents

Ebook Cost Acc Carter 14ed PDF

Ebook Cost Acc Carter 14ed PDF

Uploaded by

Adam Indra Laksono0 ratings0% found this document useful (0 votes)

9 views919 pagesOriginal Title

444148069 eBook Cost Acc Carter 14ed PDF

Copyright

© © All Rights Reserved

Available Formats

PDF or read online from Scribd

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

© All Rights Reserved

Available Formats

Download as PDF or read online from Scribd

0 ratings0% found this document useful (0 votes)

9 views919 pagesEbook Cost Acc Carter 14ed PDF

Ebook Cost Acc Carter 14ed PDF

Uploaded by

Adam Indra LaksonoCopyright:

© All Rights Reserved

Available Formats

Download as PDF or read online from Scribd

You are on page 1of 919

Cost Accounting

14th Edition

Carter

THONISON

ee

Custom Editor:

Greg Albert

Marketing Coordinators:

Lindsay Annett and Sara

Mercurio

Production /Manufacturing

Supervisor:

Donna M. Brown

© 2006 Carter

Printed in the

United States of America

123456789 08 07

06

For more information, please

contact Thomson Custom

Solutions, 5191 Natorp

Boulevard, Mason, OH 45040.

Or you can visit our Internet

site at

www.thomsoncustom.com

ALL RIGHTS RESERVED. No part

of this work covered by the

THOMSON

eS es

Cost Accounting

Carter

Project Coordinator:

Dave Lyons

Pre-Media Services

Supervisor:

Dan Plofchan

Rights and Permissions

Specialist:

Kalina Hintz

copyright hereon may be

reproduced or used in any form

or by any means — graphic,

electronic, or mechanical,

including photocopying,

recording, taping, Web

distribution or information

storage and retrieval systems

—without the written

permission of the author,

Carter.

The Adaptable Courseware

Program consists of products

and additions to existing

Thomson Custom Solutions

products that are produced

from camera-ready copy.

Senior Prepress Special

Kim Fry

Cover Design:

Phoenix Creative

Printer:

Quebecor, Taunton

Peer review, class testing,

and accuracy are primarily tk

responsibility of the author‘

For permission to use materia

from this text or product,

contact

us by

Tel (800) 730-2214

Fax (800) 730 2215,

www.thomsonrights.com

Cost Accounting/ Carter

14th Edition

p. 960

ISBN 0-759-33809-4

Preface

Globalization, increased competition, and new technologies have forced many companies

to reevaluate their business. This reevaluation led to changes in management philosophy

and in business systems, which in turn required accountants to reevaluate the usefulness of

information the accounting system provides to management. Accounting systems created

primarily to provide information for external reporting, or created at a time when manu-

facturing technologies and systems were essentially labor driven, are no longer adequate.

The information provided by obsolete accounting systems is sometimes useless and some-

times dangerously misleading.

To provide information needed by management, accountants began to redesign

accounting systems. Different kinds of data are needed for different kinds of decisions, and

different kinds of business systems require different kinds of accounting systems to pro-

vide that data. As business systems change, accounting systems are reevaluated and, in

some cases, changed. Recognizing these relationships leads to developing and implement-

ing new measurement systems, such as quality costing, activity based costing, and back-

flush costing, as well as to increased use of nonfinancial performance measures.

‘The fourteenth edition of Cost Accounting emphasizes the use of accounting informa

tion in planning and controlling a business and in supporting management decisions,

including strategic decisions that position the firm to compete better. To be effective, the

accounting system must be tailored to the particular business systems employed. Since the

goods and services produced by different companies vary substantially, the business sys

tems required for production and marketing vary as well. Because of these differences,

there is no one accounting system or alternative superior to all others. The best accounting

system depends on the business system and the information needs of management

To prepare the student, this textbook not only demonstrates the mechanics of alterna-

tive accounting systems and techniques but also explains the logic behind different alter-

natives, The objective is to help the student learn to look at the business first and then to

design an accounting system that can collect and generate the kind of information needed

This textbook is designed to provide the necessary background for those who prepare

accounting information and for those who use the information. This book presents not only

the systems of collecting, organizing, processing, and reporting economic data, but also the

uses of accounting information in making decisions. This dual emphasis is needed because

(J) the accountant must understand how information will be used in order to design an

accounting system to collect and report the information needed, and (2) the user of

accounting information must understand how the accounting system works in order to use

the information appropriately and know its limitations.

Highlights of Changes in the Fourteenth Edition

The textbook has undergone revisions to make it shorter and better written, with the goal

of assisting both student and instructor. As with the preceding edition, considerable effort

has been made to enhance clarity, The primary changes from the thirteenth edition are:

ation.

1. Several chapters have been edited to improve clarity and brevity of pre

2. Chapter 2 has been updated by the addition of an appendix on the Balanced

Scorecard

iv Preface

3. Approximately one-fourth of the problems and exercises have been revised. In

some of the chapters that are likely to be of higher importance to many instructors,

over one-third of the problems and exercises have been revised

Organization of the Book

The organization of the materials presented is designed to provide maximum flexibility in

meeting different course objectives. Part One presents material that forms a foundation for

understanding the basic concepts and objectives of costmanagerial accounting systems. It

thoroughly discusses the cost concept, cost objects, classification of cost, and cost behav-

ior. Part Two then discusses and illustrates the flow of cost in manufacturing and services

businesses. It begins with a general explanation of the flow of costs through the accounts

and then expands into an in-depth discussion of the two basic costing systems: job order

costing and process costing. Part Two includes the cost of quality, accounting for produc-

tion losses, and joint- and by-product costing, Part Three focuses on an in-depth under-

standing of the elements of cost—materials, labor, and overhead—from both the planning

and control perspectives.

Part Four elaborates on the heart of planning and control: static and flexible budgeting,

responsibility accounting and reporting, and standard costing. Part Five deals with the

analysis of costs and profits, including direct costing, the theory of constraints, cost-

volume-profit analysis, differential cost analysis, capital expenditure planning and analysis,

decision making under uncertainty, profit performance measurements, and transfer pricing.

Organization for Instruction

The presentation of the fundamental theoretical and practical aspects of cost accounting

provides wide flexibility for classroom usage. In addition to its applicability to the tradi-

tional two-semester course sequence, this textbook may be used in a variety of one-

semester courses. For these alternative courses, a suggested outline, by chapter numbers,

follows:

Course Description ‘Textbook Chapters

Cost Accounting (iwo semesters) Chapters 1-14 (first semester)

Chapters 15-25 (second semester)

Cost Accounting (one semester) Chapters 1-14 and 17

Cost Control (one semester) Chapters 1-4, 9-14, and 17-19

Budgetary Control (one semester) Chapters 1-4, 15-19, and 22-23

Cost Analysis (one semester) Chapters 14-25,

End of Chapter Materials

End-of-chapter materials, many of which are revised, include discussion questions, exer-

cises, problems, and cases. For each topic, these materials afford coverage of relevant

concepts and techniques at progressive levels in the learning process, thereby providing

@ significant student-learning benefit. Selected exercises and problems with which the

Cost Accounting 14" Edition x

template diskette may be used are designated by symbols in the margin, The end-of-chap-

ter materials include numerous items from the examinations administered by the America

Institute of Certified Public Accountants (AICPA adapted), the Institute of Management

Accounting (ICMA adapted), the Certified General Accountants’ Association of Canada

, (CGA-Canada Adapted), and the Society of Management Accountants of Canada ((CMA-

Canada’).

Learning and Teaching Aids that Accompany the Book

For the Instructor

Solutions Manual. This manual contains detailed solutions to the end-of chapter materi-

als, including the discussion questions, exercises, problems, and cases. In addition, a list-

ing of items coded for use with the template diskette is provided

Test Bank, prepared by Edward J. VanDerbeck of Xavier University, Cincinnati. A test

bank of multiple choice questions and examination problems accompanied by solutions is

available to the instructor, The Test Bank is designed to save time in preparing and grad-

ing periodic tests and final examinations.

Spreadsheet Applications, These template diskettes are used with Microsoft Excel! for

solving selected end-of-chapter exercises and problems identified in the textbook with the

symbol in the margin. The diskettes, which also provide a Microsoft Excel tutorial, are

provided free of charge to instructors at educational institutions who adopt this text.

For the Student

Study Guide, prepared by Edward J. VanDerbeck. This study guide contains a brief sum-

mary of each chapter, as well as questions and exercises with answers, thus providing stu-

dents with immediate feedback on their comprehension of material

Practice Cases, prepared by William K. Carter. job order case and a process cost case

are available. Each case acquaints students with basic accounting and analytical character-

istics with a minimum of time-consuming detail. Solutions are provided for the instructor.

Acknowledgements

Special thanks are due to Greg Albert, whose tireless efforts were indispensable in produc-

this edition.

July 2005 William K. Carter

1 "Microsoft" and “Excel” are registered trademarks of Microsolt Corporation. Any reference to Microsoft or Excel

felers to this footnote.

vi

Preface

About the Author

William K. Carter teaches management accounting at the McIntire School of Commerce,

University of Virginia. He eared BS and MS degrees in accounting from the University

of Southern Mississippi and a PhD from Oklahoma State University, and he is a CPA. He

has written articles on accounting, accounting education, marketing, and finance, which

have appeared in a variety of journals including The Accounting Review and the Journal of

Accountancy. He has published cases on cost accounting, business policy, the balanced

scorecard, and activity based costing

Dr. Carter has served on committees of the American Assembly of Collegiate Schools

of Business and the American Accounting Association, and on the editorial boards of The

Journal of Accounting Education and the Education Section of The Accounting Review. He

has testified as an expert witness in litigation involving accounting matters and has con-

ducted consulting engagements and executive development programs for business and

industry,

Dr. Carter is a member of the Institute of Management Accountants, the American

Institute of CPAs, and the American Accounting Association Management Accounting

Section.

Dedication

to my wife, Imelda Smith Carter, for her patience and many sacrifices.

Contents in Brief

Part 1 Costs: Concepts and Obje

1 Management, the Controller, and Cost Accounting tecsseeeee E

2 — Cost Concepts and the Cost Accounting Information System . wreieen Pel

3 Cost Behavior Analysis 6 bees o sess BI

Part2 Cost Accumulation

Cost Systems and Cost Accumulation. ....-. +. impeyecemcsen 48

Job Order Costing - es

Process Costing .....+++6+++ cee ceceeeee 6

‘The Cost of Quality and Accounting for Production Losses... 0... woo

Costing By-Products and Joint Products... ......2-0ee0ee0eeeeee eres 8

wulaHe

Part 3. Planning and Control of Costs

9 Materials: Controlling, Costing, and Planning . 9-1

10 Just-in-Time and Backflushing : 10-1

11 Labor: Controlling and Accounting for Costs il

12 Factory Overhead: Planned, Actual, and Applied 12-1

13. Factory Overhead: Departmentalization 31

14 Activity Accounting: Activity-Based Costing and

Activity-Based Management .....0. 006020020202 eeee 0 wee . 14d

Part 4 Budgeting and Standard Costs

15 Budgeting: Profits, Sales, Costs, and Expenses ....... 0.220005 eS

16 Budgeting: Capital Expenditures, Research and Development

Expenditures, and Cash; PERT/COSt.....064002200e000eeeeeeees cece GL

17 Responsibility Accounting and Reporting. . . . ete eer 17-1

18 Standard Costing: Setting Standards and Analyzing Variances sos eeseeecceee 18d

19 Standard Costing: Incorporating Standards into

the Accounting Records........e0000ee00eeeereeeeee eae eer 19-1

Part 5 Analysis of Costs and Profits

20 Direct Costing, CVP Analysis, and the Theory of Constraints. 20-1

21 Differential Cost Analysis : 21-1

22 Planning for Capital Expenditures 22-1

23, Economic Evaluation of Capital 2Bel

24 ‘ 24-1

35 Profit Performance Measurements and Intracompany

‘Transfer Pricing. . ceeeee . veeeeeee SENOS Te se wee 25-1

Glossary Gl

Ll

Index.

vil

Contents

Part 1 Costs: Concepts and Objectives

Chapter 1 Management, the Controller, and Cost Accounting. .

Learning Objectives ...

Management

Planning

Organizing

Control

Authority, Responsibility, and Accountabil

The Organization Chart ene

‘The Controller's Participation in Planning and Control...

‘The Cost Department . .

The Role of Cost Accounting

Budgeting ;

Controlling Costs

Pricing

Determining Profits ......

Choosing Among Alternatives ..

Cost Accounting and Manufacturing Technology

Certification and Ethics.

Influence of Private and Governmental Organizations an

Taxation .

Cost Accounting Standards Board...

Chapter 2. Cost Concepts and the Cost Accounting Information System...

Learning Objectives . .

The Cost Concept ......

Cost Objects...

Traceability of Costs to Cost Objects.

2ost Traceability in Service Industries.

The Cost Accounting Information System

Chart of Accounts

Electronic Data Processing. .......

Sensitivity to Changing Methods

Nonfinancial Performance Measures

Classifications of Costs. .....

Costs in Relation to the Product

Costs in Relation to the Volume of Production

Costs in Relation to Manufacturing Departments or Other Segments.

Costs in Relation to an A¢ ounting Period wee

Costs in Relation to a Decision, Action, or Evaluation .

Appendix: The Balanced Scorecard ........

The Scorecard Perspectives

A Series of Predictions :

‘orecards Aid in Communication. .

Anal

Cost Accounting 14* Edition ix

Chapter 3 Cost Behavior Analysis

Learning Objectives

Classifying Cost

Fixed Cost

Variable Cost.

Semivariable Cost

Separating Fixed and Var

High and Low Points Method

ple Costs,

Scattergraph Method . eee cee 37

Method of Least Squares 39

Method of Least Squares for Multiple Independent Variables. 3-16

Part 2 Cost Accumulation

Chapter 4 Cost Systems and Cost Accumulation ......0..-+

Learning Objectives

Flow of Production Costs

Reporting the Results of Operations

Income Statement

Balance Sheet :

tement of Cash Flows . . vanes

Cost Systems

Cost Accumulation

Job Order Costing

Process Costin

Aspects Common to Both Job Order and Proces

Blended Methods

Backflush Costing a Fayeh Fr

Costing

Chapter 5 Job Order Costing .... Seemn 4g greens even

Learning Objectives pec eeaeresnanc oe

Overview of Job Order Costing

Accounting for Materials feel rseoreeeneeees

Materials Purchased gees v canons

Materials Used ........e000e00eee

Accounting for Labor

Factory Labor Cost Incurred . .

Factory Labor Costs Distributed

Accounting for Factory Overhead.

Actual Factory Overhead Incurred...

Estimated Factory Overhead Applied .

Accounting for Jobs Completed and Products Sold...

Job Order Costing in Service Businesses .

‘Table of Contents

Chapter 6 Process Costing............0.00000085 hee 6-1

Learning Objectives Te 61

Process Cost Accumulation............ cece Gl

Costing by Departments . 62

Physical Production Flow nee “ 6-3

Accounting'for Materials, Labor, and Factory Overhead Costs - 64

‘The Cost of Production Report [ 6-7

Increase in Quantity of Production When Materials Are Added . . 6-1

Appendix: Process Costing with a Fifo Cost Flow Assumption ........... 6-15

Increase in Quantity of Production When Materials Are Added . . 6-19

Chapter 7 ‘The Cost of Quality and Accounting for Production Losses rl

Learning Objectives ; Tl

The Cost of Quality. . 72

‘Types of Quality Costs 7-2

‘Total Quality Management 72

Continuous Quality Improvement 14

Measuring and Reporting the Cost of Quality 76

Accounting for Production Losses in a Job Order Cost System 7-7

Accounting for Scrap shdoeatg elie cusine «seompg mee © 5a 1

Accounting for Spoiled Goods. . 18

Accounting for Rework iets Seheeeul 4 as 7-10

Accounting for Production Losses in a Process Cost System 7-12

Spoilage Auributable to Internal Failures. 7-12

Normal Production Shrinkage bettessssssees 716

Appendix: Process Costing with a Fifo Cost Flow Assumption se. 7-20

Spoilage Attribute to Internal Failures... vevvveeteteeeeeeeee 7-20

Normal Production Shrinkage .......... fp omneanoes 7:24

Chapter 8 Costing By-Products and Joint Products. 81

Learning Objectives . 8-1

By-Products and Joint Products Defined . 8&1

Nature of By-Products and Joint Products 8-2

Joint Costs...... a, 82

Difficulties in Costing By-Products and Joint Products. 8.2

Methods of Costing By-Products . . 83

Method 1: Recognition of Gross Revenue. Msinrueassnes 84

Method 2: Recognition of Net Revenue... cece 8S

Method 3: Replacement Cost Method : teicns 8S

Method 4: Market Value (Reversal Cost) Method ..........2.022222. 86

Underlying Accounting Theory ... : 87

Methods of Allocating Joint Production Cost to Joint Products 8.7

Market Value Method ......00.cccccecsesesseeeceeeeeeeeeeeee 8-7

Average Unit Cost Method... : wees 8410

Weighted-Average Method : wad ipwint femineceatsers » el0

Quantitative Unit Method. . boos o 8-11

Federal Income Tax Laws and the Costing of Joint Products and By-Products... 8-12

Joint Cost Analysis for Managerial Decisions and Profitability Analysis... 8-12

Ethical Considerations : 8-13

Cost Accounting 14" Edition xi

Part 3 Planning and Control of Costs

Chapter 9 Materials: Controlling, Costing, and Planning ...........---- 91

Learning Objectives ..... ee 9-1

Materials Procurement and Use o1

Purchase of Materials 92

Purchases of Supplies, Services, and Repairs .... . 93

Purchasing Forms . ageing «5 ace tn 93

Receiving . - - oF

Invoice Approval and Data Processing 9.5

Cost of Acquiring Materials 96

Storage and Use of Materials 9.8

Issuing and Costing Matei 2 oe 98

Materials Subsidiary Records phe eens - 99

Quantitative Models... cee fees 9-10

Planning Materials Requirements. . . . ce 9-10

Economic Order Quantity... Reet

The EOQ Formula and Production Runs. . ne $8 RSEE S 944

Determining the Time to Order eee od

Order Point Formula... 5 9-45

Computer Simulation for Materials Requirements Planning... 9-17

Materials Control 9-17

Materials Control Methods 918

Control of Obsolete and Surplus Inventor . 9-19

Appendix: Inventory Costing Methods. 9:19

First In, Fitst Out (Fif0).... 0002 -000ee eee e esse eeeeneerees 9.20

Average Cost. -

Last In, First Out (Lifo)

Comparison of Costing Methods

CASB Costing of Materials

Lower of Cost or Market .

Interim Financial Reporting of Inventory... - 9-24

Chapter 10. Just-in-Time and Backflushing wsonsunercosersuen Tel

Learning Objet . : : 10-1

Just-in-Time 10-1

JIT and Velocity 10-3

JIT and Production Losses 10-4

JIT and Purchasi seen 10-6

JIT and Factory Organization 10-7

JIT—A Balanced View om 10-8

Backflushing : 10-9

The Essence of Buckflush Costing, 2 10-10

A Basic Financial Accounting Analogy... sees . wees 10-11

Ilustration of Backflush Costing . .. . cuoumernensré [Ont

Table of Contents

Chapter 11 Labo

Controlling and Accounting for Costs. ...... Hel

Learning Objectives 1-1

Productivity and Labor Costs lel

Planning Product ies . 12

Measuring Productivity . apcaSiga

Economic Impact of Productivity... ser

Increasing Productivity by Better Management of Human Resources... 11-3,

Incentive Wage Plans iE. 5.1 ton s . bd

Purpose of an Incentive Wage Plan... . bene raerianeace 4

‘Types of Incentive Wage Plans. veceeeee eee es 1-5

Organizational Incentive (Gainsharing) Plans ce cesses UT

‘Time Standards and Learning Curve Theory ..... temnenmres TGS

Organization for Labor Cost Accounting and Control . ... 11-10

Personnel Department. . vecetteeteeeeeeeeeeee TEU

Production Planning Department... .. . i . HII

Timekeeping Department.............. 11-12

Payroll Department EE Meld

Cost Department... vee UIAIS

Department Interelationships and Labor Cost Control and Accounting -

Ethical Considerations:

Appendix: Accounting for Personnel-Related Costs .

Overtime Earnings ..............

Bonus Payments and Deferred Compensation Plans... oss

Vacation Pay

Guaranteed Annual Wage Plans

Pension Plans 5

Additional Legislation Affecting Labor-Related Costs

Labor-Related Deductions .

Recording Labor Costs. .

Chapter 12 Factory Overhead: Planned, Actual, and Applied.............. 12-1

Learning Objectives . . “RNG Page 5 cist»

‘The Nature of Factory Overhead...

Use of a Predetermined Overhead Rate...

Factors Considered in Selecting Overhead Rates

Base to Be Used.........

Selection of Activity Level

Including or Excluding Fixed Overhead

Calculation of an Overhead Rate

Actual Factory Overhead ... .

Applied Overhead and the Over- of Underapplied Amount. .

Applying Factory Overhead . eos

Over: or Underapplied Factory Overhead .

Disposition of Over- or Underapplied Amount

Changing Overhead Rates...

Cost Accounting 14" Edi

jon

Chapter 13 Factory Overhead: Departmentalization.

Learning Objectives .

Departmentalization <

Producing and Service Departments.

Selection of Producing Department :

Selection of Service Departments .......

Direct Departmental Costs

Supervision, Indirect Labor, and Overtime .

Labor Fringe Benefits

Indirect Materials and Supplies ......... 0060005

Repairs and Maintenance

Equipment Depreciation

Indirect Departmental Costs .

Establishing Departmental Overhead Rates

Estimating Direct Departmental Costs

Factory Survey .

Estimating and Allocating Indirect Costs

Distributing Service Department Costs

Calculating Departmental Overhead Rates,

Using Departmental Overhead Rates

Actual Factory Overhead—Departmentalized

Steps at End of Fiscal Period

Muhtiple Overhead Rates. .

Overhead Departmentalization in Nonmanufacturing Businesses

and Not-for Profit Organizations . . .

Chapter 14 Activity Accounting: Activity-Based Costing

and Activity-Based Management .

Learning Objectives

Activity-Based Costing

Levels of Costs and Drivers oo

Comparison of ABC and Traditional Costing «+...

ABC and Product Cost Distortion

Strategic Advantage of ABC... .

Example of ABC Implementation. :

Strengths and Weaknesses of ABC.........

Activity-Based Management. . . . .

Behavioral Changes

Cost Control

Part 4 Budgeting and Standard Costs

Chapter 15 Budgeting: Profits, Sales, Costs, and Expenses

Leaming Objectives .

Profit Planning. .....

Setting Profit Objective

Long-Range Profit Planning

xiv ‘Table of Contents

Short-Range Budgets .........0605 sab rise - 15:3

Advantages of Profit Planning fee cece 154

Limitations of Profit Planning .........6...0. . wim 154

Principles of Budgeting. : og v0.8 Sree, 155.

The Budget Commitee. ... ¥ sey on - 155

Budget Development and Implementation 15-6

Budgeting and Human Behavior 15-7

The Complete Periodic Budget, . 15-8

Sales Budget... 15-8

Production Budget 15-12

Manufacturing Budgets 15-13

Budgeting Commercial Expenses. 15-19

Budgeted Incom 15-22

cece 15-23

Chapter 16 Budget pital Expenditures, Research and

Development Expenditures, and Cash; PERT/Cost 16-1

Learning Objectives 16-1

Capital Expenditures Budget . .. peaeah - . 16-1

Evaluating Capital Expenditures ........0.... 16-2

Short- and Long-Range Capital Expenditures 16-2

Research and Development Budget . ee 16-2

Form of a Research and Development Budget estamos 163

Accounting for Research and Development Costs ....... 164.

Cash Budget _ Pei 16-5

Purpose and Nature of a Cash Budget 16-5

Preparation of a Periodic Cash Budget 16-6

Development of Daily Cash Budget Detail . 16-7

Electronic Cash Management 16-8

Planning and Budgeting for Nonmanufacturing Businesses

and Not-for-Profit Organ

Nonmanufacturing Businesse:

Not-for-Profit Organiza

Zero-Base Budgeting

Computerized Budgeting

Prospective Financial Informan

stem...

The PERT/Cost System

Computer Applications...

Probabilistic Budgets

seeeene a 17-1

Learning Objectives .......... se IT

Responsibility Accountin 17-1

c sin 17-2

Determining Who Controls Cost . MLE ESEE Pian icine ns 1903

Cost Accounting 14" Edition XY

Responsibility for Overhead Costs

Responsibility Reporting ...........+

Fundamental Characteristics of Responsibility Reports

Responsibility-Reporting Systems Illustrated

Reviewing the Reporting Stucture

The Flexible Budget and Variance Analysis

Preparing a Flexible Budget

Preparing a Variance Report...

Responsibility Accounting and Reporti

Dysfunctional Behavior of Managers.

Usefulness of the Data to Managers. .

An Alternative View

Chapter 18 Standard Costing: Setting Standards

and Analyzing Variances... oon vee 181

Learning Objectives ... . is an : 18-1

Usefulness of Standard Costs. : ee 18-1

Setting Standards, (isone 18-3

Determining Standard Production. 18-5

tandard Cost Variances ..... wine - 18-7

Determini

Materials Standards and Variances 18-7

Labor Standards and Variances. . 18-9

Factory Overhead Standards and Variances « 18-11

Mix and Yield Variances . .. ee vee : » 1816

Mix Variance 18-16

Yield Variance. . . 18-17

lustration of Mix and Yield Variane 18-17

Responsibility and Control of Variances 18-19

Causes of Variances - : a cess 18-20

Tolerance Limits for Variance Control... ++ 5 3 18-26

Overemphasizing Variances . .- iene 18-26

Appendix: Alternative Factory Overhead Variance Methods... 18-28,

Alternative Three-Variance Method

Four-Variance Method . . . to

Chapter 19 Standard Costing: Incorporating Standards

into the Accounting Records

Learning Objectives ....- 03

Recording Standard Cost Variances in the Accounts... +

Standard Cost Accounting for Materials.

Method 1. . oe re

Method 2.......00208++ . sen CaN

Method 3..... cunone otha : ee

Standard Cost Accounting for Labor

Standard Cost Accounting for Factory Overhead . .

‘Two- Variance Method

Three-Variance Method

Standard Cost Accounting for Completed Products...

xvi ‘Table of Contents

Disposition of Variances . 19-7

Variances Treated as Period Expenses. 19-7

Variances Allocated to Cost of Goods Sold and Ending Inventories 19-10

The Logie of Disposing of Varia 19-12

Disposition of Variances for Interi 19-14

Revision of Standard Costs....... 19-14

Broad Applicability of Standard Co: 19-15

Appendix: Alternative Factory Overhead Variance Method 19-16

Alternative Three-Variance Method... . cone 19-16

Four-Variance Method . Se 19-16

Part 5 Analysis of Costs and Profits

Chapter 20 Direct Costing, Cost-Volume-Profit Analysis, and

the Theory of Constraints... 20-1

Learning Objectives 20-1

Direct Costing . 20-2

Contribution Margin Defined . 20-2

Internal Uses of Direct Costing . .. 20-3

External Uses of Direct Costing. 20-7

Cost-Volume-Profit A 20-13

Constructing a Bi 20-16

Cost-Volume-Pro 20-18

The Theory of Constr 20-23

Measures Used in the Theory of Constraints 20-24

Using the Theory of Constraints 20-24

Examples of TOC Implementation. 20-25

Embracing TOC as an Accounting Tool. 20-26

Chapter 21 Differential Cost Analysis 21-1

Learning Objectiv nat sing 21-1

Differential Cost Studies. 24-1

Examples of Differential Cost Studies ..

Accepting Additional Orders : 21-4

ing the Price of a Special Order 21-5

or-Buy Decisions . 21-7

ms to Shut Down Facilities 21-9

Decisions to Discontinue Products. 2-1

Additional Applications of Differen 21-13

Appendix: Linear Programming 24-17

Maximization of Contribution Margin 21-17

Minimization of Cost . si ceeeeee 21-21

Simplex Method . es +. 21-22

Chapter 22 Planning for Capital Expenditures....0..0.......0.4 te. 928

Learning Objectives E i tg ae 2-1

Planning for Capital Expenditures rn 1

Cost Accounting 14" Edition

Relating Plans to Objectives... .. rer

Structuring the Framework

Searching for Proposals . : .

Budgeting Capital Expenditures. egnexamns

Requesting Authority for Expenditures

Ethical Considerations . ee

Evaluating Capital Expenditures

Classification of Capital Expendiaes

Estimating Cash Flows

Inflationary Considerations in the Estimation of Cash Flows...

Income Tax Considerations in the Estimation of Cash Flows

Economic Evaluation of Cash Flows ...... er

Controlling Capital Expenditures .......+.+ ce

Control While in Process -

Follow-up of Project Results,

Chapter 23 Economic Evaluation of Capital Expenditures ..

Learning Objectives

‘The Cost of Capital .

Economic Evaluation Techniques

The Payback Period Method :

‘The Accounting Rate of Retuin Method

‘The Net Present Value Method

The Internal Rate of Return Method

The Error Cushion

Purchasing versus Leasing

Chapter 24 Decision Making Under Uncertainty .

Learning Object beens

Using Probabilities in Decision Making.

Determining the Best Strategy Under Uncertainty

Payoff Tables .

Decision Trees .. ae

Continuous Probability Distributions

Monte Carlo Simulations a

Considering Uncertainty in Capital Expenditure Evaluation

Independent Cash Flows. .

Perfectly Correlated Cash Flows

Mixed Cash Flows

Evaluating Investment Risk -

Incorporating Nonquantitative Factors into the Analysis ......0.

ves,

‘Table of Contents

Chapter 25. Profit Performance Measurements and

Glossary .

Intracompany Transfer Pricing .. seesereeserees 25h

Learning Objectives ... veces cee 25e1

Rate of Return on Capital Employed . .

The Formula

‘The Formula’s Underlying Data. .

Using the Rate of Return on Capital Employed. .

Divisional Rates of Return Urine

Graphs as Operating Guides... .

Advantages of Using the Return on Capital Employed

Limitations of Using the Return on Capital Enployea :

Multiple Performance Measures. vee

Management Incentive Compensation Plans

Selecting Performance Measures

Intracompany Transfer Pricing ....... 7

Transfer Pricing Based on Cost

Market-Based Transfer Pricing.

Cost-Plus Transfer Pricing .

Negotiated Transfer Pricing

Arbitrary Transfer Pricing

Dual Transfer Pricing .......

Index . ‘sie eines s ower e 6 ERR GUHA Yate ai seeeeeee EL

PART 1

Costs: Concepts and Objectives

Chapter 1 > Management, the Controller, and Cost Accounting

Chapter 2 > Cost Concepts and the Cost Accounting Information

System

Chapter 3 > Cost Behavior Analysis

Chapter 1

Management, the Controller,

and Cost Accounting

Learning Objectives

After studying this chapter, you will be able to:

1. Model the management process as three interrelated activities: planning, organizing, and

control,

2. Identify and distinguish three kinds of plans: short-range, long-range, and strategic.

3. Identify and differentiate the tasks in which management is aided by information about

costs and benefits.

4, Identify which of the management accountant’s ethical responsibilities apply to partic

ular ethical issue.

5, State the role of the pronouncements of the Cost Accounting Standards Board.

This chapter describes the environment of cost accounting from internal and external per-

spectives. Within the organization, cost accounting is presented as part of the management

function, and the roles of the controller and cost department are discussed. In the external

environment, the certification movement, ethical expectations, and other private and gov-

emmental influences on cost accounting are examined.

Management

5 Management is composed of three groups: (1) operating management, consisting of super

iors: (©) middle management, represented by department heads, division managers, and

branch managers: and (3) executive management, consisting of the president, executive

vice-presidents, and executives in charge of marketing, purchasing, engineering, manufac-

turing, finance, and accounting.

Management consists of many activities, including making decisions, giving orders,

establishing policies, providing work and rewards, and hiring people to carry out polici

Management sets objectives to be achieved by integrating its knowledge and skills with the

abilities of the employees. Planning and control may be the centerpiece of an organiza-

tion’s approach to management. This was true in many organizations in the past

Alternatively, planning and control may be pushed into the background and become almost

invisible to line workers unless a major problem or failure occurs. Even when the planning

and control functions are not in the forefront of day-to-day activities, management still

must effectively perform the basic functions of planning, organizing, and control to be suc

cessful. All three functions require participation by all management levels.

Planning and control are divided for theoretical purposes, just as time frames are divided

imo discrete operating periods. However, these divisions are artificially designed for the

convenience of analysis and do not reflect the dynamic way in which an entity evolves. In

é

bea

aie youwerneg~

Jerproqcave- Fo

cua PMT

Ww ae

Part 1 > Costs: Concepts and Objectives

and interwoven processes. Time

and control are simultaneous, inseparable,

frames such as short- and long-range periods are not clearly distinguishable. Control of an

activity takes place simultaneously with the planning for the next cycle of that same activity,

other planning for longer and shorter cycles of activity, and the control of other activities,

Planning

Planning, the construction of a detailed operating program, is the process of sensing exter

nal opportunities and threats, determining desirable objectives, and employing resources

to accomplish these objectives. Planning investigates the nature of the company’s business,

its major policies, and the timing of major action steps. Eifective planning is based on

analyses of facts and requires reflective thinking, imagination, and foresight.

An example of routine planning is the estimation of an organization's daily cash bal-

ances for the next 30 days, with plans made to buy or sell short-term investments on cer-

tain days so that the cash balance stays within a desired range. This kind of planning is so

routine that the personnel involved are not likely to see that their work involves decisions

of any kind; the decisions are all “programmed.” At the other extreme, examples of non-

routine planning include executive management's responses to the appearance of a new,

major competitor, a new or proposed government regulation of the industry, or a revolu-

ionary new technology. This kind of planning involves so many unique, complex deci-

sions that it defies any attempt to reduce all the relevant variables and the relationships

among them into a “programmable” task

Effective planning requires participation and coordination of all parts of the entity.

Planning includes determining company objectives, which are measurable targets or

results, In stating the objectives of a business, many people first think of profit. Although

Profit is indispensable in a successful business, it is only one goal and cannot be the sole

objective. The companies best able to maximize profits are those that produce goods or

services at an excellent level of quality and value, in a volume, at a time and place, at a

Cost, and at a price that will win cooperation of employees, gain the goodwill of customers,

and meet social responsibilities.

Three kinds of plans are identifiable in business entities. Strategic plans are formu-

lated at the highest levels of management, take the broadest view of the company and its

environment, are the least quantifiable, and are formulated at irregular intervals by an

essentially unsystematic process that begins with identifying an external threat or oppor-

‘unity. Strategic planning decisions shape the future nature of the firm, its products, and its

customers, and they have the potential to alter the external environment

Short-range plans, often called budgets, are sufficiently detailed to permit prepara

tion of budgeted financial statements for the entity as of a future date (typically the end of

the budget period). These plans are prepared through a systematized process, are highly

quantified, are expressed in financial terms, focus mainly on the organization itself by tak-

ing the external environment as a given, and usually are prepared for periods of a month,

quarter, or year.

In addition to these two kinds of plans are the long-range plans prepared by some enti-

ties. Long-range plans, or long-range budgets, typically extend three to five years into the

future. In terms of their degree of detail and quantifiability, long-range plans are an inter-

mediate step between short-range plans and strategic plans. For example, a long-range plan

may culminate in a highly summarized set of financial statements or other quantified

objectives such as targeted financial ratios (e.g. earnings per share) as of a date five years

Chapter 1 >> Management, the Controller, and Cost Accounting 13

in the future. As a long-range plan is revised and refined during the early portions of the

arting point for successive sets of short-range plans.

planning period, it serves as a si

Organizing

Organizing is the establishment of the framework within which activities are to be per-

—> formed. The terms organize and organization refer to the systematization of interdependent

parts into one unit. Organizing requires bringing the many functional units of an enterprise

into a coordinated structure and assigning authority and responsibility to individuals.

Organizing efforts include motivating people to work together for the good of the company.

Organization usually involves the establishment of functional divisions, departments,

sections, or branches. These units are created to permit specialization of labor. A manuf

turing firm, for example, usually consists of three fundamental units: manufacturing, market-

ing, and administration. Within these units, departments are formed according to the nature,

location, and amount of work, the degree of specialization, and the number of employees

Management assigns work to each organizational unit created. An effective division of

work among employees is vital in attaining company objectives. Also important are the

relationships among managers and between superiors and subordinates.

Control

— Control is management's systematic effort to achieve objectives. Activities are continually

legge

Bedeger

s

ron

Panne

ya

monitored to see that results stay within desired boundaries. Actual results of each activ-

ity are compared with plans, and if significant differences are noted, remedial actions may

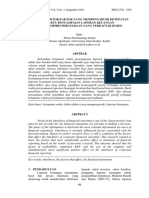

) be taken. Figure 1-1 illustrates the control process, using top management as an example:

Similar relationships exist at all management levels within the organization.

‘The concept of control in business differs from that used in engineering, where con-

trols are designed to work continuously, to use physical measures as their information

inputs, and to work largely independently of human decision making. Thermostats and

fuses are simple examples of engineering controls. In contrast, the control process in busi-

ness always includes a human decision maker. In addition, the information on which con-

trol actions are based includes financial information, and the control activity is periodic

rather than continuous.

Soting

Odectves

sdakeg "assis ans. rettons 2

Policy

Decisions |

y v

‘BOARD OF DIRECTORS | PRESIDENT

o ot MARKETING MANUFACTURING FINANCE ENGINEERING

EXECUTIVE COMMITTEE MANAGER |

, Y Y |

a“ 4+ |

Leasing 10

NewDeciers |___Jesues |g ata Assembled in COST anor BUDGET DEPARTHENTS

wealcatons

FIGURE 1-1 Control Diagram

Part 1 > Costs: Concepts and Objectives

The concept of control in business also differs from that used in military and police

work, in which the need for coercive force is always possible, although undesirable, in

achieving control. In business, control is achieved through others’ actions only with their

cooperat

Authority, Responsibility, and Accountability

Ina small firm, planning and control are performed by a single person, usually the owner

or general manager intimately familiar with the firm’s products, processes, financing, and

customers. In a large company with many organizational units and a variety of products or

services, planning and control are larger tasks. Large firms assign planning and control

functions to many people, so that reports and corrective actions will not be too far removed

from the activity being controlled.

Authority is the power to direct others to perform or not perform activities. Authority

is the key 10 the managerial job and the basis for responsibility. It is the force that binds

the organization together, Authority originates with executive management, which dele-

gates it to lower levels. Delegation is essential to organizational structure. Through dele-

gation, a manager’s area of influence is extended, but the manager remains responsible for

delegated functions because delegation does not remove responsibility.

Responsibility, or obligation, is closely related to authority. It originates principally in

the superior-subordinate relationship in that the superior has the authority to require specific

work from others. If subordinates accept the obligation to perform, they create their own

responsibility. The superior still is ultimately responsible for subordinates’ performance.

One facet of responsibility is aecountability—reporting results to higher authority.

Reporting is important because it enables measuremént of the extent to which objectives

are reached. Usually accountability is imposed on an individual rather than a group. This

principle of individual accountability is well established in both profit and nonprofit organ-

izations. If the organizational structure permits pooling of judgment, responsibility is

fused and accountability nullified.

The Organization Chart

An organization chart shows an entity's principal management positions, helps to define

authority, responsibility, and accountability, and is essential in developing a cost account-

ing system capable of reporting the responsibilities of individuals. The coordinated devel-

opment of a company’s organization with the cost and budgetary system leads to an

approach to accounting and reporting called responsibility accounting

Most organization charts are based on the line-staff concept. The assumption of this

concept is that all positions or functional units can be categorized into two groups: the line,

which makes decisions, and the staff, which gives advice and performs technical functions,

A line-staff organization chart is illustrated in Figure 1-2

Another type of organization chart is based on the functional-teamwork concept of

management, which emphasizes the most important functions of an enterprise: resources,

processes, and human interrelations, The resources function involves the acquisition, dis-

posal, and prudent management of a wide variety of resources—tangible and intangible,

human and physical. The processes function dei ities such as product design,

research and development, purchasing, manufacturing, advertising, marketing, and billing.

een,

vodawy deine

prot

‘Chapter 1 > Management, the Controller, and Cost Accounting 1-5

STOCKHOLDERS

BOARD OF DIRECTORS

PRESIDENT SECRETARY

— oe ——.——————j

| | | |

VICE-PRESIDENT «VICE-PRESIDENT —_ VICE-PRESIDENT

‘WaRKETING WANUPRETURING "RESEARCH AND TREASURER CONTROLLER

DeveLomMeNT

| |

| \

WORKS MANAGER WORKS MANAGER DjAECTOR GENERAL cost

PRODUCTION PERNT ENGINEERING INOUSTHIAL RELATIONS ACCOUNTING | ACCOUNTING

OPERATING | EMPLOYMENT TAXES INTERNAL

PLANNING —}—

| sranoanos ene AUDITING

| DEPARTMENTS

wer

OPERATIONAL DEPARTMENTS eLEARES GENERAL

‘OFFICE

t+ | MANAGEMENT

MAINTENANCE — meio

FIGURE 1-2 Organization Chart Based on Line-Staff Concept

‘The human interrelations function directs the company’s efforts concerning the behavior

of people inside and outside the company. A functional-teamwork organization chart is

illustrated in Fi

re |

The Controller’s Participation in Planning and Control

The controller is the executive manager responsible for the accounting function. The con-

troller coordinates management's participation in planning and controlling the attainment

of objectives. in determining the effectiveness of policies, and in creating organizational

structures and processes. The controller also is responsible for observing methods of plan-

ning and control throughout the enterprise and for proposing improvements in them.

Effective control depends on communicating information to management. By issuing

performance reports, the controller advises other managers of activities requiring correc-

tive action, These reports emphasize deviations from a predetermined plan, following the

principle of management by exception. The principle of management by exception is a

belief that managers should be provided with information that directs their attention to

activities that require corrective action. The concept is premised on the belief that man-

agers do not have time to review every action of every subordinate nor to consult with cach

subordinate prior to each action. This is not to say that managers’ main task is correcting

probiems or “putting out fires.” but simply that managers need not take actions in the many

areas where the work is proceeding as planned

1-6 Part 1 > Costs: Concepts and Objectives

STOCKHOLDERS

BOARD OF DIRECTORS

| DIRECTOR OF

qn ce iin cee

Mes ire foe

oncetes oa peat

ASSISTANT.

oinecToa oF

DIRECTOR OF DIRECTOR OF DIRECTOR OF MANAGERIAL

RESOURCES PROCESS ACTIVITIES wuNan ee

| INTERRELATIONS

ASSISTANT ASSISTANT ASSISTANT

DIRECTOR OF: DIRECTOR OF DIRECTOR OF;

ua Resounces PRODUCTS & SERVICES |- STOCKHOLDER & FINANCIAL

ance MANUFACTURING COMMUNITY RELATIONS

PHYSICAL ASSETS MARKETING LABOR & EMPLOYEE RELATIONS

INTANGIBLE ASSETS CUSTOMER RELATIONS

PUBLIC & COMMUNITY RELATIONS

GGOVERHENT RELATIONS

FIGURE 1-3 Organization Chart Based on Functional-Teamwork Concept

Using the accounting system and other systems, the controller provides information

for planning a company’s future and for controlling its activities, This information goes far

beyond the basic financial statements. Investors, government agencies, and other external

parties also receive information by which management’ effectiveness may be judged. This

information is usually communicated to external users by means of quarterly and annual

reports that include financial statements but lack the depth of explanatory detail available

to internal decision makers.

The Cost Department

The cost department, under the direction of the controller, is responsible for gathering,

compiling, and communicating information regarding a company's activities. This depart-

ment analyzes costs and issues performance reports and other decision-making data to

managers for use in controlling and improving operations. Analysis of costs and prepara-

tion of reports are facilitated by proper division of functions within the cost department

and by coordination with other accounting functions, such as general accounting. The cost

Chapter 1 > Management, the Control

und Cost Accounting, 17

department also coordinates with the manufacturing, personnel, treasury, marketing, pub-

lations, legal, and other departments.

The manufacturing departments, under the direction of engineers and factory superin-

tendents, design and control production. In research and design, cost estimates are used in

deciding whether to accept, improve. or reject a design. Likewise, scheduling, production,

and inspection are measured for etficiency in terms of quantity, quality, costs, and, to the

extent practical, benefits,

The personnel department interviews and selects employees and maintains personnel

»* records, including wage rates. This information forms the basis for computing payroll

costs and for calculating the labor-related costs of any activity, service, or good produced

The treasury department is responsible for financial administration of a company. In

Scheduling cash requirements and expectations, it relies on budgets and related reports

from the cost department.

‘The marketing department needs a quality product at a competitive price to attra

tomers, Prices generally are not set merely by adding a predetermined percentage to cost, but

costs cannot be ignored. Marketing managers use cost data to determine which products are

profitable and to determine sales policies, plan promotions, and evaluate market segments

The public relations department has the function of maintaining good relations

between the company and its public, especially its customers and stockholders. Points of

friction are likely to include prices, wages, profits, and dividends. The cost department pro-

vides information for public releases concerning these areas

The legal department uses cost information as an aid in maintaining compliance with

contracts and laws, including the Equal Pay Act, union contracts, the Robinson-Patman

Act. the Employee Retirement Security Act of 1974, and the income tax, social security,

and unemployment compensation laws, all of which can affect costs.

cus-

The Role of Cost Accounting

In the past, cost accounting was widely regarded as the calculation of the inventory cost

presented in the balance sheet and cost of goods sold figure in the income statement. This

view limits the broad range of information that managers need for decision making to

nothing more than the product cost data that satisfy external reporting rules. Examples of

these rules are income tax regulations, accounting rules prescribed for goverument con-

tracts, and generally accepted accounting principles (GAAP). Such a restrictive definition

is inappropriate today and is certainly an inaccurate description of the uses of cost infor-

* mation, Cost accounting furnishes management with necessary tools for planning and con-

trolling activities, improving quality and efficiency, and making both routine and strategic

decisions. The collection, presentation, and analysis of information regarding costs and

benefits helps management accomplish the following tasks:

Creating and executing plans and budgets for operating under expected competi-

tive and economic conditions. An important aspect of plans is their potential for

motivating people to perform in a way consistent with company goals.

Establishing costing methods that permit control of activities, reductions of costs,

and improvements of quality.

3. Controlling physical quantities of inventory, and determining the cost of each

product or service produced for the purpose of pricing and.for evaluating the per-

ya A formance of a product, department, or division.

18

Part 1 > Costs: Concepts and Objectives

aot 4. Determining company costs and profit for an annual accounting period or a shorter

ow period. This includes determining the cost of inventory and cost of goods sold

according to external reporting rules

Choosing among two or more short-run or long-run alternatives that might alter

revenues or costs.

Notice the distinction between determining the cost of a product in.task 3 and the cost

ing of inventory for external reporting in task 4. The distinction is that the cost of a prod-

uct (task 3) can be calculated for many purposes, including predicting costs and making

decisions, while inventory costing for external reporting (task 4) deals with satisfying

external reporting rules. In very simple production settings, the two are often the same. For

example, if all units produced in a facility are alike, any reasonable way of dividing the

total cost equally among the units will suffice for both external reporting and for many

decision-making purposes. Although the costs incurred in such a setting may be large and

complex, the product line is extremely Simple—all units are identical—and so the costing

of each unit of the product is simple, too. This is the model of manufacturing that is often

assumed in economic theory.

Many actual manufacturing settings are much more complicated than the economist’s

model. A firm can produce a diverse product line in a single facility, where the same

resources are used very differently in producing different products. In addition to a diverse

product line, some settings exhibit complex cost structures, and the combination of the two

makes it difficult to predict or identify the costs of producing one unit of one product. In

these settings, the challenge to cost accounting is to measure the cost of all the things con-

sumed in making a unit or lot of a product. When precision is needed in such a calculation

(for example, in quoting a fiercely competitive price to a customer who needs a million

units or batches), then the level of detail needed in calculating cost goes far beyond any-

thing required by external reporting rules

Service businesses provide excellent examples of the distinction between tasks 3 and

4. Consider a walk-in medical clinic, auto oil-change and lubrication shop, ot hairdresser,

in which all jobs are of such short duration that there are no fully or partially completed

Jobs on hand at the end of a business day. In such a setting, the inventory costing role in

external reporting (task 4) simply does not exist, but product costs (task 3) still must be

known by management to permit decisions such as which services to provide and what

prices to charge.

In sum, the information needs of managers range from simple to complex, and depend

on the nature of products and processes, the particular decision to be made, the competi-

tive environment, and other factors. In contrast, the nature of inventory costing required in

external reporting is constant through time unless an external reporting rule is changed. In

addition, inventory costing must satisfy only the following: (1) it must be based on actual

historical costs, verifiable through documented transactions; (2) it must be consistent from.

period to period; and (3) it must include all manufacturing costs in the cost calculated for

cach unit of output

The simplest cost accounting systems can generate product cost data that satisfy

external reporting rules (task 4), There is a dangerous tendency among some executiv

to endorse only the cost accounting effort needed for external reporting, ignoring man-

agers’ potentially much greater needs for detailed, reliable product cost information

(task 3)

Chapter 1 > Management, the Controller, and Cost Accounting 19

Budgeting

The budget is the quantified. writien expression of management's plans. All levels of man-

agement should be involved in ereating it. A workable budget promotes coordination of

personnel, clarification of policies, and crystallization of plans. It also creates greater Inter-

nal harmony and unanimity of purpose among managers and workers.

In recent years, considerable attention has been given to the behavioral implications of

providing managers with data required for planning and control, Budgeting plays an

important role in influencing individual and group behavior at all stages of the manage-

ment process, including (1) setting goals, (2) informing individuals about what they should

ails, (3) motivating desirable performance, (4)

contribute to the accomplishment of the

evaluating performance, and (5) suggesting when corrective action should be taken. In

short, accountants cannot ignore the behavioral sciences (psychology, social psychology,

and sc

ioral function.

Managers’ attitudes toward the budget depend a great deal on relationships within the

cment group. Guided by the company plan, with opportunities for increased com-

pensation, greater satisfaction, and eventually promotion, middle and lower management

can achieve remarkable results. A discordant management group, unwilling to accept the

budget's underlying assumptions, may perform unacceptably.

“The following clements have been suggested as means for motivating personnel to aim

for goals set forth in a budget."

ology) because the decision-making function of accounting is essentially a behav-

man:

maintains a clearly understood relation-

A compensation system that builds

ship between results and rewards.

2. A system for performance appraisal that employees understand with regard to

their individual effectiveness and key results, their tasks and their responsibilities,

their degree and span of influence in decision making, as well as the time allowed

to judge their results

3. A system of communication that allows employees to query their superiors with

trust and honest communication.

A system of promotion that generates and sustains employee faith in its validity

and judgment

A system of employee support through coaching, counseling, and career planning.

‘A system that considers not only company objectives, but also employees’ skills

and capacities.

‘A system that does not settle for mediocrity, but reaches for realistic and attainable

Standards, stressing improvement and providing an environment in which the con-

cept of excellence can grow

Empirical research in this field contributes to a useful understanding of the inter-

relationships of budgeting and human behavior, Numerous research projects have been

undertaken and more are needed. Illustrating the insights that such studies provide, one

reseurch project indicated that budgetary participation and budget goal clarity had signifi-

cant positive effects on managers’ attitudes and performance, while excessively high goals

had adverse effects. The study also found that budgetary evaluation and feedback exerted

41 €. Sussman, “Motivating Financial Personne!” The Journal of Accountancy, Vel. 141, No.2, p &

1-10 Part 1 > Costs: Concepts and Objectives

only weak effects on managers’ attitudes and performance.’ Budgeting is examined in

depth in Chapters 15, 16, and 17.

Controlling Costs

fic individuals who are also

% ~ The responsibility for cost control should be assigned to spk

3) gs eg accountable for budgeting the costs under their control. Each manager's responsibilities

gf FF > should be limited to the cosis and revenies Ihat are conteallabie by the manager, and per-

YS 2 formance is generally measured by comparing actual costs and revenues with the budget.

Re OX Systems designed to achieve these goals are called responsibility accounting systems.

¢ To aid in controlling costs, the cost accountant may use predetermined cost amounts

ey called standard costs. Standard costs also can be the foundation for budgets and cost

reports, Standard costs are examined in Chapters 18 and 19.

Another important aspect of cost control is the identification of the costs of different

s rather than the costs of different departments and products. In a complex produc

tion setting, often only a small fraction of total activity actually adds value to the final

&,, put. Other activities, called non-value-added activities, generally are a result of the

3 ¥ complexity of production settings and are not specific to the production of any particular

© © good or service. Examples of non-value-added a 's in a factory are retrieving, han

dling, and moving materials; expediting; holding inventories; and reworking defective

Reporting the costs of non-value-added activities is a first step toward their reduc-

tion or elimination

Pricing

Management's pricing policy ideally should assure long-run recovery of all costs and a

profit, even under adverse conditions. Although supply and demand usually are determin-

ing factors in pricing, the establishment of a profitable sales price requires consideration

of costs. Competitively bidding on a proposed job, for example, is a difficult pricing deci-

sion if there is little or no past experience with the kind of good or service involved

Determining Profits

Cost accounting is used to calculate the cost of the output sold during a period; this and

other costs are matched with revenues to calculate profits. Costs and profits may be

reported for segments of the firm or for the entire firm, depending on management's needs

and the external reporting requirements.

The matching process involves identifying short-run and long-run costs, and variable

and fixed (capacity) costs. Variable manufacturing costs are assigned first to the units man-

ufactured and then matched with revenue when those units are sold. (Nonmanufacturing

costs, both fixed and variable, typically are matched with revenues of the period.) Fixed

manufacturing costs are matched with revenues by one of the following alternatives:

*lzzeltin Kenis, “Etfects of Budgetary Goal Characteristics on Managerial Attitudes and Perlormance; The

Accounting Review, Vol, LIV, No, 4, pp. 707-721

Chapter 1 > Man

troller, and Cost Accounting 1a

1. Matching total fixed costs of a period with revenues of that period; this alternative

is called direct costing or variable costing

Matching some or ali of the fixed manufacturing co:

is are then expensed as part of the income statement’s cost of

th units of product; these

ods sold fig

ce

ony

WG ure when the related units are sold. This alternative is called absorption costing

gan

and is required for GAAP and income tax reporting,

These alternatives give the same reported results in the long run but yield a different

profit for individual short periods such as years. These alternatives are examined in more

detail in Chapter 20.

Choosing Among Alternatives

Cost accounting provides information concerning the different revenues and costs that

might result from alternative actions. Based on this information, management makes short-

range and long-range decisions concerning entering new markets, developing new prod-

ucts, discontinuing individual products or whole product lines, buying versus making @

necessary component of a product, and buying versus leasing equipment. In the decisions

ting products, reliable cost information is espe-

cially crucial to the competitive success of the firm, Misstated costs create the possibility

that undesirable business might be initiated or continued and desirable business rejected.

In these ways. cost information plays an essential role in identifying, evaluating, and

nization.

to add new products and discontinue ex

selecting strategies for the o1

Cost Accounting and Manufacturing Technology

Factory automation, which has spread rapidly, results in capital-intensive processes, often

with computerized systems that use robot-controlled machinery. Automation is expensive,

however, and is not a cure-all for an obsolete production process. Many problems are

rooted in systems and attitudes, and by focusing on those areas first, the firm can reap even

greater gains from automation, In automating a process, employee involvement and moti-

vation are the first step. and simplification of the existing process is second. Only then

should a large investment in automation be considered, Innovative and experimental appli-

cations, including changes in systems and attitudes, now permeate business from product

cturing process, inventory management, qual-

design to production scheduling, the manuf:

ity control, and strategic decision making.

Changes in manufacturing technology have spawned a long list of new terminology,

including computer-aided design (CAD), computer-aided engineering (CAE), computer-

aided manufacturing (CAM), just-in-time production (JIT), computer numerical control

machinery (CNC), optimized production technology (OPT), the theory of constraints

(TOC), fiexible manufacturing systems (FMS), and computer-integrated manufacturing

(CIM). These innovations are discussed in appropriate places throughout this text.

2 the nature of costs, producing, for example, lower inv

less use of labor, and increasing levels of fixed costs. In thi

challenged to evolve and take on increased relevance.

tion has become a competitive weapon.

ntory

new environment, cost

echnology is chang

level

accounting systems are bei

Reliable cost accounting infor

12 Part 1 > Costs: Concepts and Objectives

Certification and Ethics

Persons engaged in cost accounting or other accounting functions within an organization are

referred to as “management iccountants” or “financial managers.” They may also be referred

to by their professional certifications, Certified Management Accountant (CMA) and

Certified Financial Manager (CFM), which are formal recognition of professional compe-

tence and educational achiovement in the field. Requirements for the CMA and CFM certifi-

cates include passing demanding examinations offered by the Institute of Ce

Management Accountants and completing two years of professional experienc

In 1983 the National Association of Accountants—later renamed the Institute of

Management Accountants (IMA)—issued a code of ethics, Although individuals practicing

as independent certified public accountants had long been subject to a code of conduct, these

standards were the first ever issued for management accountants. This code of ethics was

‘modified in 1997. The result, Standards of Ethical Conduct for Practitioners of Management

Accounting and Financial Management, is presented in Exhibit 1-1. Among the published

codes of ethics of various professional groups, these Standards of Ethical Conduct are dis-

tinct in that they prescribe steps to be followed in resolving an ethical conflict.

Influence of Private and Governmental Organizations

Occasionally the research and pronouncements of professional organizations contribute to

the development of cost accounting. These organizations include the Financial Accounting

Standards Board (FASB), the Governmental Accounting Standards Board (GASB), the

American Institute of Certified Public Accountants (AICPA), the Institute of Management

Accountants (IMA), the American Accounting Association (AAA), and the Financial

Executives Institute (FED). In addition, cost accounting can be influenced by university

esearch, individuals, and private companies.

The rapid growth of international business has led several international organizations

to become involved in accounting, including cost accounting. These organizations include

the International Accounting Standards Board (IASB) and the Organization for Economic

Cooperation and Development (OECD).

In the public sector, there are federal, state, and local government regulations embodied

in many accounting systems. At the national level, the Internal Revenue Service (IRS) and the

Cost Accounting Standards Board (CASB) have a significant influence on cost accounting

Taxation

Federal income tax liability is determined according to the Internal Revenue Code (Title 26

of the United States Code) as enacted and amended by Congress. The Treasury Department,

acting under authority granted by Congress, issues regulations (Title 26 of the Code of

Federal Regulations) which interpret the tax statutes enacted by Congress. The Internal

Revenue Service, a branch of the Treasury Department, collects taxes and issues rulings and

Procedures as guidance to taxpayers. Revenue Rulings and Revenue Procedures are pub-

lished weekly in the Jniernal Revenue Bullet: and semiannually in the Cumulative Bulletin

The influence of these statutes, regulations, rulings, and procedures cannot be ignored.

Similar considerations apply for state and local income taxation. Management's planning

decision making must consider tax consequences at all these levels.

Chapter 1 > M

agement, the Controller, and Cost Accounting

113

Practitioners of management accounting and financial man-

agement have an obligation to the organizations they serve,

their profession, the public, and themselves to maintain the

highest standards of ethical conduct. In recognition of this,

obligation, the Institute of Management Accountants has

promulgated the following standards of ethical conduct for

practitioners of management accounting and financial man-

agement. Adherence to these standards, both domestically

land internationally, is integral to achieving the Objectives of

Management Accounting. Practitioners of management

accounting and financial management shall not commit acts

contrary to these standards nor shail they condone the com-

mission of such acts by others within their organizations.

Competence”

Practitioners of management accounting and financial

management have a responsibilty to:

~ Maintain an appropriate level of professional competence

by ongoing development oftheir knowledge and skills,

~ Perform their professional duties in accordance with rel

‘vant laws, regulations, and technical standaves.

~ Prepare complete and clear reports and recommenda-

tions after appropriate analysis of relevant and reliable

information Sat Aegan) va

R taper or

Confidentiality

Practitioners of management accounting and financial

management have a responsibiliy to:

Retrain from disclosing confidential information

acquired in the course of their work except when

authorized, unless legally obligated to d0 so.

» Inform subordinates as appropriate regarding the con-

fidentialty of information acquired in the course ot

their work and monitor their activities to assure the

maintenance of that confidentiality

“> Retrain from using or appearing to use confidential

information acquired in the course of their work for

unethical or illegal advantage either personally or

through third parties,

Integrity ~

Practitioners of management accounting and financial

management have a responsibilty to:

> Avoid actual or apparent conllcts of interest and advise

all appropriate parties of any potential conflict.

“= Refrain from engaging in any activity that would preju-

dice their ability to carry out their duties ethically.

“+ Refuse any gift, favor, or hospitality that would influ-

tence or would appear to influence their actions.

“> Refrain from either actively or passively subverting the

attainment of the organization's legitimate and ethical

objectives,

Recognize and communicate professional limitations or

other constraints that would preclude responsible judg-

‘ment or successful performance of an activity.

> Communicate unfavorable as well as favorable infor

mation and professional judgments or opinions.

> Refrain from engaging in or supporting any activity

that would discredit the profession.

Objectivity ~

Practitioners of management accounting and financial

‘management have a responsibilty 10:

= Communicate information faitly and objectively

“> Disclose fully all relevant information that could rea-

sonably be expected to influence an intended user's,

understanding of the reports, comments, and recom-