You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Material Engineer ReviewerDocument64 pagesMaterial Engineer ReviewerEulogio JameroNo ratings yet

- Arens Auditing16e SM 14Document38 pagesArens Auditing16e SM 14김현중No ratings yet

- Arens Auditing16e SM 21Document28 pagesArens Auditing16e SM 21김현중No ratings yet

- Arens Auditing16e SM 22Document20 pagesArens Auditing16e SM 22김현중No ratings yet

- Audit of The Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts PayableDocument33 pagesAudit of The Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable김현중No ratings yet

- Arens Auditing16e SM 26Document15 pagesArens Auditing16e SM 26김현중No ratings yet

- Arens Auditing16e SM 15Document27 pagesArens Auditing16e SM 15김현중No ratings yet

- Ch. 6 - SM ACCDocument20 pagesCh. 6 - SM ACCkrstn_hghtwrNo ratings yet

- Ch. 3 - SM ACCDocument19 pagesCh. 3 - SM ACCkrstn_hghtwr100% (1)

- Arens Auditing16e SM 12Document40 pagesArens Auditing16e SM 12김현중No ratings yet

- Arens Auditing16e SM 10Document30 pagesArens Auditing16e SM 10김현중100% (2)

- Arens Auditing16e SM 13Document21 pagesArens Auditing16e SM 13김현중No ratings yet

- Arens Auditing16e SM 09Document28 pagesArens Auditing16e SM 09김현중No ratings yet

- Ch. 7 - SM ACCDocument26 pagesCh. 7 - SM ACCkrstn_hghtwrNo ratings yet

- Arens Auditing16e SM 11Document20 pagesArens Auditing16e SM 11김현중No ratings yet

- ARM STM32F476 Interrupts PDFDocument38 pagesARM STM32F476 Interrupts PDFLars NymanNo ratings yet

- Transportation Chapter 3Document17 pagesTransportation Chapter 3Tuan NguyenNo ratings yet

- El Proceso Migratorio en El Ecuador Despues de La Crisis Economica-Financiera de 1998-1999Document30 pagesEl Proceso Migratorio en El Ecuador Despues de La Crisis Economica-Financiera de 1998-1999Alex IntriagoNo ratings yet

- Pimentel v. HRET, GR No. 141489Document8 pagesPimentel v. HRET, GR No. 141489Nikki Rose Laraga AgeroNo ratings yet

- Inmuno Linfocitos Cd4 y 8Document22 pagesInmuno Linfocitos Cd4 y 8Marco RamírezNo ratings yet

- Expose DetecteursDocument15 pagesExpose DetecteursPatrice CamaraNo ratings yet

- Mis Historias Urbanas - Por BlankimonkiDocument212 pagesMis Historias Urbanas - Por BlankimonkiAlex Daniel Cabezas EuvinNo ratings yet

- Chap 2 Concept of IhrmDocument7 pagesChap 2 Concept of IhrmjagdishNo ratings yet

- Capacidad EléctricaDocument3 pagesCapacidad Eléctrica01-IC-HU-CRISTIAM RICARDO POMALAZA RODRIGUEZNo ratings yet

- Cuadernillo de Martin Miguel de Güemes MatematicaDocument6 pagesCuadernillo de Martin Miguel de Güemes MatematicaFatima Mariela BepreNo ratings yet

- MaldivasDocument13 pagesMaldivasNaym ElizabethNo ratings yet

- Bem Vindos A Cabana Do VulcãoDocument9 pagesBem Vindos A Cabana Do VulcãoMell VieiraNo ratings yet

- Tesla Coil Instruction DiyDocument7 pagesTesla Coil Instruction Diydmj90464100% (1)

- ICE Guidance Memo - Post Order Custody Reviews Responsibilities and Guidance (9/17/07)Document7 pagesICE Guidance Memo - Post Order Custody Reviews Responsibilities and Guidance (9/17/07)J CoxNo ratings yet

- COLEGIO PARROQUIAL SAN LUIS GONZAGA - Abiertas - 801Document3 pagesCOLEGIO PARROQUIAL SAN LUIS GONZAGA - Abiertas - 801David Santiago LongoNo ratings yet

- Essais MecaniquesDocument10 pagesEssais MecaniqueshamidochNo ratings yet

- (WWW - Entrance-Exam - Net) - Manual of Procedure For Approval of Teachers in AICTE Approved Polytechnics by MSBTEDocument18 pages(WWW - Entrance-Exam - Net) - Manual of Procedure For Approval of Teachers in AICTE Approved Polytechnics by MSBTERajanikant KakadeNo ratings yet

- Measuring Patient ExperienceDocument50 pagesMeasuring Patient ExperienceUmakNo ratings yet

- Se Data Logger Installation Guide NaDocument67 pagesSe Data Logger Installation Guide NaapocalipcNo ratings yet

- Beginning - Middle - EndDocument17 pagesBeginning - Middle - EndGrishma DaghaNo ratings yet

- Onkologia EkzamenDocument171 pagesOnkologia EkzamenМихаил ГрицевецNo ratings yet

- Arbeitsblatt 3 Lösungen: While Watching 00:22-05:50Document3 pagesArbeitsblatt 3 Lösungen: While Watching 00:22-05:50FamilyGangNo ratings yet

- PLUMADocument13 pagesPLUMAismyliveNo ratings yet

- Sindrome de Guillian BarreDocument2 pagesSindrome de Guillian Barreenf.luismatiasNo ratings yet

- UntitledDocument282 pagesUntitledSerge AnthonyNo ratings yet

- Country Project PPT GuidelinesDocument2 pagesCountry Project PPT GuidelinesLaia Moreno FerranNo ratings yet

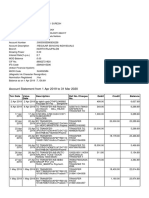

- Account Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancesureshNo ratings yet

- Guía de Adaptación TitanDocument2 pagesGuía de Adaptación TitanOrlando Gonzalez PicadoNo ratings yet