You might also like

- Financial Markets & Institutions 1. Definition of Financial SystemDocument4 pagesFinancial Markets & Institutions 1. Definition of Financial SystempragyaNo ratings yet

- Aditi Basak: NTPC LimitedDocument7 pagesAditi Basak: NTPC LimitedAditi Basak ChakrabortyNo ratings yet

- International Banking and Money MarketDocument28 pagesInternational Banking and Money MarketNiharika Satyadev JaiswalNo ratings yet

- Transaction ExposureDocument25 pagesTransaction ExposureAmit SrivastavaNo ratings yet

- Treasury ManagementDocument47 pagesTreasury Managementsinghsudhir261No ratings yet

- 11 CHPTDocument6 pages11 CHPTI IvaNo ratings yet

- Arbitrage Speculation and Hedging in ForDocument62 pagesArbitrage Speculation and Hedging in ForNihar RanjanNo ratings yet

- Treasury Management in Banking - Sem 4Document4 pagesTreasury Management in Banking - Sem 4payablesNo ratings yet

- Answer TreasyDocument7 pagesAnswer TreasyShraddhey JainNo ratings yet

- FM&BODocument17 pagesFM&BOvinaydevrukhkar2629No ratings yet

- Discuss The Importance of International Finance in The Context of Indian EconomyDocument12 pagesDiscuss The Importance of International Finance in The Context of Indian EconomyBIKRAM KUMAR BEHERANo ratings yet

- FM ClipDocument16 pagesFM ClipNidhi SatvekarNo ratings yet

- FMO Unit 1Document8 pagesFMO Unit 1aakashsankhla33No ratings yet

- Ethical Practice in Correspondent BankingDocument35 pagesEthical Practice in Correspondent Bankingmahesh ojhaNo ratings yet

- Introduction To Financial Markets and Institutions:: Hide Links Within DefinitionsDocument10 pagesIntroduction To Financial Markets and Institutions:: Hide Links Within DefinitionsfananjelinaNo ratings yet

- Consumers and TravelersDocument11 pagesConsumers and TravelersRahul AnandNo ratings yet

- Integrated Forex and Treasury Operations by Banks in India: AbhinavDocument21 pagesIntegrated Forex and Treasury Operations by Banks in India: AbhinavNagesh35No ratings yet

- International FinanceDocument8 pagesInternational Financesarah IsharatNo ratings yet

- International Banking LawDocument10 pagesInternational Banking LawMir ArastooNo ratings yet

- Money MarketsDocument13 pagesMoney MarketsZiedwrick Ayson DicarNo ratings yet

- Financial MarketDocument14 pagesFinancial MarketkomalNo ratings yet

- DIB 02 - 202 International Trade and Finance - 03Document13 pagesDIB 02 - 202 International Trade and Finance - 03farhadcse30No ratings yet

- Assignment No 02Document13 pagesAssignment No 02Shivani BalaniNo ratings yet

- Iinternational Finacial ManagementDocument24 pagesIinternational Finacial ManagementSushma GNo ratings yet

- ASSIGNMENT International Banking & Foreign Exchange ManagementDocument18 pagesASSIGNMENT International Banking & Foreign Exchange Managementdhawalbaria7No ratings yet

- International Banking and Foreign Exchnage ManagementDocument6 pagesInternational Banking and Foreign Exchnage ManagementPrashant AhujaNo ratings yet

- Ge AssignmentDocument9 pagesGe AssignmentNidhuNo ratings yet

- Money Markets: For A Period Longer Than 1 Year, in Form of Both Debt & Equity)Document5 pagesMoney Markets: For A Period Longer Than 1 Year, in Form of Both Debt & Equity)api-19893912No ratings yet

- Chapter Two Financial Institutions and Their Operations LectureDocument147 pagesChapter Two Financial Institutions and Their Operations LectureAbdiNo ratings yet

- Lim Yew Joon B19080668 FMI Tutorial 4Document7 pagesLim Yew Joon B19080668 FMI Tutorial 4Jing HangNo ratings yet

- FINS 3616 Tutorial Questions-Week 6-AnswersDocument7 pagesFINS 3616 Tutorial Questions-Week 6-AnswersOscarHigson-SpenceNo ratings yet

- CapitalDocument5 pagesCapitalLyn AmbrayNo ratings yet

- Finm3404 NotesDocument20 pagesFinm3404 NotesHenry WongNo ratings yet

- Master of Business Administration 42Document7 pagesMaster of Business Administration 42ali_rahim1988No ratings yet

- Capital BudgetingDocument15 pagesCapital BudgetingAishvarya PujarNo ratings yet

- Ict2 ST Agnes Bulaon Jun 7pmquizDocument18 pagesIct2 ST Agnes Bulaon Jun 7pmquizArjeune Victoria BulaonNo ratings yet

- Finance FatDocument28 pagesFinance Fatruchitac28No ratings yet

- Foreign Exchange RiskDocument5 pagesForeign Exchange RiskPushpa BaruaNo ratings yet

- Do You Think Having A Stock Market Is A Necessity? Give Your Reasons WhyDocument5 pagesDo You Think Having A Stock Market Is A Necessity? Give Your Reasons WhyCẩm NhungNo ratings yet

- Money & Banking: Capitalist EconomiesDocument7 pagesMoney & Banking: Capitalist Economiesmabvuto phiriNo ratings yet

- Chapter 1 Financial Markets and Institutions 1Document48 pagesChapter 1 Financial Markets and Institutions 1Gowtham SrinivasNo ratings yet

- Done Motives For Using International Financial MarketsDocument6 pagesDone Motives For Using International Financial Marketskingsley Bill Owusu NinepenceNo ratings yet

- IF Internals 1Document11 pagesIF Internals 1Amith AlphaNo ratings yet

- Money MarketsDocument4 pagesMoney Marketskrissamarie.chuaNo ratings yet

- Treasury Management AssignmentDocument8 pagesTreasury Management AssignmentAnkit JugranNo ratings yet

- Analyzing Forex Exposure of Infosys: CIA-1 OF International Financial ManagementDocument12 pagesAnalyzing Forex Exposure of Infosys: CIA-1 OF International Financial ManagementNehal SharmaNo ratings yet

- International FinanceDocument11 pagesInternational Financerohit chaudharyNo ratings yet

- Indian Monetary Policy and Its Impact On Indian Money MarketDocument4 pagesIndian Monetary Policy and Its Impact On Indian Money MarketNeeraj DaniNo ratings yet

- Money Market TMDocument6 pagesMoney Market TMpetut zipagangNo ratings yet

- The Role of Money Market in Indian Economy (Growth) : SKMD Imran, G.Harikrishna, M.UpendraDocument13 pagesThe Role of Money Market in Indian Economy (Growth) : SKMD Imran, G.Harikrishna, M.UpendraPrabhu SahuNo ratings yet

- Bank Interview Question For Business GraduateDocument7 pagesBank Interview Question For Business GraduateHumayun KabirNo ratings yet

- Scheduled Banks in India:: Market Segments of Money Market in India AreDocument4 pagesScheduled Banks in India:: Market Segments of Money Market in India AreTaltson SunnyNo ratings yet

- Basic Banking ConceptsDocument17 pagesBasic Banking ConceptsVishnuvardhan VishnuNo ratings yet

- Basic Banking ConceptsDocument17 pagesBasic Banking ConceptsVyasraj Singamodi100% (1)

- XXX Final FimDocument50 pagesXXX Final FimSiddhesh RaulNo ratings yet

- Money BankingDocument11 pagesMoney BankingRose DallyNo ratings yet

- International Banking and Money Market: Chapter ObjectiveDocument21 pagesInternational Banking and Money Market: Chapter ObjectiveElla Marie WicoNo ratings yet

- FMI CH 4 Financial Markets in The Financial SystemDocument25 pagesFMI CH 4 Financial Markets in The Financial SystemYared GirmaNo ratings yet

- Introduction To Securities and InvestmentDocument26 pagesIntroduction To Securities and InvestmentJerome GaliciaNo ratings yet

- Ramiro, Lorren - Money MarketsDocument4 pagesRamiro, Lorren - Money Marketslorren ramiroNo ratings yet

- Insurance and Risk ManagementDocument6 pagesInsurance and Risk Managementbhupendra mehraNo ratings yet

- International Banking and ForexDocument4 pagesInternational Banking and Forexbhupendra mehraNo ratings yet

- Business Ethics Governance and RisksDocument7 pagesBusiness Ethics Governance and Risksbhupendra mehraNo ratings yet

- Research MethodologyDocument6 pagesResearch Methodologybhupendra mehraNo ratings yet

- Financial Accounting and AnalysisDocument4 pagesFinancial Accounting and Analysisbhupendra mehraNo ratings yet

- Business EconomicsDocument4 pagesBusiness Economicsbhupendra mehraNo ratings yet

- Business CommunicationDocument6 pagesBusiness Communicationbhupendra mehraNo ratings yet

- Essentials of HRMDocument7 pagesEssentials of HRMbhupendra mehraNo ratings yet

- Tender 0 buycon43.BKPL - BarauniDocument105 pagesTender 0 buycon43.BKPL - BarauniVishal ShrivastavaNo ratings yet

- Chronology of Important Events in The History of The Reserve BankDocument4 pagesChronology of Important Events in The History of The Reserve BankBishwajitSinhaNo ratings yet

- International Finance JUNE 2022Document9 pagesInternational Finance JUNE 2022Rajni KumariNo ratings yet

- Role of RBI in Indian EconomyDocument2 pagesRole of RBI in Indian Economynikitasharma88_49144No ratings yet

- NRI - Questionaire (Non Medical)Document2 pagesNRI - Questionaire (Non Medical)Mexico EnglishNo ratings yet

- ACT - NET BillDocument2 pagesACT - NET Billsourav84No ratings yet

- GP 22002166Document1 pageGP 22002166ashishmehta736No ratings yet

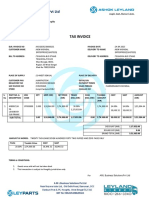

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)raviNo ratings yet

- Chapter 4, Money ExchangeDocument11 pagesChapter 4, Money ExchangeAfjal khanNo ratings yet

- MBF14e Chap10 Transaction PbmsDocument19 pagesMBF14e Chap10 Transaction PbmsQurratul Asmawi100% (2)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)ankurNo ratings yet

- Currency Derivatives: by "Me"Document15 pagesCurrency Derivatives: by "Me"Shikhar AroraNo ratings yet

- Dev of RupeeDocument37 pagesDev of RupeeRonitSingNo ratings yet

- AMA School of Medicine - Makati Campus Fee Structure PDFDocument1 pageAMA School of Medicine - Makati Campus Fee Structure PDFrishikeshkallaNo ratings yet

- Publishing AgreementDocument4 pagesPublishing AgreementTasneem BanoNo ratings yet

- 200 Questions of Economics With Answers Including 8 Chapters..Document21 pages200 Questions of Economics With Answers Including 8 Chapters..Lea PortalNo ratings yet

- Weekly One Liners 08th To 14th August 2022Document10 pagesWeekly One Liners 08th To 14th August 2022RAhul sNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ajay Gupta0% (1)

- Fedai RulesDocument36 pagesFedai RulesManipal SinghNo ratings yet

- PNB Housing FinanceDocument12 pagesPNB Housing FinanceManav SinghNo ratings yet

- Forex For CAIIBDocument6 pagesForex For CAIIBkushalnadekarNo ratings yet

- BPCLDocument173 pagesBPCLmitr82No ratings yet

- Sealdah Division-Electrical - Eleg-Ot-989-2022-23 - 21-06-2023Document5 pagesSealdah Division-Electrical - Eleg-Ot-989-2022-23 - 21-06-2023ADEE G GRCNo ratings yet

- Floating Exchange RatesDocument6 pagesFloating Exchange RatesYukiyo LangevinNo ratings yet

- Final Manpower TenderEZ TS 1102Document76 pagesFinal Manpower TenderEZ TS 1102rafikul123No ratings yet

- Anti Termite BoqDocument2 pagesAnti Termite BoqAbu Mariam100% (1)

- IFM Notes Full Rudramurthy SirDocument94 pagesIFM Notes Full Rudramurthy SirSachin PatilNo ratings yet

- New Mondal - Pedal - Sub Frame 1-3Document1 pageNew Mondal - Pedal - Sub Frame 1-3Ashirwad BanerjeeNo ratings yet