You might also like

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- 4 Common Types of Financial Statements To Know: 1. What Is A Statmemt of Financial Position (Balance Sheets) ?Document15 pages4 Common Types of Financial Statements To Know: 1. What Is A Statmemt of Financial Position (Balance Sheets) ?Ray Allen Uy100% (1)

- Fabm 1Document12 pagesFabm 1Antonio RaveloNo ratings yet

- Fabm 2Document7 pagesFabm 2Akaashi KeijiNo ratings yet

- Accounting AssignmentDocument2 pagesAccounting AssignmentMarvel TatingNo ratings yet

- Financial StatementsDocument4 pagesFinancial StatementsConrad DuncanNo ratings yet

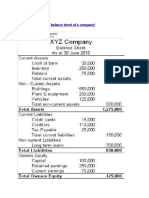

- Balance SheetDocument6 pagesBalance Sheetddoc.mimiNo ratings yet

- Economic Entity AssumptionDocument4 pagesEconomic Entity AssumptionNouman KhanNo ratings yet

- Lesson 1.1: Intro & SFPDocument7 pagesLesson 1.1: Intro & SFPIshi MaxineNo ratings yet

- Fabm2 PPTG1Document65 pagesFabm2 PPTG1chrisraymund.bermudoNo ratings yet

- Accounting Review 3Document1 pageAccounting Review 3Scouty TheboyNo ratings yet

- Finman CHPT 1Document12 pagesFinman CHPT 1Rosda DhangNo ratings yet

- Accounting SummarizeDocument3 pagesAccounting Summarizeghulam aliNo ratings yet

- CH 11Document30 pagesCH 11Jean-Paul MoubarakNo ratings yet

- ReportDocument4 pagesReportEuneze LucasNo ratings yet

- Reading and Interpreting Banks Balance SheetDocument8 pagesReading and Interpreting Banks Balance SheetRavalika PathipatiNo ratings yet

- SCRIPTDocument5 pagesSCRIPTJohn LucaNo ratings yet

- A Balance SheetDocument3 pagesA Balance SheetKarthik ThotaNo ratings yet

- Chapter 4 Underlying AssumptionsDocument7 pagesChapter 4 Underlying AssumptionsMicsjadeCastilloNo ratings yet

- Elements of Financial Statements & The Recognition Criteria For Assets & LiabilitiesDocument13 pagesElements of Financial Statements & The Recognition Criteria For Assets & LiabilitiesdeepshrmNo ratings yet

- Balance Sheet Assets Liabilities Income StatementDocument4 pagesBalance Sheet Assets Liabilities Income Statementmadhav5544100% (1)

- Financialfeasibility 200129141325Document20 pagesFinancialfeasibility 200129141325Princess BaybayNo ratings yet

- Reading The Balance SheetDocument4 pagesReading The Balance Sheetsandipghosh123No ratings yet

- Social AccountingDocument28 pagesSocial Accountingfeiyuqing_276100% (1)

- Financial Stements Analysis-2Document30 pagesFinancial Stements Analysis-2Mega capitalmarketNo ratings yet

- Balance SheetDocument4 pagesBalance SheetPFENo ratings yet

- Balance SheetDocument8 pagesBalance SheetadjeponehNo ratings yet

- Statement of Financial PositionDocument11 pagesStatement of Financial Positionshafira100% (1)

- How The Balance Sheet WorksDocument5 pagesHow The Balance Sheet Worksrimpyagarwal100% (1)

- The Elements of A Financial StatementDocument2 pagesThe Elements of A Financial StatementAnunobi JaneNo ratings yet

- Financial-Analysis-and-Reporting Study Material-Central Mindanao UniversityDocument22 pagesFinancial-Analysis-and-Reporting Study Material-Central Mindanao UniversityAngelito Han-awon100% (2)

- FINANCIAL ACCOUNTING - AsbDocument9 pagesFINANCIAL ACCOUNTING - AsbMuskaanNo ratings yet

- Financial Statement AnalysisDocument4 pagesFinancial Statement AnalysisYasir ABNo ratings yet

- Faculty of Businee and EconomicsDocument9 pagesFaculty of Businee and EconomicsEfrem WondaleNo ratings yet

- Financial Accounting and Reporting (: Assignment #1)Document4 pagesFinancial Accounting and Reporting (: Assignment #1)Mary Elouise BundaNo ratings yet

- Pre Reading To Basic FinancialDocument2 pagesPre Reading To Basic Financialyerio.dwiyantoNo ratings yet

- Chapter 3 HandoutsDocument9 pagesChapter 3 HandoutsHonie Jane D. AmerilaNo ratings yet

- Understand Basic Accounting TermsDocument5 pagesUnderstand Basic Accounting Termsabu taherNo ratings yet

- What Are Financial StatementsDocument3 pagesWhat Are Financial StatementsShelamae AlabastroNo ratings yet

- MTTM 05 2021Document10 pagesMTTM 05 2021Rajni KumariNo ratings yet

- Financial StatementsDocument2 pagesFinancial StatementsgrazielafgNo ratings yet

- Chap 3-5Document5 pagesChap 3-5jessa mae zerdaNo ratings yet

- Chapter 4 Conceptual Framework - Financial Statements and Reporting Entity Underlying AssumptionsDocument3 pagesChapter 4 Conceptual Framework - Financial Statements and Reporting Entity Underlying AssumptionsEllen MaskariñoNo ratings yet

- How To Read Balance SheetDocument6 pagesHow To Read Balance SheetDanish SheikhNo ratings yet

- Balance Sheet (Research)Document3 pagesBalance Sheet (Research)Joycel MerdegiaNo ratings yet

- Chapter 3 SummaryDocument3 pagesChapter 3 SummaryDarlianne Klyne BayerNo ratings yet

- Chapter 5 Financial StatementsDocument8 pagesChapter 5 Financial StatementshwhwhwhjiiiNo ratings yet

- Corporate FininanceDocument10 pagesCorporate FininanceMohan KottuNo ratings yet

- Shareholders' EquityDocument2 pagesShareholders' EquityLJBernardoNo ratings yet

- The Balance SheetDocument7 pagesThe Balance Sheetsevirous valeriaNo ratings yet

- Interview StudyDocument34 pagesInterview StudyJyotirmay SahuNo ratings yet

- W3 Module 5 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 3Document6 pagesW3 Module 5 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 3leare ruazaNo ratings yet

- What Is Cash FlowDocument31 pagesWhat Is Cash FlowSumaira BilalNo ratings yet

- Balance Sheet Definition - InvestopediaDocument3 pagesBalance Sheet Definition - InvestopediaAnjuRoseNo ratings yet

- Types of Financial Statements: Statement of Profit or Loss (Income Statement)Document4 pagesTypes of Financial Statements: Statement of Profit or Loss (Income Statement)LouiseNo ratings yet

- Tutorial 3 (Financial Management)Document2 pagesTutorial 3 (Financial Management)muthuNo ratings yet

- ACC321Document6 pagesACC321Allysa Del MundoNo ratings yet

- FABM2 STATEMENT OF FINANCIAL POSITION AbstractionDocument5 pagesFABM2 STATEMENT OF FINANCIAL POSITION AbstractionIrish Shyne IINo ratings yet

- Module-1 Fabm2Document7 pagesModule-1 Fabm2Kate ArenasNo ratings yet

- Restructuring and ReschedulingDocument16 pagesRestructuring and ReschedulingJeyashankar Ramakrishnan100% (1)

- Chapter 2: Accounting Statements and Cash FlowDocument4 pagesChapter 2: Accounting Statements and Cash FlowBarbara H.CNo ratings yet

- Test Bank 27.1Document4 pagesTest Bank 27.1Perbielyn BasinilloNo ratings yet

- 資產 (Assets) 業主權益 (Owner's Equity) : (Paid-in capital in excess of par value)Document1 page資產 (Assets) 業主權益 (Owner's Equity) : (Paid-in capital in excess of par value)顏子傑No ratings yet

- EB-TopR2R KPIs We Should Be TrackingDocument13 pagesEB-TopR2R KPIs We Should Be TrackingAndrewNo ratings yet

- BVS Sample Valuation Report 01 1 PDFDocument59 pagesBVS Sample Valuation Report 01 1 PDFAmygoNo ratings yet

- Advanced aCCOUNTING 2 SOLMAN PDFDocument418 pagesAdvanced aCCOUNTING 2 SOLMAN PDF杉山未来100% (1)

- Business Plan On BeweryDocument24 pagesBusiness Plan On BeweryAjay SahNo ratings yet

- 2233 - EN TNG Financial Statements 31-12-2015Document42 pages2233 - EN TNG Financial Statements 31-12-2015Nhật Linh LêNo ratings yet

- Car Wash Business Plan: Executive SummaryDocument12 pagesCar Wash Business Plan: Executive SummaryRaj KambojNo ratings yet

- Reviewer Partnership Formation 1Document6 pagesReviewer Partnership Formation 1Joshua SolayaoNo ratings yet

- MOB Unit 1 SyllabusDocument18 pagesMOB Unit 1 SyllabussadNo ratings yet

- Cpa Aditional CorlynDocument34 pagesCpa Aditional CorlynAlexaMarieAliboghaNo ratings yet

- CH 11Document6 pagesCH 11Saleh RaoufNo ratings yet

- Creditmanual NepaliDocument462 pagesCreditmanual NepaliNabin SijaliNo ratings yet

- Alternative Models of Bank PerformanceDocument50 pagesAlternative Models of Bank Performancechikku8764No ratings yet

- ALCO and Operational Risk Management at CITI Bank: Name Student ID Instructor DateDocument16 pagesALCO and Operational Risk Management at CITI Bank: Name Student ID Instructor DateAbrarNo ratings yet

- DDT - Chapter 1Document47 pagesDDT - Chapter 1Suba ChaluNo ratings yet

- Management Accounting - Fund Flow AnalysisDocument30 pagesManagement Accounting - Fund Flow AnalysisT S Kumar KumarNo ratings yet

- Trend Analysis, Horizontal Analysis, Vertical Analysis, Balance Sheet, Income Statement, Ratio AnalysisDocument4 pagesTrend Analysis, Horizontal Analysis, Vertical Analysis, Balance Sheet, Income Statement, Ratio Analysisnaimenim100% (1)

- WAPO1Q11Document7 pagesWAPO1Q11Inde Pendent LkNo ratings yet

- FinanceDocument6 pagesFinancesuhana.khanNo ratings yet

- Debt Reduction Calculator 10Document6 pagesDebt Reduction Calculator 10mmahaliNo ratings yet

- BES 001 ReviewDocument3 pagesBES 001 ReviewAC Joyce SaulNo ratings yet

- Module 1 Current LiabilitiesDocument13 pagesModule 1 Current LiabilitiesLea Yvette SaladinoNo ratings yet

- TAKE HOME EXAM Partnership LiquidationDocument22 pagesTAKE HOME EXAM Partnership LiquidationMaria Kathreena Andrea AdevaNo ratings yet

- Cash Inflow and OutflowDocument6 pagesCash Inflow and OutflowMubeenNo ratings yet

- Sem-5 10 BCOM HONS DSE-5.2A CORPORATE-ACCOUNTING-0758Document5 pagesSem-5 10 BCOM HONS DSE-5.2A CORPORATE-ACCOUNTING-0758hussain shahidNo ratings yet

- PT Gihon Telekomunikasi Indonesia TBK Dan Entitas Anak / and SubsidiaryDocument62 pagesPT Gihon Telekomunikasi Indonesia TBK Dan Entitas Anak / and SubsidiaryDhen NurdiansyahNo ratings yet

- ExercisesDocument13 pagesExercisesalyNo ratings yet