You might also like

- Chambers MnA in Technology - VN Chapter - HongBui (En) 2023Document21 pagesChambers MnA in Technology - VN Chapter - HongBui (En) 2023Nguyen Hoang Phuong UyenNo ratings yet

- Compendious Study 2021 (4th Edition)Document64 pagesCompendious Study 2021 (4th Edition)Mirza Mustafa Bin Adnan BaigNo ratings yet

- Global Withholding Taxes Guide 2023 KpmgDocument78 pagesGlobal Withholding Taxes Guide 2023 KpmgVojdan TrajkovskiNo ratings yet

- Chambers & Partners - India - Gaming Law 2022Document37 pagesChambers & Partners - India - Gaming Law 2022Prerna PatilNo ratings yet

- Afghanistan Tax Card FinalDocument17 pagesAfghanistan Tax Card FinalSalman XrNo ratings yet

- Mid-2 NCHDocument52 pagesMid-2 NCHKarthikNo ratings yet

- Singapore Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreDocument28 pagesSingapore Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax Centrehằng phạmNo ratings yet

- VALUATIONDocument25 pagesVALUATIONAlekh PandeyNo ratings yet

- UntitledDocument310 pagesUntitledChiara WhiteNo ratings yet

- 2022 Edition of The Guide To Doing Business in OmanDocument25 pages2022 Edition of The Guide To Doing Business in OmanafrahNo ratings yet

- Doing Business Guide Lebanon PDFDocument14 pagesDoing Business Guide Lebanon PDFRoy SaadNo ratings yet

- Indonesia Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreDocument26 pagesIndonesia Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreIsnan Hari MardikaNo ratings yet

- Taxation I Course SyllabusDocument4 pagesTaxation I Course Syllabuszeigfred badanaNo ratings yet

- KPMG Foreign Taxation India - 2018-v2Document38 pagesKPMG Foreign Taxation India - 2018-v2Sai Kiran ReddyNo ratings yet

- Corporate M&A - Indonesia 2022Document13 pagesCorporate M&A - Indonesia 2022Andhika Hananta RNo ratings yet

- Course Information Pibt v3Document3 pagesCourse Information Pibt v379569zdqtwNo ratings yet

- Sri Lanka 2018 PDFDocument24 pagesSri Lanka 2018 PDFSoofi AthamNo ratings yet

- GX Deloitte Global Mining Tax Trends 2017Document40 pagesGX Deloitte Global Mining Tax Trends 2017Pran RNo ratings yet

- Compendious Study - Doing Business in Pakistan (3rd Edition) PDFDocument57 pagesCompendious Study - Doing Business in Pakistan (3rd Edition) PDFMuhammad Nauman Hafeez KhanNo ratings yet

- Business Tax Guide2009Document30 pagesBusiness Tax Guide2009HoshikageNo ratings yet

- Ethics Digest FinalDocument126 pagesEthics Digest FinalLachica KeduNo ratings yet

- PERCENTAGE TAX RATES FOR VARIOUS INDUSTRIESDocument21 pagesPERCENTAGE TAX RATES FOR VARIOUS INDUSTRIESCarla Zante0% (1)

- Botswana Banking Law GuideDocument13 pagesBotswana Banking Law GuideMasego MatheoNo ratings yet

- Definitive global guide to securitisation law and practiceDocument25 pagesDefinitive global guide to securitisation law and practicejohn pynchonNo ratings yet

- db0612Document20 pagesdb0612RaghaNo ratings yet

- Coporate Amalgamation EtcDocument19 pagesCoporate Amalgamation EtcPravin KakadeNo ratings yet

- Comprehensive Income Taxation Somera (4!29!14)Document200 pagesComprehensive Income Taxation Somera (4!29!14)Moi Warhead0% (1)

- Business Income Tax Guide FinalDocument40 pagesBusiness Income Tax Guide FinalOlaNo ratings yet

- Franchise AgreementDocument64 pagesFranchise AgreementEmmanuel C. DumayasNo ratings yet

- ACCTG 603. AFAR by EMGLDocument1 pageACCTG 603. AFAR by EMGLErika LanezNo ratings yet

- Philippines 2018 PDFDocument28 pagesPhilippines 2018 PDFJohnryan Anthony CabatacNo ratings yet

- Sesi 2 - Bpk. Darussalam - International Taxation DDTC-1Document35 pagesSesi 2 - Bpk. Darussalam - International Taxation DDTC-1ridy venny teffendyNo ratings yet

- On Standard CharteredDocument11 pagesOn Standard Charterednitin01.snetNo ratings yet

- Doing Business in Oman - by SASLODocument21 pagesDoing Business in Oman - by SASLOPMO Oman ProjectsNo ratings yet

- Trinidad & Tobago TaxDocument26 pagesTrinidad & Tobago TaxHaydn Dunn100% (4)

- Introduction To IFRS 6th Ed PDFDocument563 pagesIntroduction To IFRS 6th Ed PDFSaad Khan YT100% (1)

- Pajak Internasional Singgih 050318Document87 pagesPajak Internasional Singgih 050318Irham FathoniNo ratings yet

- Final Tax PDFDocument50 pagesFinal Tax PDFMicol Villaflor Ü100% (1)

- (Elspeth Deards) Practice Notes On Partnership Law PDFDocument153 pages(Elspeth Deards) Practice Notes On Partnership Law PDFBee RahmingNo ratings yet

- AlltDocument237 pagesAlltMuhammad Tanko100% (1)

- T I E L: I U: He Ndian Qualisation Evy Nelegant But Not NexpectedDocument24 pagesT I E L: I U: He Ndian Qualisation Evy Nelegant But Not NexpectedSTQNo ratings yet

- Ncert Solutions For Class 12 Accountancy 22 May Chapter 2 Accounting For Partnership Firms Basic ConceptsDocument85 pagesNcert Solutions For Class 12 Accountancy 22 May Chapter 2 Accounting For Partnership Firms Basic Conceptskankariya1424No ratings yet

- Chamber Global Practice Guide Gaming LawsDocument14 pagesChamber Global Practice Guide Gaming Lawsramya raviNo ratings yet

- Carlos Pinedo Texidor INTERNATIONALTAXATIONTEST2021-BDocument4 pagesCarlos Pinedo Texidor INTERNATIONALTAXATIONTEST2021-Bdanosito.garciaNo ratings yet

- XII Accountancy Notes All Chapters MR - Mohan H BaksaniDocument176 pagesXII Accountancy Notes All Chapters MR - Mohan H BaksaniALAY SINGHNo ratings yet

- Prepares Financial Statements of a PartnershipDocument21 pagesPrepares Financial Statements of a PartnershipMihara AmaratungaNo ratings yet

- Chambers Global Practice Guides Private Wealth 2020 - Japan ChapterDocument9 pagesChambers Global Practice Guides Private Wealth 2020 - Japan ChapterYoNo ratings yet

- Bulgarian Taxes: Pocket GuideDocument27 pagesBulgarian Taxes: Pocket GuidedeviltryNo ratings yet

- Doing Business Guide Kuwait PDFDocument12 pagesDoing Business Guide Kuwait PDFBooraj DuraisamyNo ratings yet

- Me - Tax Handbook 2022Document84 pagesMe - Tax Handbook 2022lscable.hannahNo ratings yet

- Note 6Document55 pagesNote 6sohamdivekar9867No ratings yet

- Nhóm 7 Tax Evasion and Avoidance in Multinational CompaniesDocument6 pagesNhóm 7 Tax Evasion and Avoidance in Multinational CompaniesHưng TrịnhNo ratings yet

- Cameroon - Country Key FeaturesDocument5 pagesCameroon - Country Key FeaturesTheo HendricksNo ratings yet

- Forms of business organization and partnershipsDocument2 pagesForms of business organization and partnershipsJaypee ManiegoNo ratings yet

- Real Estate Rental Income As Business' Income For State Tax PurposesDocument20 pagesReal Estate Rental Income As Business' Income For State Tax PurposesfalkynNo ratings yet

- Lease QuestionsDocument12 pagesLease Questionszakhonalubanzi95No ratings yet

- Tax Management on Outbound InvestmentDocument15 pagesTax Management on Outbound Investmentdummy yummyNo ratings yet

- Application Convention PB 000Document31 pagesApplication Convention PB 000Farid NabiliNo ratings yet

- Itc LTD: ValuationsDocument11 pagesItc LTD: ValuationsMera Birthday 2021No ratings yet

- Coffee Truck Business Plan PDFDocument49 pagesCoffee Truck Business Plan PDFjesicalarson123No ratings yet

- Ultimate Social Enterprise Pitch Deck TemplateDocument31 pagesUltimate Social Enterprise Pitch Deck TemplatejaishitaNo ratings yet

- Literature Review On Investment BankingDocument8 pagesLiterature Review On Investment Bankingfdnmffvkg100% (1)

- Lesson 10 Stock and BondsDocument4 pagesLesson 10 Stock and BondsIrene FranciscoNo ratings yet

- Mastering Options Trading: by Mentor - Ravi ChandiramaniDocument120 pagesMastering Options Trading: by Mentor - Ravi ChandiramanivivekNo ratings yet

- Cibil - Report (P - JAYSINGH YADAV - 26 - 05 - 2023 12 - 23 - 04)Document5 pagesCibil - Report (P - JAYSINGH YADAV - 26 - 05 - 2023 12 - 23 - 04)Geeta MallahNo ratings yet

- Business Bankruptcy Prediction Models A Significant Study of The Altman'sDocument9 pagesBusiness Bankruptcy Prediction Models A Significant Study of The Altman'sTathianaNo ratings yet

- Mutual Fund SWP Calculator Plan 1Document8 pagesMutual Fund SWP Calculator Plan 1Yada GiriNo ratings yet

- Managerial Economics OCT 2022Document2 pagesManagerial Economics OCT 2022Dr Praveen KumarNo ratings yet

- Preface: National Institute of Financial Market (NIFMDocument65 pagesPreface: National Institute of Financial Market (NIFMSankitNo ratings yet

- Internship ReportDocument38 pagesInternship ReportManasvi DoshiNo ratings yet

- Cma Fina Group4 All MCQDocument205 pagesCma Fina Group4 All MCQtusharjaipur7No ratings yet

- Agri-SosioEkonomi Analysis Pig Farming Financial FeasibilityDocument8 pagesAgri-SosioEkonomi Analysis Pig Farming Financial FeasibilityChristuvel ManansangNo ratings yet

- Economics Assignment 2-NewDocument21 pagesEconomics Assignment 2-New2003 raianNo ratings yet

- English File Intermediate. Workbook With Key (Christina Latham-Koenig, Clive Oxenden Etc.) (Z-Library)Document2 pagesEnglish File Intermediate. Workbook With Key (Christina Latham-Koenig, Clive Oxenden Etc.) (Z-Library)dzinedvisionNo ratings yet

- Task 4 - Model Answer - RevisedDocument1 pageTask 4 - Model Answer - RevisedRoshan GaikwadNo ratings yet

- Capital Structure and Financial Performance in NigeriaDocument12 pagesCapital Structure and Financial Performance in Nigeriaalikali usmanNo ratings yet

- The "Kind Martin" Strategy - Official Olymp Trade BlogDocument7 pagesThe "Kind Martin" Strategy - Official Olymp Trade BlogGopal NapoleonNo ratings yet

- Information Memorandum Series - VII NewDocument174 pagesInformation Memorandum Series - VII NewRAHUL AGARWALNo ratings yet

- Distance Test PDFDocument10 pagesDistance Test PDFSoneni HandaNo ratings yet

- Also, We Have Many Other Ebooks and ReportsDocument15 pagesAlso, We Have Many Other Ebooks and ReportsZhou RuojingNo ratings yet

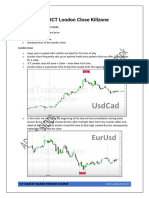

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- Financial Ratio Analysis 1682974149 PDFDocument55 pagesFinancial Ratio Analysis 1682974149 PDFMerve Köse100% (1)

- USA State Wise Email Leads PDFDocument7 pagesUSA State Wise Email Leads PDFBriltex Industries0% (1)

- 3032 Main ProjectDocument71 pages3032 Main Projectamanmukri1No ratings yet

- CMFAS Module 8A (1 Edition) Mock Paper: © Singapore College of InsuranceDocument13 pagesCMFAS Module 8A (1 Edition) Mock Paper: © Singapore College of InsuranceMalvin Tan100% (1)

- 3g-Income-Statement FinalDocument13 pages3g-Income-Statement FinalPERCIVAL DOMINGONo ratings yet

- 23.11.16.SUPPLIER ENDORSEMENT VertifluteDocument3 pages23.11.16.SUPPLIER ENDORSEMENT VertifluteChristian DavidNo ratings yet

- Accounting Grade 11 Term 3 Week 4 - 2020Document6 pagesAccounting Grade 11 Term 3 Week 4 - 2020adriana espinoza de los monterosNo ratings yet

- SallDocument59 pagesSallMalik Kumail KumailNo ratings yet

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASFrom EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASRating: 3 out of 5 stars3/5 (5)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseFrom EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNo ratings yet

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicFrom EverandThe Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicRating: 5 out of 5 stars5/5 (1)

- Competition and Antitrust Law: A Very Short IntroductionFrom EverandCompetition and Antitrust Law: A Very Short IntroductionRating: 5 out of 5 stars5/5 (3)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsFrom EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsRating: 5 out of 5 stars5/5 (24)

- Indian Polity with Indian Constitution & Parliamentary AffairsFrom EverandIndian Polity with Indian Constitution & Parliamentary AffairsNo ratings yet

- California Employment Law: An Employer's Guide: Revised and Updated for 2024From EverandCalifornia Employment Law: An Employer's Guide: Revised and Updated for 2024No ratings yet

- The Real Estate Investing Diet: Harnessing Health Strategies to Build Wealth in Ninety DaysFrom EverandThe Real Estate Investing Diet: Harnessing Health Strategies to Build Wealth in Ninety DaysNo ratings yet

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessFrom EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessRating: 5 out of 5 stars5/5 (1)