You might also like

- Financial Accounting, 7e by Pfeiffer, Hanlon, Magee 2023, Test BankDocument32 pagesFinancial Accounting, 7e by Pfeiffer, Hanlon, Magee 2023, Test BankTest bank World0% (1)

- Famba 8e Test Bank Mod01 TF MC 093020 1Document16 pagesFamba 8e Test Bank Mod01 TF MC 093020 1Trisha Mae BeltranNo ratings yet

- Financial Accounting and Reporting Learning ModulesDocument126 pagesFinancial Accounting and Reporting Learning ModulesLovelyn Joy Solutan100% (2)

- Financial and Managerial Accounting For Mbas 4th Edition Easton Test Bank 191001163059Document32 pagesFinancial and Managerial Accounting For Mbas 4th Edition Easton Test Bank 191001163059josh100% (1)

- Clep Financial AccountingDocument5 pagesClep Financial AccountingAlexandraSammyDlodloNo ratings yet

- Financial Statement Analysis and Valuation 4th Edition Easton Test BankDocument30 pagesFinancial Statement Analysis and Valuation 4th Edition Easton Test BankTroyKnappdpci100% (15)

- Acca Afm s18 NotesDocument9 pagesAcca Afm s18 NotesUsman MaqsoodNo ratings yet

- ASE20104 - Examiner Report - March 2019 PDFDocument14 pagesASE20104 - Examiner Report - March 2019 PDFAung Zaw HtweNo ratings yet

- Restore Classic Cars Business PlanDocument33 pagesRestore Classic Cars Business PlanCristianbraicu0% (1)

- TBDocument31 pagesTBBenj LadesmaNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No ratings yet

- Far ReviewerDocument21 pagesFar Reviewerbea kullinNo ratings yet

- Pas 38Document34 pagesPas 38Abegail AdoraNo ratings yet

- Business PlanDocument11 pagesBusiness Planrrahul209467% (3)

- Financial Accounting March 2009 Marks PlanDocument14 pagesFinancial Accounting March 2009 Marks Plankarlr9No ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Module 3Document46 pagesModule 3ThelmaNo ratings yet

- Chapter 1Document24 pagesChapter 1mobinil10% (1)

- Cost Sheet Exercise 1Document3 pagesCost Sheet Exercise 1Phaniraj LenkalapallyNo ratings yet

- Case Study:Napolact S.A: Transilvania University of Brasov Faculty of Economic Sciences and BusinessDocument12 pagesCase Study:Napolact S.A: Transilvania University of Brasov Faculty of Economic Sciences and BusinessMarian DobrinNo ratings yet

- ASE20091 April 2016 Examiner ReportDocument7 pagesASE20091 April 2016 Examiner ReportTin Zar ThweNo ratings yet

- ASE20091 Examiner Report November 2019Document14 pagesASE20091 Examiner Report November 2019ringotgNo ratings yet

- Examiner Report ASE20104 Sept 18Document18 pagesExaminer Report ASE20104 Sept 18Aung Zaw HtweNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document22 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- ASE20097 Examiner Report December 2018 PDFDocument11 pagesASE20097 Examiner Report December 2018 PDFPhyu Phyu MoeNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document19 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document19 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- ASE20104 - Examiner Report - November 2018Document14 pagesASE20104 - Examiner Report - November 2018Aung Zaw HtweNo ratings yet

- ASE20104 Examiner Report - March 2018Document20 pagesASE20104 Examiner Report - March 2018Aung Zaw HtweNo ratings yet

- WAC11 01 Pef 20210304Document7 pagesWAC11 01 Pef 20210304new yearNo ratings yet

- Examiner Report ASE20104 July 2018Document22 pagesExaminer Report ASE20104 July 2018Aung Zaw HtweNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document20 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- Examiner Report ASE20104 January 2018Document22 pagesExaminer Report ASE20104 January 2018Aung Zaw HtweNo ratings yet

- Examiners' Report Principal Examiner Feedback January 2020Document5 pagesExaminers' Report Principal Examiner Feedback January 2020DURAIMURUGAN MIS 17-18 MYP ACCOUNTS STAFFNo ratings yet

- Examiner Report - ASE20104 - January 2019Document13 pagesExaminer Report - ASE20104 - January 2019Aung Zaw Htwe100% (1)

- Examiner's Report For 2015 MayDocument32 pagesExaminer's Report For 2015 MaySerenaNo ratings yet

- Examiners' Report June 2014 IAL Accounting WAC02 01Document20 pagesExaminers' Report June 2014 IAL Accounting WAC02 01RafaNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document24 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- Examiners' Report January 2008: GCE Accounting (8011-9011)Document13 pagesExaminers' Report January 2008: GCE Accounting (8011-9011)RafaNo ratings yet

- IA Examiner Report 0615Document4 pagesIA Examiner Report 0615Mohammad TufelNo ratings yet

- Accounting QBDocument661 pagesAccounting QBTrang VũNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document25 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- AccountingDocument8 pagesAccountingBilal MustafaNo ratings yet

- Examiners' Report/ Principal Examiner Feedback Summer 2014: International GCSE Accounting (4AC0 - 01)Document7 pagesExaminers' Report/ Principal Examiner Feedback Summer 2014: International GCSE Accounting (4AC0 - 01)Maryam SamaahathNo ratings yet

- Examiners' Report Principal Examiner Feedback Summer 2019: Pearson Edexcel International GCSE Accounting (4AC1) 02RDocument5 pagesExaminers' Report Principal Examiner Feedback Summer 2019: Pearson Edexcel International GCSE Accounting (4AC1) 02RYan Naing TunNo ratings yet

- Pearson LCCI Certificate in Management Accounting (VRQ) Level 4Document17 pagesPearson LCCI Certificate in Management Accounting (VRQ) Level 4Aung Zaw HtweNo ratings yet

- ASE20102 - Examiner Report - November 2018Document13 pagesASE20102 - Examiner Report - November 2018Aung Zaw HtweNo ratings yet

- WAC01 - 01 - Pef - 20150305 (Accounting Edexcel IAL 2015 January Unit Examiner's Report)Document9 pagesWAC01 - 01 - Pef - 20150305 (Accounting Edexcel IAL 2015 January Unit Examiner's Report)James JoneNo ratings yet

- Test Bank For Financial Statement Analysis Valuation 4th Edition by Easton Mcanally Sommers ZhangDocument30 pagesTest Bank For Financial Statement Analysis Valuation 4th Edition by Easton Mcanally Sommers ZhangJames Martino100% (36)

- Accounting I Syllabus: Instructor's Name and Contact InformationDocument6 pagesAccounting I Syllabus: Instructor's Name and Contact InformationDino DizonNo ratings yet

- Examiner's Report: Financial Reporting (FR) June 2019Document10 pagesExaminer's Report: Financial Reporting (FR) June 2019saad aliNo ratings yet

- f7 Examreport d17Document7 pagesf7 Examreport d17rashad surxayNo ratings yet

- Accounting June 2011 Unit 2 Examiner's ReportDocument8 pagesAccounting June 2011 Unit 2 Examiner's ReportArif BillahNo ratings yet

- Examiner Reports Unit 1 (WAC01) June 2014Document16 pagesExaminer Reports Unit 1 (WAC01) June 2014RafaNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Test Bank For New Zealand Financial Accounting 6th Edition by CraigDocument67 pagesTest Bank For New Zealand Financial Accounting 6th Edition by CraigCarolparker100% (1)

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Chapter 05Document51 pagesChapter 05蓝依旎No ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Examiners' Report June 2019: IAL Accounting WAC12 01Document48 pagesExaminers' Report June 2019: IAL Accounting WAC12 01DURAIMURUGAN MIS 17-18 MYP ACCOUNTS STAFFNo ratings yet

- Question and Answer - 1Document31 pagesQuestion and Answer - 1acc-expertNo ratings yet

- Accounting in Business: Quick StudiesDocument13 pagesAccounting in Business: Quick StudiesAlex TseNo ratings yet

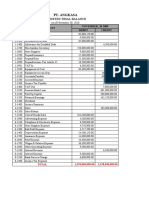

- Kerja Kelompok PT Angkasa BDocument28 pagesKerja Kelompok PT Angkasa BElisa EndrianiiNo ratings yet

- Training Completion ReportDocument40 pagesTraining Completion ReportDurga BachatNo ratings yet

- Practice Question: Recognition and MeasurementDocument2 pagesPractice Question: Recognition and MeasurementJong HannahNo ratings yet

- City Development PlanDocument139 pagesCity Development Planstolidness100% (1)

- Sibl 2006arDocument49 pagesSibl 2006aroneupperNo ratings yet

- In 2012 Satellite Systems Modified Its Model z2 Satellite ToDocument1 pageIn 2012 Satellite Systems Modified Its Model z2 Satellite ToMiroslav GegoskiNo ratings yet

- Accounts - Aditya BirlaDocument11 pagesAccounts - Aditya Birlarahul raviNo ratings yet

- Ngas OgasDocument24 pagesNgas OgasMark MlsNo ratings yet

- Trial Balance, 4 - 7 - 2022, 5 - 43 - 13 AMDocument6 pagesTrial Balance, 4 - 7 - 2022, 5 - 43 - 13 AMiwan setionoNo ratings yet

- Lecture 4Document54 pagesLecture 4premsuwaatiiNo ratings yet

- August 20 DiscussionDocument26 pagesAugust 20 DiscussionJOSCEL SYJONGTIANNo ratings yet

- CE - LiabilitiesDocument7 pagesCE - LiabilitiesJohn WIckNo ratings yet

- Urc 1Document18 pagesUrc 1Jelna CeladaNo ratings yet

- Basic BookkeepingDocument25 pagesBasic BookkeepingJovelyn AvilaNo ratings yet

- Balance Sheet of Allahabad BankDocument26 pagesBalance Sheet of Allahabad BankMemoona RizviNo ratings yet

- Adjusting Entries ProblemsDocument5 pagesAdjusting Entries ProblemsSharmaine manobanNo ratings yet

- ESOP and Sweat EquityDocument7 pagesESOP and Sweat EquityShehana RenjuNo ratings yet

- Question IA 2 - Topic 4Document2 pagesQuestion IA 2 - Topic 4YAANESHWARAN A/L CHANDRAN STUDENTNo ratings yet

- Understanding Financial StatementsDocument103 pagesUnderstanding Financial StatementsLawa LopezNo ratings yet

- Ifrs 8 Operating Segments: BackgroundDocument4 pagesIfrs 8 Operating Segments: Backgroundmusic niNo ratings yet

- Laporan Keuangan Cikarang ListrindoDocument3 pagesLaporan Keuangan Cikarang ListrindoEko H PrasetyoNo ratings yet

- Fa MCQDocument4 pagesFa MCQShivarajkumar JayaprakashNo ratings yet

- Doctora (DR - Nickmarasigan) WorksheetDocument2 pagesDoctora (DR - Nickmarasigan) Worksheetkianna doctoraNo ratings yet

- Payslip 03-01-2024Document1 pagePayslip 03-01-2024ernestkozar8No ratings yet