You might also like

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- Coursebook Answers: Answers To Test Yourself QuestionsDocument6 pagesCoursebook Answers: Answers To Test Yourself QuestionsDonatien Oulaii73% (11)

- Reconciliation StatementsDocument26 pagesReconciliation StatementsPetrinaNo ratings yet

- Accountacy For Lawyers Assignement 1Document7 pagesAccountacy For Lawyers Assignement 1Leticia HipangelwaNo ratings yet

- Cash and Cash EquivalentsDocument20 pagesCash and Cash EquivalentsPetrina100% (1)

- June Grade 10 Marking Guideline PDFDocument7 pagesJune Grade 10 Marking Guideline PDFBasetsana MakuaNo ratings yet

- Grade 8 EMS Excercise MemoDocument13 pagesGrade 8 EMS Excercise MemoElon RuskNo ratings yet

- Bank Reconciliation Statements ExplainedDocument5 pagesBank Reconciliation Statements ExplainedAdil Khan LodhiNo ratings yet

- GR 10 Accounting P2 (English) November 2022 Question PaperDocument10 pagesGR 10 Accounting P2 (English) November 2022 Question PaperspbdinkebogileNo ratings yet

- Types of Cash Books Single - Column Cash Book Two Column Cash Book Three Column Cash Book Past KCSE Questions On The TopicDocument10 pagesTypes of Cash Books Single - Column Cash Book Two Column Cash Book Three Column Cash Book Past KCSE Questions On The TopicHENRY MURIGINo ratings yet

- Assignment 3 Apple BlossomDocument21 pagesAssignment 3 Apple BlossomMonica NainggolanNo ratings yet

- Pilate Limited Income StatementDocument13 pagesPilate Limited Income Statementouo So方No ratings yet

- Cash Book GiveDocument19 pagesCash Book GiveZainullah KhanNo ratings yet

- The Cash Book Grade 11 Business Prepare By: Ms PercivalDocument6 pagesThe Cash Book Grade 11 Business Prepare By: Ms PercivalDenishNo ratings yet

- Gyuhyeon JeongDocument4 pagesGyuhyeon JeongITNo ratings yet

- MYUNGSOO YOO StatementDocument4 pagesMYUNGSOO YOO StatementIT100% (1)

- May 2018 and 2017 SolutionsDocument43 pagesMay 2018 and 2017 SolutionsgNo ratings yet

- Bank ReconcilliationDocument22 pagesBank ReconcilliationAli BhattiNo ratings yet

- INDIVIDUAL ASSIGNMENT KEY FINANCIAL STATEMENTSDocument6 pagesINDIVIDUAL ASSIGNMENT KEY FINANCIAL STATEMENTSshiloh chipendoNo ratings yet

- CSEC Principles of Accounts SEC. 3-Balancing The BooksDocument18 pagesCSEC Principles of Accounts SEC. 3-Balancing The BooksEphraim PryceNo ratings yet

- David W WilfongDocument4 pagesDavid W WilfongMark WilliamsNo ratings yet

- Cash BookDocument55 pagesCash Bookshrestha.aryxnNo ratings yet

- Sudsidiary Ledger and Control AccountsDocument20 pagesSudsidiary Ledger and Control AccountsPetrinaNo ratings yet

- Tutorial Set FourDocument6 pagesTutorial Set FourNathaniel MensahNo ratings yet

- Chapter 7 Class ExerciseDocument23 pagesChapter 7 Class ExerciseTiffany ChanceNo ratings yet

- 11 Acc Task 5.5 5.8 5.9 5.12 5.16 Memos 2023 GoodDocument10 pages11 Acc Task 5.5 5.8 5.9 5.12 5.16 Memos 2023 Goodora mashaNo ratings yet

- Ledger accounts and trial balanceDocument42 pagesLedger accounts and trial balanceAmruthaprashanth100% (1)

- Financial Accounting Assisgnment 1.2021Document9 pagesFinancial Accounting Assisgnment 1.2021Mudada Trevor IINo ratings yet

- CCP102Document16 pagesCCP102api-3849444No ratings yet

- CCP102Document15 pagesCCP102api-3849444No ratings yet

- Bank of America StatementDocument12 pagesBank of America StatementAmin Sahil0% (1)

- Case Study Acct MGT - ACCT 102 - FinalDocument5 pagesCase Study Acct MGT - ACCT 102 - FinalbrightsparksintlNo ratings yet

- GR 10 Acc T1 Week 2 ENGDocument7 pagesGR 10 Acc T1 Week 2 ENGAmal MohmoudNo ratings yet

- PDF Coursebook Chapter 4 Answers - CompressDocument6 pagesPDF Coursebook Chapter 4 Answers - CompressSama ZabadyNo ratings yet

- Assignment 1 Principles of AccountingDocument13 pagesAssignment 1 Principles of AccountingMmonie MotseleNo ratings yet

- gr9t2 Ems wk2 7 Topic 1 Financial Literacy MemoDocument18 pagesgr9t2 Ems wk2 7 Topic 1 Financial Literacy MemoLeeora NairNo ratings yet

- EC Accounting Grade 10 November 2022 P2 and MemoDocument28 pagesEC Accounting Grade 10 November 2022 P2 and Memon2yqzmd67fNo ratings yet

- Ryan BoA July 2022Document11 pagesRyan BoA July 2022Yooo100% (3)

- AccountsDocument8 pagesAccountsWilliNo ratings yet

- Nam-Kee LeeDocument4 pagesNam-Kee LeeITNo ratings yet

- Cathay Bank Money Market Account Statement SummaryDocument8 pagesCathay Bank Money Market Account Statement SummaryCiprian IoleaNo ratings yet

- BAStmt - 2022 12 30Document12 pagesBAStmt - 2022 12 30Amin SahilNo ratings yet

- Accounting Workbook Section 4 AnswersDocument49 pagesAccounting Workbook Section 4 Answersalya mahaputriNo ratings yet

- Acc Clerk Chapter 4b-Preparing Trial BalanceDocument15 pagesAcc Clerk Chapter 4b-Preparing Trial BalanceEphraim PryceNo ratings yet

- Bank RecDocument24 pagesBank RecbillNo ratings yet

- Bank reconciliation statement explainedDocument24 pagesBank reconciliation statement explainedJishnuPatilNo ratings yet

- Tutorial 1week 11Document2 pagesTutorial 1week 11Lawrence Mirie MudakuvakaNo ratings yet

- 03 Books of Original Entry and Ledgers (I)Document16 pages03 Books of Original Entry and Ledgers (I)YU TaktakNo ratings yet

- Estmt - 2022 09 07Document4 pagesEstmt - 2022 09 07Pablo Gomez100% (1)

- Worksheet8.1Document3 pagesWorksheet8.1RealGenius (Carl)No ratings yet

- 9 Ems Acc Revision Test Term 2 2022 GoDocument6 pages9 Ems Acc Revision Test Term 2 2022 GoEstelle EsterhuizenNo ratings yet

- AFE3582 AFE3582 Lesson 5. Bank Reconciliation StatementDocument8 pagesAFE3582 AFE3582 Lesson 5. Bank Reconciliation StatementelfigossNo ratings yet

- Janthakan SuksompuechDocument4 pagesJanthakan SuksompuechIT100% (2)

- Kate Corp Periodical Exam AnalysisDocument10 pagesKate Corp Periodical Exam AnalysisCharlesNo ratings yet

- Bank Reconciliation Statement - Docx QueDocument5 pagesBank Reconciliation Statement - Docx QueannahkaupaNo ratings yet

- Estmt - 2023 03 21Document4 pagesEstmt - 2023 03 21Heriberto Rios RealtorNo ratings yet

- Data Entries in AccountingDocument13 pagesData Entries in AccountingMai SalehNo ratings yet

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaFrom EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaNo ratings yet

- Endocrine SystemnewDocument22 pagesEndocrine SystemnewFlor AidaNo ratings yet

- Work Energy and PowerDocument5 pagesWork Energy and PowerJoRaccoonaNo ratings yet

- SOUTH POEM ANALYSIS by Kamau BrathwaiteDocument33 pagesSOUTH POEM ANALYSIS by Kamau BrathwaiteJoRaccoonaNo ratings yet

- Ol'Higue Poem-NotesDocument4 pagesOl'Higue Poem-NotesJoRaccoonaNo ratings yet

- Tutorial 1.1Document23 pagesTutorial 1.1Xiuqin LiNo ratings yet

- Islamic FinanceDocument15 pagesIslamic FinanceHassaan ButtNo ratings yet

- Foreign Trade Policy 2004-09Document25 pagesForeign Trade Policy 2004-09Nishant RaoNo ratings yet

- Etextbook 978 0132773706 Economics For ManagersDocument61 pagesEtextbook 978 0132773706 Economics For Managerslee.ortiz429100% (51)

- L'Oréal in Vietnam - Optimizing the Cosmetics Supply ChainDocument11 pagesL'Oréal in Vietnam - Optimizing the Cosmetics Supply ChainRain HaruNo ratings yet

- Anexo 2. T2 - David RicardoDocument5 pagesAnexo 2. T2 - David Ricardoingrith vanesa delgado guangaNo ratings yet

- Place of Supply Under IGSTDocument4 pagesPlace of Supply Under IGSTSUNNY GUPTANo ratings yet

- 2022 Sem 1 ACC10007 Practice MCQs - Topic 3Document7 pages2022 Sem 1 ACC10007 Practice MCQs - Topic 3JordanNo ratings yet

- InvoiceDocument1 pageInvoicemohammad touffiqueNo ratings yet

- E Canna Buy Online Shopping Site - E Canna CoinsDocument2 pagesE Canna Buy Online Shopping Site - E Canna CoinsE Canna BuyNo ratings yet

- Op Transaction HistoryDocument2 pagesOp Transaction HistorySappy SoniNo ratings yet

- Bill of Lading - Funciones Descripcion y LlenadoDocument21 pagesBill of Lading - Funciones Descripcion y LlenadoLuciano ReboraNo ratings yet

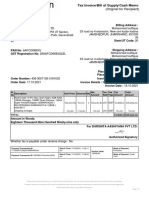

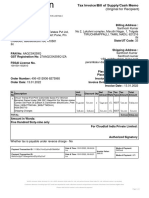

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)kishanprasadNo ratings yet

- RBL Credit Card Statement - UnlockedDocument2 pagesRBL Credit Card Statement - UnlockedDipra DasNo ratings yet

- Tax Invoice for Saree PurchaseDocument1 pageTax Invoice for Saree PurchaseSanthosh Hero SantoNo ratings yet

- Cardoso, Fishlow 1992Document23 pagesCardoso, Fishlow 1992L Laura Bernal HernándezNo ratings yet

- Review of COGS and CGMDocument4 pagesReview of COGS and CGMChloe Ann CabayloNo ratings yet

- Assignment 1 M.Rabi Ijaz 10678Document23 pagesAssignment 1 M.Rabi Ijaz 10678Rabi IjazNo ratings yet

- RBI and Its Control Over BanksDocument10 pagesRBI and Its Control Over BanksHarshad PatilNo ratings yet

- Corporate ValuationDocument16 pagesCorporate Valuationvinit warangNo ratings yet

- INCOTERMS 2020 Rules Short - TFG - SummaryDocument20 pagesINCOTERMS 2020 Rules Short - TFG - SummaryPaulina GraciannaNo ratings yet

- PORTFOLIODocument7 pagesPORTFOLIOismail abidNo ratings yet

- MITI Report 2018 PDFDocument162 pagesMITI Report 2018 PDFTuan Pauzi Tuan IsmailNo ratings yet

- Inflation: Prices On The RiseDocument1 pageInflation: Prices On The RiseMicheleFontanaNo ratings yet

- 1.factors Influencing Foreign Direct Investment in Lesser Developed CountriesDocument9 pages1.factors Influencing Foreign Direct Investment in Lesser Developed CountriesAzan RasheedNo ratings yet

- Mishkin Econ13e PPT 17Document25 pagesMishkin Econ13e PPT 17Huyền Nhi QuảnNo ratings yet

- Fundamentals of Capital Budgeting: Learning Packet 1Document17 pagesFundamentals of Capital Budgeting: Learning Packet 1jenniferNo ratings yet

- Farm Bills 2020 Economics ProjectDocument11 pagesFarm Bills 2020 Economics ProjectDhanshri ThakreNo ratings yet

- Wells Fargo StatementDocument8 pagesWells Fargo StatementJohn Bean100% (3)

- Chapter 2 - International ShippingDocument54 pagesChapter 2 - International ShippingLâm Tố NhưNo ratings yet