You might also like

- Assignment Module 3 LedgerDocument3 pagesAssignment Module 3 LedgerPRINCE100% (1)

- Assignment: Unit Vi: Trial BalanceDocument3 pagesAssignment: Unit Vi: Trial BalanceGautami Patil100% (1)

- Scotia and TD TransactionsDocument12 pagesScotia and TD TransactionsaspiringstudentNo ratings yet

- Department of Business Administration Group Assignment On Fundamental of Accounting IDocument5 pagesDepartment of Business Administration Group Assignment On Fundamental of Accounting IMohammed HassenNo ratings yet

- Joining Ajman Free Zone New ProcedureDocument6 pagesJoining Ajman Free Zone New ProcedureclauraNo ratings yet

- PNB Process NoteDocument36 pagesPNB Process NotePawan BagrechaNo ratings yet

- Class Work Journal EntryDocument16 pagesClass Work Journal EntryRishabh ChawlaNo ratings yet

- Hyzer Disc Golf Course Was Opened On March 1 by PDFDocument1 pageHyzer Disc Golf Course Was Opened On March 1 by PDFAnbu jaromiaNo ratings yet

- Golden Lamian Franchise 1.1Document28 pagesGolden Lamian Franchise 1.1Adrian KurniaNo ratings yet

- Sample Air Asia BookingDocument3 pagesSample Air Asia BookingMa-an MaromaNo ratings yet

- LSGD Section Karakurissi Karakkurissi GP-2020-21-Veluthedathu Padam Road Concrete - (Proj - No.62/20-21)Document2 pagesLSGD Section Karakurissi Karakkurissi GP-2020-21-Veluthedathu Padam Road Concrete - (Proj - No.62/20-21)AE Karakurissy100% (1)

- Exercise (Final Accounts)Document14 pagesExercise (Final Accounts)Abhishek BansalNo ratings yet

- Tanzania Single Administrative Document: Component No Item Invoice Price Unit Price 48.model, Specification QuantityDocument1 pageTanzania Single Administrative Document: Component No Item Invoice Price Unit Price 48.model, Specification QuantityHonest consolidationNo ratings yet

- عقد بيع ابتدائيDocument2 pagesعقد بيع ابتدائيbaghloul ahmedNo ratings yet

- AssigmentDocument8 pagesAssigmentMuhammad Rafique0% (1)

- Hotel AccountingDocument8 pagesHotel AccountinglindakuttyNo ratings yet

- Hotel Inderlok Classic: Net Payable Amount 27983Document10 pagesHotel Inderlok Classic: Net Payable Amount 27983Mohit TyagiNo ratings yet

- Accrual and ProvisionDocument66 pagesAccrual and ProvisionVeronica Bailey100% (1)

- 6int 2011 Jun ADocument7 pages6int 2011 Jun AMuhmmad FahadNo ratings yet

- Unit 3 - LedgerDocument18 pagesUnit 3 - LedgerKanak RathoreNo ratings yet

- JournalDocument5 pagesJournalGanapathi VNo ratings yet

- Additional Illustrations-13Document9 pagesAdditional Illustrations-13Gulneer LambaNo ratings yet

- CCP102Document26 pagesCCP102api-3849444No ratings yet

- CCP102Document37 pagesCCP102api-3849444No ratings yet

- Lecture 2 Part 2 - Emily - SolutionDocument8 pagesLecture 2 Part 2 - Emily - SolutionIsyraf Hatim Mohd TamizamNo ratings yet

- Lesson-5 LedgerDocument16 pagesLesson-5 LedgernishaashaxxNo ratings yet

- Assets Increases Decreases Liabilities Decreases Increases Income Decreases Increases Expenses Increases DecreasesDocument9 pagesAssets Increases Decreases Liabilities Decreases Increases Income Decreases Increases Expenses Increases DecreasesprashantsdpikiNo ratings yet

- CCP102Document39 pagesCCP102api-3849444No ratings yet

- Concepts of FinanceDocument1 pageConcepts of FinanceNISHANTH P CHOYAL 2228512No ratings yet

- Branch AccountsDocument9 pagesBranch AccountsKalpana SinghNo ratings yet

- Preparation of Ledger Accounts & Trial Balance - 1Document24 pagesPreparation of Ledger Accounts & Trial Balance - 1sneha sasidharanNo ratings yet

- Lahore Garrison University: Assignment # 4Document6 pagesLahore Garrison University: Assignment # 4Muhammad huzaifaNo ratings yet

- Ledger: HAT IS EdgerDocument5 pagesLedger: HAT IS EdgerTara GilaniNo ratings yet

- Preparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFDocument30 pagesPreparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFzaya sarwarNo ratings yet

- Abdulla YounisDocument4 pagesAbdulla Younisashwani singhaniaNo ratings yet

- Assignment 5Document2 pagesAssignment 5Phuong DungNo ratings yet

- In The Books of Anshal LTD Date Particulars JournalDocument10 pagesIn The Books of Anshal LTD Date Particulars JournalANISH DUA IPM 2019-24 BatchNo ratings yet

- Accounting EntriesDocument6 pagesAccounting EntriesIndu GuptaNo ratings yet

- T Accounts and TB by Riffat JabeenDocument4 pagesT Accounts and TB by Riffat JabeenAbie AsifNo ratings yet

- LEDGERDocument10 pagesLEDGERKul DeepNo ratings yet

- Ledger AccountDocument14 pagesLedger AccountAnnpourna ShuklaNo ratings yet

- Balancing of An AccountDocument3 pagesBalancing of An AccountaNo ratings yet

- Assignment No 1 FinalDocument13 pagesAssignment No 1 FinalMuhammad AwaisNo ratings yet

- Guide To Prepare Ledger AccountsDocument6 pagesGuide To Prepare Ledger AccountsSami KhanNo ratings yet

- CCP102Document23 pagesCCP102api-3849444No ratings yet

- Accounting AssignmentDocument3 pagesAccounting AssignmentJohn RazaNo ratings yet

- Chapter 7 LedgerDocument18 pagesChapter 7 LedgerJumayma MaryamNo ratings yet

- CCP102Document21 pagesCCP102api-3849444No ratings yet

- Assignment 4Document2 pagesAssignment 4Samira AlhashimiNo ratings yet

- Partnership Accounts - IDocument23 pagesPartnership Accounts - IM JEEVARATHNAM NAIDU100% (1)

- AccountsDocument44 pagesAccountsadityachy.817No ratings yet

- Susquehanna Equipment RentalsDocument17 pagesSusquehanna Equipment RentalsFaiza SattiNo ratings yet

- CLASS WORK 2 (11 DEC) CHP 6Document14 pagesCLASS WORK 2 (11 DEC) CHP 6Isha KatiyarNo ratings yet

- Depre Sums 4-1Document6 pagesDepre Sums 4-1Pradeep NairNo ratings yet

- GJ No. 1Document6 pagesGJ No. 1AN AdeNo ratings yet

- 5 0Document14 pages5 0Shashwat sai VyasNo ratings yet

- Date Particulars J.F DR CR Balance: Cash AccountDocument4 pagesDate Particulars J.F DR CR Balance: Cash AccountAkash AliNo ratings yet

- LedgerDocument8 pagesLedgerAnkur AryaNo ratings yet

- Slowhand Services General Journal For The Month Ended of May, 2011 Date Explanation Ref DR CRDocument19 pagesSlowhand Services General Journal For The Month Ended of May, 2011 Date Explanation Ref DR CRAnna Altahea ArthicNo ratings yet

- Acctg Books - Subsidiary Ledgers IllustrationDocument9 pagesAcctg Books - Subsidiary Ledgers IllustrationCorn SaladNo ratings yet

- Bank Reconciliation StatementDocument2 pagesBank Reconciliation StatementHARIKIRAN PRNo ratings yet

- Introduction To AccountingDocument3 pagesIntroduction To AccountingHARIKIRAN PRNo ratings yet

- Span of ControlDocument2 pagesSpan of ControlHARIKIRAN PRNo ratings yet

- Principles of ManagementDocument2 pagesPrinciples of ManagementHARIKIRAN PRNo ratings yet

- Social & Ethical Responsibilities of ManagementDocument2 pagesSocial & Ethical Responsibilities of ManagementHARIKIRAN PRNo ratings yet

- International Trade TheoriesDocument5 pagesInternational Trade TheoriesHARIKIRAN PRNo ratings yet

- Archived DataDocument2 pagesArchived DataTim SchlankNo ratings yet

- Jan 2024Document27 pagesJan 2024izzneqaylNo ratings yet

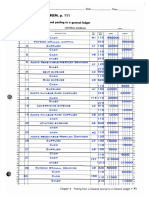

- Mastery Problem, 111: Journalizing Transactions and Posting To A General LedgerDocument3 pagesMastery Problem, 111: Journalizing Transactions and Posting To A General LedgerJames SargentNo ratings yet

- When Transactions Are Transferred Into Concerned Account The System Is Called LedgerDocument32 pagesWhen Transactions Are Transferred Into Concerned Account The System Is Called LedgerAjay Kumar SharmaNo ratings yet

- FDocument2 pagesFPravat mallik100% (2)

- 2020 Statement of Account: PBT Muhammad Ridwan Bin Ab WahabDocument3 pages2020 Statement of Account: PBT Muhammad Ridwan Bin Ab WahabMuhammad RidwanNo ratings yet

- Journal and LedgerDocument23 pagesJournal and Ledgerfarooq.haqiq2012No ratings yet

- Kelompok 6 - Akuntansi Dasar - Chapter 2Document22 pagesKelompok 6 - Akuntansi Dasar - Chapter 2Awun Sukma100% (1)

- Bony BZW - Gbs Feed BRD v1.0Document15 pagesBony BZW - Gbs Feed BRD v1.0umeshchandra0520No ratings yet

- 2019 2020Document16 pages2019 2020Raj KamaniNo ratings yet

- Chapter 2 - Recording ProcessDocument35 pagesChapter 2 - Recording ProcessMinetteGabrielNo ratings yet

- CHP 4 MCQDocument5 pagesCHP 4 MCQskynemesis3No ratings yet

- Buku Kerja Tugas Praktek Mandiri Lab Auditing (Eksi4414) - TUGAS 1 S/D 8Document2 pagesBuku Kerja Tugas Praktek Mandiri Lab Auditing (Eksi4414) - TUGAS 1 S/D 8Laylia LatifahNo ratings yet

- 08 Jan 2024 - 514002AccStmtDownloadReportDocument12 pages08 Jan 2024 - 514002AccStmtDownloadReportshas2sriNo ratings yet

- Journalizing, Posting, Preparing Trial Balance Week 2 CheckPointDocument6 pagesJournalizing, Posting, Preparing Trial Balance Week 2 CheckPointmrnick1102No ratings yet

- Cib GF Jan To Dec 2018Document413 pagesCib GF Jan To Dec 2018Jerwin Cases TiamsonNo ratings yet

- Yfc Projects PVT Ltd. (New Delhi)Document1 pageYfc Projects PVT Ltd. (New Delhi)jatincasualNo ratings yet

- 2006-2007 Ledger LKR AF RevalDocument1,422 pages2006-2007 Ledger LKR AF RevalShamin RanaweeraNo ratings yet

- Accounting Journal Practice: Date Particular Account Type Debit Account TypeDocument4 pagesAccounting Journal Practice: Date Particular Account Type Debit Account TypeRavi Modi100% (1)

- Ns (Klasik) Pabrik Tas Bigbag - Pramestya K.N (Xii-Akl 1)Document2 pagesNs (Klasik) Pabrik Tas Bigbag - Pramestya K.N (Xii-Akl 1)29. Pramestya Khoirun Nisa'No ratings yet

- General Ledger (Detail) PD MITRA DES 16 REV 2018Document7 pagesGeneral Ledger (Detail) PD MITRA DES 16 REV 2018Faie RifaiNo ratings yet

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document1 pagePenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)THIEVIYASREE A/P LECHUMANAN MoeNo ratings yet

- 3.2.3 Record - The Ledger (T-Accounts)Document3 pages3.2.3 Record - The Ledger (T-Accounts)andelka2No ratings yet

- Addl Correction of TB Errors - 20200921 - 0002Document3 pagesAddl Correction of TB Errors - 20200921 - 0002Dalemma FranciscoNo ratings yet

- Orimhl HYEPJz TCB ZDocument15 pagesOrimhl HYEPJz TCB ZoneofmymanyNo ratings yet

- Swifto A Unit of API Holding Apr 22 To Sept 22Document6 pagesSwifto A Unit of API Holding Apr 22 To Sept 22Remedycube PharmaceuticalsNo ratings yet

- Bookkeeping TemplatesDocument51 pagesBookkeeping TemplatesKyle100% (2)

- Ajanta Ele Gold Mobile ZebronicsDocument1 pageAjanta Ele Gold Mobile ZebronicsRajkumar WadhwaniNo ratings yet

- Dr. Panjwani Center For Molecular Medicine & Drug Research Diagnostic Lab & Clinical Research Facility University of KarachiDocument4 pagesDr. Panjwani Center For Molecular Medicine & Drug Research Diagnostic Lab & Clinical Research Facility University of KarachiIbtehaj SheikhNo ratings yet

- Employee Reimbursement Balance PDFDocument38 pagesEmployee Reimbursement Balance PDFary.ardyanNo ratings yet