You might also like

- Cadajas vs. People, GR No. 247348 (2021)Document2 pagesCadajas vs. People, GR No. 247348 (2021)ace042363No ratings yet

- Case Digest - Corporation LawDocument14 pagesCase Digest - Corporation LawAiko Dalagan100% (1)

- Central Bank V CADocument1 pageCentral Bank V CAchaNo ratings yet

- Foreclosure Attorney Retainer AgreementDocument12 pagesForeclosure Attorney Retainer AgreementB_KLAWGROUP100% (1)

- ANG TIBAY Petitioners, vs. The Court of Industrial Relations RespondentsDocument7 pagesANG TIBAY Petitioners, vs. The Court of Industrial Relations Respondentsme1204No ratings yet

- Set 8 - Bar Ops 2Document20 pagesSet 8 - Bar Ops 2jojo50166No ratings yet

- Pio Barretto Realty Development Corporation V. Court of AppealsDocument2 pagesPio Barretto Realty Development Corporation V. Court of AppealsTherese GitganoNo ratings yet

- Aldaba vs. COMELEC, G.R. No. 188078, January 25, 2010Document1 pageAldaba vs. COMELEC, G.R. No. 188078, January 25, 2010Di ko alamNo ratings yet

- Loan Calculator ExcelDocument16 pagesLoan Calculator ExcelAtif NazirNo ratings yet

- Wills Transcription 1 PDFDocument88 pagesWills Transcription 1 PDFAiko DalaganNo ratings yet

- Metrobank v. SF Naguiat MDocument2 pagesMetrobank v. SF Naguiat MGab SollanoNo ratings yet

- Dickinson V Del SolarDocument2 pagesDickinson V Del SolarAiko Dalagan100% (2)

- Doctrine:: Bank of The Philippine Islands v. Reynald Suarez GR NO 167750 - March 15, 2010 - CARPIO, JDocument2 pagesDoctrine:: Bank of The Philippine Islands v. Reynald Suarez GR NO 167750 - March 15, 2010 - CARPIO, JJORLAND MARVIN BUCUNo ratings yet

- Banking Law Case DigestsDocument4 pagesBanking Law Case DigestsPatricia PinedaNo ratings yet

- Fidelity Savings and Mortgage Bank Vs CenzonDocument1 pageFidelity Savings and Mortgage Bank Vs Cenzoncmv mendozaNo ratings yet

- Tagolino V HRET Case DigestDocument4 pagesTagolino V HRET Case DigestJose Ignatius D. PerezNo ratings yet

- 89planters Development Bank v. Lopez (Mier - Keith Jasper)Document2 pages89planters Development Bank v. Lopez (Mier - Keith Jasper)Keith Jasper MierNo ratings yet

- Juliet Dano V Comelec and Digal - Case DigestDocument3 pagesJuliet Dano V Comelec and Digal - Case DigestAnonymous lokXJkc7l7No ratings yet

- Case Digest - FRIADocument13 pagesCase Digest - FRIAAiko DalaganNo ratings yet

- Arnado Vs COMELEC DigestDocument3 pagesArnado Vs COMELEC DigestAriza ValenciaNo ratings yet

- Case Digest - Transportation LawDocument14 pagesCase Digest - Transportation LawAiko DalaganNo ratings yet

- Altarejos Vs COMELECDocument2 pagesAltarejos Vs COMELECJL A H-DimaculanganNo ratings yet

- Aglipay Vs Ruiz G.R. No. L-45459 March 13, 1937Document4 pagesAglipay Vs Ruiz G.R. No. L-45459 March 13, 1937Allaylson chrostian100% (1)

- AASJS - Calilung v. DatumanongDocument1 pageAASJS - Calilung v. DatumanongRaymond RoqueNo ratings yet

- Kilosbayan V Morato - Art8Sec1Document2 pagesKilosbayan V Morato - Art8Sec1Kiana AbellaNo ratings yet

- Fort Bonifacio Development Corp v. CIR, G.R. No. 173425, 2013 Case DigestDocument4 pagesFort Bonifacio Development Corp v. CIR, G.R. No. 173425, 2013 Case Digestbeingme2No ratings yet

- CITYSTATE SAVINGS BANK, Petitioner, vs. TERESITA TOBIAS and SHELLIDIE VALDEZ, Respondents.Document12 pagesCITYSTATE SAVINGS BANK, Petitioner, vs. TERESITA TOBIAS and SHELLIDIE VALDEZ, Respondents.Franz Raymond Javier AquinoNo ratings yet

- Citystate Savings Bank vs. Teresita Tobias and Shellidie ValdezDocument2 pagesCitystate Savings Bank vs. Teresita Tobias and Shellidie ValdezJunelyn T. Ella100% (1)

- De Silva Cruz V People Anthony de Silva Cruz vs. People of The PhilippinesDocument9 pagesDe Silva Cruz V People Anthony de Silva Cruz vs. People of The PhilippinesAdrian KitNo ratings yet

- PNB vs. GonzalesDocument1 pagePNB vs. GonzalesMaggi BonoanNo ratings yet

- Nacar v. Gallery FramesDocument2 pagesNacar v. Gallery FramesJave Mike AtonNo ratings yet

- Habana vs. RoblesDocument2 pagesHabana vs. RoblesGabrielle Dayao100% (1)

- Cloma Vs CADocument2 pagesCloma Vs CARachel GeeNo ratings yet

- Maliksi V ComelecDocument20 pagesMaliksi V ComelecNika RojasNo ratings yet

- Mid-Terms Sales Exams Part IDocument8 pagesMid-Terms Sales Exams Part IEppie Severino50% (2)

- Case Digest - New Central Bank ActDocument14 pagesCase Digest - New Central Bank ActAiko DalaganNo ratings yet

- CO V Deportation BoardDocument2 pagesCO V Deportation BoardCelinka ChunNo ratings yet

- LegRes 021924 Case DigestDocument6 pagesLegRes 021924 Case DigestGenesis TuppalNo ratings yet

- Citystate Savings Bank v. Teresita Tobias GR No. 22790 Reyes, JR., JDocument7 pagesCitystate Savings Bank v. Teresita Tobias GR No. 22790 Reyes, JR., JAnastasia ZaitsevNo ratings yet

- Hilao vs. Marcos, 25 F. Ed 1467Document2 pagesHilao vs. Marcos, 25 F. Ed 1467Janine Castro100% (1)

- GERONIMOvs COMELECDocument2 pagesGERONIMOvs COMELECyanaNo ratings yet

- Financial Sector Development in AfricaDocument254 pagesFinancial Sector Development in AfricadonoegNo ratings yet

- Election Law Add NTL CasesDocument12 pagesElection Law Add NTL CasesLizanne GauranaNo ratings yet

- 03 GR NO 255099 Beacon Currency Exchange, Inc. v. RepublicDocument1 page03 GR NO 255099 Beacon Currency Exchange, Inc. v. RepublicLawNo ratings yet

- 27 Ricardo B. Bangayan vs. Rizal Commercial Banking CorporationDocument2 pages27 Ricardo B. Bangayan vs. Rizal Commercial Banking CorporationArthur Archie TiuNo ratings yet

- Raytheon v. Rouzie PDFDocument3 pagesRaytheon v. Rouzie PDFJona CalibusoNo ratings yet

- Nogales Vs People of The PhilippinesDocument2 pagesNogales Vs People of The PhilippinesFai MeileNo ratings yet

- Lo vs. KJSDocument2 pagesLo vs. KJSamareia yapNo ratings yet

- Ma. Gracia Hao and Danny Hao, Petitioners People of The Philippines - RespondentDocument2 pagesMa. Gracia Hao and Danny Hao, Petitioners People of The Philippines - RespondentEffy SantosNo ratings yet

- People vs. BeranDocument1 pagePeople vs. BeranJohn Dexter FuentesNo ratings yet

- ABEL v. RULEG.R. No. 234457, 12 May, 2021Document1 pageABEL v. RULEG.R. No. 234457, 12 May, 2021Marlon EspinaNo ratings yet

- Poe vs. ComelecDocument1 pagePoe vs. ComelecRUBY JAN CASASNo ratings yet

- PERSONS Case Digests (Unciano Paramedical College & Madrigal Wan Hai Lines Cases)Document5 pagesPERSONS Case Digests (Unciano Paramedical College & Madrigal Wan Hai Lines Cases)Robinson MojicaNo ratings yet

- MASTURA vs. COMELECDocument1 pageMASTURA vs. COMELECGale Charm SeñerezNo ratings yet

- G.R. No. 156052 Sjs vs. AtienzaDocument3 pagesG.R. No. 156052 Sjs vs. AtienzaRubz JeanNo ratings yet

- Mangonon vs. CADocument11 pagesMangonon vs. CAChristianneDominiqueGravosoNo ratings yet

- MARY LOU GETURBOS TORRES - Versus - CORAZON ALMA G. DE LEON G.R. No. 199440Document2 pagesMARY LOU GETURBOS TORRES - Versus - CORAZON ALMA G. DE LEON G.R. No. 199440LawiswisNo ratings yet

- Concurring Opinions of Supreme Court JusticesDocument306 pagesConcurring Opinions of Supreme Court JusticesGMA News OnlineNo ratings yet

- Single Borrower's Limit RevDocument2 pagesSingle Borrower's Limit RevJoey SulteNo ratings yet

- Affidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This 3Document1 pageAffidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This 3Aidalyn MendozaNo ratings yet

- Lanto V Coa DigestDocument3 pagesLanto V Coa DigestRaya Alvarez TestonNo ratings yet

- 006 COSCOLLUELA Re in The Matter of Clarification of ExemptionDocument2 pages006 COSCOLLUELA Re in The Matter of Clarification of ExemptionKatrina CoscolluelaNo ratings yet

- Saludo vs. AMEX DigestDocument2 pagesSaludo vs. AMEX DigestPMVNo ratings yet

- Trial Memorandum BuenoDocument3 pagesTrial Memorandum BuenoEfie LumanlanNo ratings yet

- Constitutionalism & MimicryDocument4 pagesConstitutionalism & MimicryAmirah PeñalberNo ratings yet

- 469 Scra 397 Ppa Vs CoaDocument8 pages469 Scra 397 Ppa Vs CoaPanda CatNo ratings yet

- Construction of Election Laws: G.R. No. 78302 Grand Alliance of Democray Vs Comelec WALADocument60 pagesConstruction of Election Laws: G.R. No. 78302 Grand Alliance of Democray Vs Comelec WALANicole Ann Delos ReyesNo ratings yet

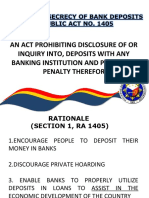

- The Law On Secrecy of Bank DepositsDocument17 pagesThe Law On Secrecy of Bank DepositsMakoy BixenmanNo ratings yet

- 123 Charles Lee, Et Al Vs CA Phil Bank of Communications, GR 117913, Feb 1, 2002Document2 pages123 Charles Lee, Et Al Vs CA Phil Bank of Communications, GR 117913, Feb 1, 2002Alan GultiaNo ratings yet

- Citystate Savings Bank Vs Tobias GR No. 227990, March 7, 2018-Unathorized Bank Transactions in Behalf of OthersDocument9 pagesCitystate Savings Bank Vs Tobias GR No. 227990, March 7, 2018-Unathorized Bank Transactions in Behalf of OthersDuko Alcala EnjambreNo ratings yet

- 6 City State Savings Vs TobiasDocument8 pages6 City State Savings Vs TobiasMary Fatima BerongoyNo ratings yet

- G.R. No. 227990Document12 pagesG.R. No. 227990Chito TolentinoNo ratings yet

- General Banking Act 2000 (HGFF) 2Document13 pagesGeneral Banking Act 2000 (HGFF) 2Marcus-Ruchelle MacadangdangNo ratings yet

- Legform GPA and SPADocument4 pagesLegform GPA and SPAAiko DalaganNo ratings yet

- Raintree ComplaintDocument18 pagesRaintree Complaintmsdyer923No ratings yet

- Contracts: Essential RequisitesDocument120 pagesContracts: Essential RequisitesJong PerrarenNo ratings yet

- MicrofinanceDocument9 pagesMicrofinancesmartwebs100% (1)

- TariffDocument10 pagesTariffDeepshikhaDixitNo ratings yet

- Sample Resolution For A Construction or A ProjectDocument3 pagesSample Resolution For A Construction or A Projectleonida p. barnobalNo ratings yet

- Sale DeedDocument5 pagesSale Deedpintu ramNo ratings yet

- How Much Money Does Your New Venture NeedDocument10 pagesHow Much Money Does Your New Venture NeedFabiana Elena AparicioNo ratings yet

- Rosoft Office PowerPoint PresentationDocument13 pagesRosoft Office PowerPoint PresentationNancy VermaNo ratings yet

- Book 4: Obligations & Contracts Title XI. - LOAN Chapter 1 CommodatumDocument3 pagesBook 4: Obligations & Contracts Title XI. - LOAN Chapter 1 CommodatumJana marieNo ratings yet

- Roles Responsibilities Matrix - LMS Application NewDocument18 pagesRoles Responsibilities Matrix - LMS Application NewunnikallikattuNo ratings yet

- Netmagic Solutions Private Limited: Memorandum of Association OFDocument19 pagesNetmagic Solutions Private Limited: Memorandum of Association OFbapun2007No ratings yet

- Banker Customer RelationshipDocument12 pagesBanker Customer RelationshipPallavi SharmaNo ratings yet

- Viney Testbank With AnswersDocument186 pagesViney Testbank With Answersasyunmwewert83% (12)

- Building and Construction Industry Security of Payment Act 1999 No 46Document31 pagesBuilding and Construction Industry Security of Payment Act 1999 No 46Jason ShermanNo ratings yet

- Lighthouse Point News July IssueDocument76 pagesLighthouse Point News July IssueJon FrangipaneNo ratings yet

- Dignos V CA GR No L-59266 Feb 29 198Document7 pagesDignos V CA GR No L-59266 Feb 29 198Bonito BulanNo ratings yet

- 85 Panlilio v. Citibank PDFDocument16 pages85 Panlilio v. Citibank PDFNeil ChuaNo ratings yet

- REAL ESTATE FINANCE FINAL (No PW)Document11 pagesREAL ESTATE FINANCE FINAL (No PW)PriscillaNo ratings yet

- Sample LoanDocument1 pageSample Loannikhil3831No ratings yet

- ADSF Bankruptcy FilingDocument207 pagesADSF Bankruptcy FilingHannah ColtonNo ratings yet

- Reliance Industries: 2 QTR Results UpdateDocument9 pagesReliance Industries: 2 QTR Results UpdatesonujangirNo ratings yet

- Notice of Filing Cert of Service - Complaint Generic SampleDocument3 pagesNotice of Filing Cert of Service - Complaint Generic Sampleguyte123No ratings yet

- Power Distribution: Comparative Study of Capital Structure Adani PowerDocument3 pagesPower Distribution: Comparative Study of Capital Structure Adani PowerVrushabh ShelkarNo ratings yet