You might also like

- Lecture Notes in Comparative Economic PlanningDocument31 pagesLecture Notes in Comparative Economic PlanningRebekah Grace Abanto90% (10)

- Economic Planning - MA Economics Karachi UniversityDocument12 pagesEconomic Planning - MA Economics Karachi UniversitySharina ObogNo ratings yet

- Project Handout For Masters (Text Book Two)Document177 pagesProject Handout For Masters (Text Book Two)Hamse HusseinNo ratings yet

- Principle of Accounting AssignmentDocument67 pagesPrinciple of Accounting Assignmentአንተነህ የእናቱNo ratings yet

- # Macroeconomics Chapter - 1Document31 pages# Macroeconomics Chapter - 1Getaneh ZewuduNo ratings yet

- Economics Ca2Document13 pagesEconomics Ca2Ayan BeraNo ratings yet

- Sustainable Economic GrowthDocument44 pagesSustainable Economic Growthjatt ManderNo ratings yet

- Economic Policy, Planning and Programming I (Ec311: BAEC-3 & BAED-3 2020/2021Document102 pagesEconomic Policy, Planning and Programming I (Ec311: BAEC-3 & BAED-3 2020/2021Hashim Said100% (1)

- Subject EconomicsDocument10 pagesSubject EconomicsMubashirNo ratings yet

- Applied Economics-Lesson 2Document25 pagesApplied Economics-Lesson 2emmanuel.penetranteNo ratings yet

- Unit 1Document6 pagesUnit 1prateeksharma3358No ratings yet

- Engineering Economic 2020-1Document5 pagesEngineering Economic 2020-1Mr sfeanNo ratings yet

- Book 2Document61 pagesBook 2manofiron20002000No ratings yet

- SHatnenko Methodological Instructions For The Tutorials On Microeconomics 3Document51 pagesSHatnenko Methodological Instructions For The Tutorials On Microeconomics 3pn5hcykvf6No ratings yet

- Abhijeet Audichya 1 Indian EconomyDocument11 pagesAbhijeet Audichya 1 Indian EconomyABHIJEET AUDICHYANo ratings yet

- StabilizationDocument21 pagesStabilizationSherali SoodNo ratings yet

- Monetary and Fiscal Policy: Faridullah HamdardDocument7 pagesMonetary and Fiscal Policy: Faridullah HamdardFaridullahNo ratings yet

- Macro Economics Policies and PracticesDocument82 pagesMacro Economics Policies and Practicesmayur satavNo ratings yet

- Week 3.2Document4 pagesWeek 3.2Frank Nicoleson D. AjoloNo ratings yet

- Monetary Targeting Strategy and Monetary Policy Objectives in Nigerian Economy, 1986 - 2017Document22 pagesMonetary Targeting Strategy and Monetary Policy Objectives in Nigerian Economy, 1986 - 2017Novelty JournalsNo ratings yet

- Assignment Unit 2 - Keynesian VS Classicist ModelsDocument4 pagesAssignment Unit 2 - Keynesian VS Classicist Modelsdugasanuguse1No ratings yet

- Macro-Economics ProjectDocument63 pagesMacro-Economics ProjectarpanmajumderNo ratings yet

- Chapter 1 - Introduction To Economic TheoryDocument12 pagesChapter 1 - Introduction To Economic TheoryMaria Teresa Frando CahandingNo ratings yet

- Evolution of Monetary Policy in India Early PhaseDocument15 pagesEvolution of Monetary Policy in India Early PhaseNitesh kuraheNo ratings yet

- Study Guide For Module No. 1Document5 pagesStudy Guide For Module No. 1Aila Erika EgrosNo ratings yet

- Table of ContentDocument26 pagesTable of ContentRishabh GuptaNo ratings yet

- Mabini Development Policymaking and StateDocument8 pagesMabini Development Policymaking and StatePran piyaNo ratings yet

- Scope and Methods of Economics: I Learning ObjectivesDocument5 pagesScope and Methods of Economics: I Learning ObjectivesMics leonNo ratings yet

- Economics Module 1Document6 pagesEconomics Module 1ManishNo ratings yet

- Assignment 1 Basic MacroeconomicsDocument3 pagesAssignment 1 Basic MacroeconomicsQuienilyn SanchezNo ratings yet

- Cep NoteDocument6 pagesCep Notesorianojayem2No ratings yet

- Economic PlanningDocument141 pagesEconomic PlanningAyaan Ansary50% (2)

- 4.microecomics - MacroeconomicsDocument5 pages4.microecomics - MacroeconomicsSandip GhimireNo ratings yet

- Group 2 Regional Planning StudioDocument19 pagesGroup 2 Regional Planning StudioTerna HonNo ratings yet

- Economics Assingment HiteshDocument20 pagesEconomics Assingment Hiteshhitesh kashyapNo ratings yet

- Economics NotesDocument3 pagesEconomics NotesSushant SatyalNo ratings yet

- MacroDocument34 pagesMacroPratik LawanaNo ratings yet

- Economics Planning (MA in Economics)Document52 pagesEconomics Planning (MA in Economics)Karim Virani0% (1)

- Chand (1977)Document45 pagesChand (1977)Fredy A. CastañedaNo ratings yet

- Lec 9 Macroeconomic Policy DebatesDocument16 pagesLec 9 Macroeconomic Policy DebatesMy NguyễnNo ratings yet

- SSE 107 Macroeconomics SG 1Document6 pagesSSE 107 Macroeconomics SG 1Aila Erika EgrosNo ratings yet

- Eco 6 FDDocument16 pagesEco 6 FD20047 BHAVANDEEP SINGHNo ratings yet

- Financial AdministrationDocument15 pagesFinancial Administrationshivkanth28No ratings yet

- Chapter 1 - Introduction To Economics: Jsalonga 08/22/19Document6 pagesChapter 1 - Introduction To Economics: Jsalonga 08/22/19Xsob LienNo ratings yet

- Mohd Ebad Askari Unit 3 EEDocument4 pagesMohd Ebad Askari Unit 3 EEEyaminNo ratings yet

- The Effectiveness of The Monetary Transmission Channel On Aggregate Demand During The Health PandemicDocument11 pagesThe Effectiveness of The Monetary Transmission Channel On Aggregate Demand During The Health PandemicNurhafsah JulkipliNo ratings yet

- Macroeconomic Analysis in MalaysiaDocument7 pagesMacroeconomic Analysis in MalaysiaCaroline MartinNo ratings yet

- Basic Economics With Taxation and Agrarian ReformDocument4 pagesBasic Economics With Taxation and Agrarian ReformLouie Leron72% (25)

- Applied Economics: Module No. 1: Week 1: First QuarterDocument7 pagesApplied Economics: Module No. 1: Week 1: First QuarterhiNo ratings yet

- U Iii: M P: NIT Onetary OlicyDocument30 pagesU Iii: M P: NIT Onetary OlicyVarunNo ratings yet

- C1 OverviewDocument32 pagesC1 OverviewAnh Ôn KimNo ratings yet

- Economic Policy Represents The Set Of: Lecture 3 The Financial Policy On Macroeconomic Level Slide 1Document12 pagesEconomic Policy Represents The Set Of: Lecture 3 The Financial Policy On Macroeconomic Level Slide 1LuminushNo ratings yet

- Role of Monetary and Fiscal PDFDocument15 pagesRole of Monetary and Fiscal PDFVinay Kumar KumarNo ratings yet

- Science of Wealth Laws Which Govern Wealth Mankind Allocation of Scarce Optimizing or Maximizing ObjectivesDocument6 pagesScience of Wealth Laws Which Govern Wealth Mankind Allocation of Scarce Optimizing or Maximizing ObjectivesJudy Annbel Regalia CañeteNo ratings yet

- Introduction To MacroeconomicsDocument4 pagesIntroduction To MacroeconomicsPeris WanjikuNo ratings yet

- Economic PlanningDocument13 pagesEconomic PlanningQamar Ali100% (2)

- EC366Document114 pagesEC366Claire ManyangaNo ratings yet

- EEA Complete NotesDocument33 pagesEEA Complete NotesTanuja AdabalaNo ratings yet

- Hazardous Forecasts and Crisis Scenario GeneratorFrom EverandHazardous Forecasts and Crisis Scenario GeneratorNo ratings yet

- Cot Observation ToolDocument14 pagesCot Observation ToolArnoldBaladjayNo ratings yet

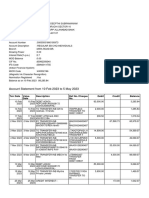

- Feb-May SBI StatementDocument2 pagesFeb-May SBI StatementAshutosh PandeyNo ratings yet

- Regression Week 2: Multiple Linear Regression Assignment 1: If You Are Using Graphlab CreateDocument1 pageRegression Week 2: Multiple Linear Regression Assignment 1: If You Are Using Graphlab CreateSamNo ratings yet

- Application of A HAZOP Study Method To Hazard Evaluation of Chemical Unit of The Power StationDocument8 pagesApplication of A HAZOP Study Method To Hazard Evaluation of Chemical Unit of The Power Stationshinta sariNo ratings yet

- ESA Mars Research Abstracts Part 2Document85 pagesESA Mars Research Abstracts Part 2daver2tarletonNo ratings yet

- English For Law Part 1 Sept 2021Document23 pagesEnglish For Law Part 1 Sept 2021Gina Ayu ApridarisaNo ratings yet

- System of Linear Equation and ApplicationDocument32 pagesSystem of Linear Equation and Applicationihsaanbava0% (1)

- Ugtt April May 2019 NewDocument48 pagesUgtt April May 2019 NewSuhas SNo ratings yet

- Chapter 3 PayrollDocument5 pagesChapter 3 PayrollPheng Tiosen100% (2)

- List of Institutions With Ladderized Program Under Eo 358 JULY 2006 - DECEMBER 31, 2007Document216 pagesList of Institutions With Ladderized Program Under Eo 358 JULY 2006 - DECEMBER 31, 2007Jen CalaquiNo ratings yet

- AAPG 2012 ICE Technical Program & Registration AnnouncementDocument64 pagesAAPG 2012 ICE Technical Program & Registration AnnouncementAAPG_EventsNo ratings yet

- End Points SubrogadosDocument3 pagesEnd Points SubrogadosAgustina AndradeNo ratings yet

- 103-Article Text-514-1-10-20190329Document11 pages103-Article Text-514-1-10-20190329Elok KurniaNo ratings yet

- Introduction To Templates in C++Document16 pagesIntroduction To Templates in C++hammarbytpNo ratings yet

- 1.3.3 1.3.4 1.3.5 Input, Output & Storage Devices Workbook by Inqilab Patel PDFDocument173 pages1.3.3 1.3.4 1.3.5 Input, Output & Storage Devices Workbook by Inqilab Patel PDFRayyan MalikNo ratings yet

- PST SubjectDocument2 pagesPST SubjectCarol ElizagaNo ratings yet

- Technical Textile and SustainabilityDocument5 pagesTechnical Textile and SustainabilityNaimul HasanNo ratings yet

- Development of PBAT Based Bio Filler Masterbatch: A Scientific Research Proposal OnDocument15 pagesDevelopment of PBAT Based Bio Filler Masterbatch: A Scientific Research Proposal OnManmathNo ratings yet

- Model Personal StatementDocument2 pagesModel Personal StatementSwayam Tripathy100% (1)

- TMA GuideDocument3 pagesTMA GuideHamshavathini YohoratnamNo ratings yet

- Study On The Form Factor and Full-Scale Ship Resistance Prediction MethodDocument2 pagesStudy On The Form Factor and Full-Scale Ship Resistance Prediction MethodRaka AdityaNo ratings yet

- Smart Cockpit System Questions - FlattenedDocument85 pagesSmart Cockpit System Questions - FlattenedBarut Brkk100% (4)

- NST 029Document123 pagesNST 029Riaz Ahmad BhattiNo ratings yet

- SQL TestDocument10 pagesSQL TestGautam KatlaNo ratings yet

- INA Over Drive Pulley SystemDocument1 pageINA Over Drive Pulley SystemDaniel JulianNo ratings yet

- Auditing Multiple Choice Questions and Answers MCQs Auditing MCQ For CA, CS and CMA Exams Principle of Auditing MCQsDocument30 pagesAuditing Multiple Choice Questions and Answers MCQs Auditing MCQ For CA, CS and CMA Exams Principle of Auditing MCQsmirjapur0% (1)

- Muhammad Firdaus - A Review of Personal Data Protection Law in IndonesiaDocument7 pagesMuhammad Firdaus - A Review of Personal Data Protection Law in IndonesiaJordan Amadeus SoetowidjojoNo ratings yet

- Role of Micro-Financing in Women Empowerment: An Empirical Study of Urban PunjabDocument16 pagesRole of Micro-Financing in Women Empowerment: An Empirical Study of Urban PunjabAnum ZubairNo ratings yet

- 1207 - RTC-8065 II InglesDocument224 pages1207 - RTC-8065 II InglesGUILHERME SANTOSNo ratings yet

- General Introduction: 1.1 What Is Manufacturing (MFG) ?Document19 pagesGeneral Introduction: 1.1 What Is Manufacturing (MFG) ?Mohammed AbushammalaNo ratings yet