You might also like

- Costing PractiseDocument8 pagesCosting PractiseMovie MasterNo ratings yet

- Departmentalization Problem Key UeDocument2 pagesDepartmentalization Problem Key Ueedrianclyde100% (1)

- New Microsoft Office Excel WorksheetDocument73 pagesNew Microsoft Office Excel WorksheetLaxmisha GowdaNo ratings yet

- CrionDocument6 pagesCrionPreticia ChristianNo ratings yet

- Day 4 - Class ExerciseDocument10 pagesDay 4 - Class Exerciseum23328No ratings yet

- Infrastructure Qty Cost AmountDocument7 pagesInfrastructure Qty Cost AmountSanjeev MiglaniNo ratings yet

- KL-ABC CostingDocument6 pagesKL-ABC CostingDebarpan HaldarNo ratings yet

- Cost & Management Accounting - MGT402 Power Point Slides Lecture 15Document22 pagesCost & Management Accounting - MGT402 Power Point Slides Lecture 15Mr. JalilNo ratings yet

- Day 4Document8 pagesDay 4um23328No ratings yet

- Tuto 11Document3 pagesTuto 11WEI QUAN LEENo ratings yet

- Management Acc. Assign.2 KashifDocument2 pagesManagement Acc. Assign.2 Kashifusman faisalNo ratings yet

- Overhead ApportionmentDocument3 pagesOverhead ApportionmentHassanAbsarQaimkhaniNo ratings yet

- 5 - ABC (Solution)Document32 pages5 - ABC (Solution)Mubashir HasanNo ratings yet

- Acccob3 HW9Document33 pagesAcccob3 HW9Reshawn Kimi SantosNo ratings yet

- Shashaank Industries LTD - Session 3Document6 pagesShashaank Industries LTD - Session 3Srijan SaxenaNo ratings yet

- Activity Activity Cost Pool Cost Driver Cost Driver Quality Pool RateDocument8 pagesActivity Activity Cost Pool Cost Driver Cost Driver Quality Pool RateAman ShahNo ratings yet

- Particulars Units Unit Cost (RS) Total Cost (RS)Document3 pagesParticulars Units Unit Cost (RS) Total Cost (RS)ginish12No ratings yet

- Example Overheards Allocation 1Document4 pagesExample Overheards Allocation 1Phomolo StoffelNo ratings yet

- ExpensesDocument3 pagesExpensesJezerie Kaye T. FerrerNo ratings yet

- Correction Cas SocaDocument23 pagesCorrection Cas Socabayern100% (1)

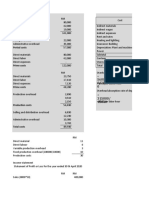

- Tumble Dry Project Financial ReportDocument3 pagesTumble Dry Project Financial ReportAkash SanganiNo ratings yet

- Overhead Analysis Solution 1Document2 pagesOverhead Analysis Solution 1Humphrey OsaigbeNo ratings yet

- 2004 DecemberDocument6 pages2004 DecemberSherif AwadNo ratings yet

- 15-Pivot TableDocument5 pages15-Pivot TableAshutosh VermaNo ratings yet

- Homework For ABCDocument6 pagesHomework For ABCLikey CruzNo ratings yet

- Bus ModDocument2 pagesBus ModdmadhavanurNo ratings yet

- Costco2-Quiz End-TermDocument4 pagesCostco2-Quiz End-TermmhikeedelantarNo ratings yet

- Câu 1 - Case Study 8.47 - 18.5.2020Document15 pagesCâu 1 - Case Study 8.47 - 18.5.2020Nguyen SaoNo ratings yet

- TYBCOM - Cost - OverheadsDocument8 pagesTYBCOM - Cost - Overheadsmkbooks4uNo ratings yet

- s15 16 (AutoRecovered)Document14 pagess15 16 (AutoRecovered)R GNo ratings yet

- Mechanical Drying Equipment FinalDocument8 pagesMechanical Drying Equipment Finalvijaypal2000100% (1)

- Installment MethodDocument4 pagesInstallment Methodjessica amorosoNo ratings yet

- Cost AccountingDocument24 pagesCost AccountingJalo NacionNo ratings yet

- Sales Budgeting (Dec 16)Document5 pagesSales Budgeting (Dec 16)Jaganath Reddy GFkKwVvllyNo ratings yet

- CF7 PDFDocument3 pagesCF7 PDFSanilyn DomingoNo ratings yet

- Ans. 677 Corp AcctDocument12 pagesAns. 677 Corp AcctHashimRazaNo ratings yet

- Alano Julius N. TM 205 - Financial and Cost Analysis For Technology Managers 2018-20700 S (9:00AM-12:00PM)Document1 pageAlano Julius N. TM 205 - Financial and Cost Analysis For Technology Managers 2018-20700 S (9:00AM-12:00PM)Julius AlanoNo ratings yet

- Exam Gestion Financier Ratt 2018 Prof MESK - Faculté HASSAN 2 CASABLANCADocument1 pageExam Gestion Financier Ratt 2018 Prof MESK - Faculté HASSAN 2 CASABLANCAAbdoNo ratings yet

- Module 2 - Laboratory Exercise 1Document10 pagesModule 2 - Laboratory Exercise 1Joana TrinidadNo ratings yet

- Quesada CleanersDocument3 pagesQuesada CleanersAngel EstradaNo ratings yet

- MGT 115 Removal Exam 1S AY 2017 2018 25 Sept 2018Document6 pagesMGT 115 Removal Exam 1S AY 2017 2018 25 Sept 2018Kadita MageNo ratings yet

- Midterms MADocument10 pagesMidterms MAJustz LimNo ratings yet

- Pearl River Valley Flood Control District 2022 BudgetDocument1 pagePearl River Valley Flood Control District 2022 BudgetAnthony WarrenNo ratings yet

- CashflowDocument5 pagesCashflowHanan SalmanNo ratings yet

- Start-Up Capital:: Particulars Taka TakaDocument5 pagesStart-Up Capital:: Particulars Taka TakaSahriar EmonNo ratings yet

- Management Accounting: Wilkerson Company Case Group 5Document5 pagesManagement Accounting: Wilkerson Company Case Group 5YATIN BAJAJNo ratings yet

- Items Cost Cost ( N ) : Cleaners Food Technicians Security Guards Other Total Salary Labor Salary in NairaDocument4 pagesItems Cost Cost ( N ) : Cleaners Food Technicians Security Guards Other Total Salary Labor Salary in NairababatundeNo ratings yet

- Essay FIN202Document5 pagesEssay FIN202thaindnds180468No ratings yet

- Monthely BudgetDocument4 pagesMonthely Budgetم سليمانNo ratings yet

- Traditional Approaches To Full Costing Answers To End of Chapter ExercisesDocument4 pagesTraditional Approaches To Full Costing Answers To End of Chapter ExercisesJay BrockNo ratings yet

- Cohas Budget 2022 - Final FinalDocument19 pagesCohas Budget 2022 - Final FinalThomasNo ratings yet

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- Managerial AccountingDocument8 pagesManagerial AccountingjaneperdzNo ratings yet

- Monthly Business BudgetDocument4 pagesMonthly Business BudgetOkasha HafeezNo ratings yet

- Accounts Case LetDocument7 pagesAccounts Case Letriya lakhotiaNo ratings yet

- Sarvajal - Estados Financieros 211028-PDF-ENG-19Document1 pageSarvajal - Estados Financieros 211028-PDF-ENG-19Santiago et AlejandraNo ratings yet

- Wilkerson CompanyDocument9 pagesWilkerson CompanyPrabhav GuptaNo ratings yet

- AccountingDocument16 pagesAccountingSheridan AcosmistNo ratings yet

- Case SolutionsDocument11 pagesCase SolutionsMohit AgrawalNo ratings yet

- Audel Guide to the 2005 National Electrical CodeFrom EverandAudel Guide to the 2005 National Electrical CodeRating: 4 out of 5 stars4/5 (1)

- Nishi Sir's Accounts-NotesDocument34 pagesNishi Sir's Accounts-Notesapi-375803189% (9)

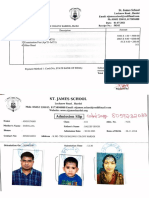

- Admission ST James Naman& AnshuDocument7 pagesAdmission ST James Naman& AnshuDaleep SinghNo ratings yet

- Cost Acctg MC Questions PDFDocument40 pagesCost Acctg MC Questions PDFBromanineNo ratings yet

- CHAPTER 10 Cost Analysis For Decision MakingDocument32 pagesCHAPTER 10 Cost Analysis For Decision MakingJellai JollyNo ratings yet

- Unit 7 Audit of Property Plant and Equipment Handout Final t21516Document10 pagesUnit 7 Audit of Property Plant and Equipment Handout Final t21516Mikaella BengcoNo ratings yet

- T1 - Bbfa4014 CrciDocument23 pagesT1 - Bbfa4014 CrciLaw KanasaiNo ratings yet

- DundalkpcDocument26 pagesDundalkpcthestorydotieNo ratings yet

- Class 14 ExampleDocument4 pagesClass 14 Exampledeepanshu guptaNo ratings yet

- 15 Financial AccountsDocument111 pages15 Financial AccountsRenga Pandi100% (1)

- Primary Books of AccountsDocument16 pagesPrimary Books of AccountsSaptha Gowda100% (1)

- 1 Apr 2021 To 5 Jul 2021Document32 pages1 Apr 2021 To 5 Jul 2021DIPAK VINAYAK SHIRBHATENo ratings yet

- Case Study 4Document4 pagesCase Study 4RoseanneNo ratings yet

- SBMF Examinations June 2010Document50 pagesSBMF Examinations June 2010van Dana kam'sNo ratings yet

- Internal Audit in Practice Case StudiesDocument32 pagesInternal Audit in Practice Case StudiesJo Bats67% (3)

- Fabm 1 Lesson 4-5Document32 pagesFabm 1 Lesson 4-5Dionel RizoNo ratings yet

- MAS Diagnostic ExamDocument10 pagesMAS Diagnostic ExamDanielNo ratings yet

- BDO Knows ASC 740 Intra Entity Transfers of Assets Other Than Inventory - FINAL PDFDocument9 pagesBDO Knows ASC 740 Intra Entity Transfers of Assets Other Than Inventory - FINAL PDFUlii PntNo ratings yet

- Case 01a Growing Pains SolutionDocument7 pagesCase 01a Growing Pains SolutionUSD 654No ratings yet

- Jad Payroll April 01-07 2022Document9 pagesJad Payroll April 01-07 2022Jervie JalaNo ratings yet

- Intermediate Accounting 3 - January 24, 2023, F2F DiscussionDocument8 pagesIntermediate Accounting 3 - January 24, 2023, F2F DiscussionZhaira Kim CantosNo ratings yet

- Acca Ethics and Professionalism.Document22 pagesAcca Ethics and Professionalism.abirking50% (2)

- Cash Flow in Capital Budgeting KeownDocument37 pagesCash Flow in Capital Budgeting Keownmad2kNo ratings yet

- Frequently Asked Questions Relating To Comfort Letters and Comfort Letter PracticeDocument12 pagesFrequently Asked Questions Relating To Comfort Letters and Comfort Letter PracticeKennith NgNo ratings yet

- Sabari Inn DRHPDocument283 pagesSabari Inn DRHPArpan Mehta SameerNo ratings yet

- ICAEW - Accounting 2020 - Chap 5Document51 pagesICAEW - Accounting 2020 - Chap 5TRIEN DINH TIENNo ratings yet

- WWF Tanzania Vacancies AugustDocument24 pagesWWF Tanzania Vacancies AugustSaumu MbanoNo ratings yet

- Senarai Kursus Pindahan Kredit Fep 011019Document20 pagesSenarai Kursus Pindahan Kredit Fep 011019CintopanNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- AOM NO. 01-Stale ChecksDocument3 pagesAOM NO. 01-Stale ChecksRagnar Lothbrok100% (2)

- ACC-303 Discussion QuestionsDocument15 pagesACC-303 Discussion QuestionsVivek Surana100% (1)