You might also like

- Case StudyDocument8 pagesCase StudyTHE INDIAN FOOTBALL GUYNo ratings yet

- Module 7: Case Study - The Cash Flow StatementDocument8 pagesModule 7: Case Study - The Cash Flow StatementTHE INDIAN FOOTBALL GUYNo ratings yet

- Chapter 2Document127 pagesChapter 2Dung Hoàng Khưu VõNo ratings yet

- In-House Banks Nothing NewDocument3 pagesIn-House Banks Nothing NewitreasurerNo ratings yet

- Financial Management Lecture1Document21 pagesFinancial Management Lecture1Sasha SGNo ratings yet

- Lecture 5 Financial InstitutionsDocument8 pagesLecture 5 Financial Institutionstejpalattwal23No ratings yet

- FinanceDocument10 pagesFinancePawar Shirish PrakashNo ratings yet

- Profitability of Commercial Banks: Presented By:-Ruchika Singh (MBA/10046/18) Nikhil Mishra (MBA/10051/18)Document24 pagesProfitability of Commercial Banks: Presented By:-Ruchika Singh (MBA/10046/18) Nikhil Mishra (MBA/10051/18)Manas MaheshwariNo ratings yet

- Chap 5Document23 pagesChap 5selva0% (1)

- Etano Garda AriyanDocument9 pagesEtano Garda AriyanETANO GARDA ARIYANNo ratings yet

- Bank Administration: Ratio AnalysisDocument33 pagesBank Administration: Ratio AnalysisSharma AmitNo ratings yet

- Financial Management Source #7Document49 pagesFinancial Management Source #7EDPSENPAINo ratings yet

- Cfa Books - The Analysis and Use of Financial Statements - Resume - White, Sondhi, WhiteDocument18 pagesCfa Books - The Analysis and Use of Financial Statements - Resume - White, Sondhi, Whiteshare7575100% (3)

- UntitledDocument12 pagesUntitledPrashant ChatterjeeNo ratings yet

- Axis Bank Aug. 2012Document13 pagesAxis Bank Aug. 2012Deepankar MitraNo ratings yet

- Components of Assets & Liabilities in Bank'S Balance SheetDocument7 pagesComponents of Assets & Liabilities in Bank'S Balance SheetAnonymous nx6TUjNP4No ratings yet

- Chapter 1 Banking Business and CapitalDocument49 pagesChapter 1 Banking Business and CapitalColin KmNo ratings yet

- Banking Theory and Practice Chapter FiveDocument23 pagesBanking Theory and Practice Chapter Fivemubarek oumerNo ratings yet

- Budget Statement of Cash Flow-1Document7 pagesBudget Statement of Cash Flow-1AhmedNo ratings yet

- Corporate Financing Decision (FIN 502) MBA Kathmandu University School of ManagementDocument13 pagesCorporate Financing Decision (FIN 502) MBA Kathmandu University School of ManagementShreeya SigdelNo ratings yet

- Credit Monitoring ArrangementDocument19 pagesCredit Monitoring ArrangementRachita Tilak67% (3)

- AccountingDocument16 pagesAccountingJad AbbasNo ratings yet

- Balance Sheet Analysis PresentationDocument13 pagesBalance Sheet Analysis PresentationChristian Emmanuel Jo BencaloNo ratings yet

- Executive SummaryDocument84 pagesExecutive SummaryNeha SharmaNo ratings yet

- Financial Statements, Cash Flows, and TaxesDocument27 pagesFinancial Statements, Cash Flows, and TaxeszhengcunzhangNo ratings yet

- SPCL Thrift Bank MOJICADocument2 pagesSPCL Thrift Bank MOJICARobinson MojicaNo ratings yet

- Definition of NPADocument3 pagesDefinition of NPAsajilapkNo ratings yet

- Evaluating Bank Performance: - OutlineDocument14 pagesEvaluating Bank Performance: - OutlineNeha AggarwalNo ratings yet

- Audit of BanksDocument10 pagesAudit of BanksIra Grace De Castro100% (2)

- Short Notes - Lesson 2Document2 pagesShort Notes - Lesson 2HaifaNo ratings yet

- ALM Maturity ProfileDocument16 pagesALM Maturity ProfileMorshed Chowdhury ZishanNo ratings yet

- Profitability of Commercial BanksDocument14 pagesProfitability of Commercial BanksprincevimalNo ratings yet

- Asset Liability Management StrategiesDocument9 pagesAsset Liability Management StrategiesAhnafTahmidNo ratings yet

- What Are The Basic Principals of Banking? Discuss BrieflyDocument19 pagesWhat Are The Basic Principals of Banking? Discuss BrieflyNihathamanie PereraNo ratings yet

- Cash PoolingDocument9 pagesCash PoolingGirishNo ratings yet

- Capital Structure Decision ReportDocument14 pagesCapital Structure Decision ReportPratik GanatraNo ratings yet

- Accounting Problems of Islamic BanksDocument27 pagesAccounting Problems of Islamic Banksaqas_khan100% (1)

- 1g Bingham CH 7 Prof Chauvins Instructions Student VersionDocument13 pages1g Bingham CH 7 Prof Chauvins Instructions Student VersionSalman KhalidNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Unit 6mfrbDocument46 pagesUnit 6mfrbSweety TuladharNo ratings yet

- Funds Analysis, Cash-Flow Analysis, and Financial PlanningDocument31 pagesFunds Analysis, Cash-Flow Analysis, and Financial Planningmyasir1992100% (1)

- Q/A: 4 Ways Investment Firms Make Money: Investment Banking Investing and Lending Client Services Investment Management 1. What Is Investment BankingDocument4 pagesQ/A: 4 Ways Investment Firms Make Money: Investment Banking Investing and Lending Client Services Investment Management 1. What Is Investment BankingkrstupNo ratings yet

- AAOIFI Vs IFRS: Accounting For Islamic FinanceDocument11 pagesAAOIFI Vs IFRS: Accounting For Islamic FinanceMuhammad Faisal Kamarul ZamanNo ratings yet

- Asset Liability Management Module A C.S.Balakrishnan Faculty Member, SPBT CollegeDocument43 pagesAsset Liability Management Module A C.S.Balakrishnan Faculty Member, SPBT Collegetimtim1496No ratings yet

- Libby Financial Accounting Chapter14Document7 pagesLibby Financial Accounting Chapter14Jie Bo TiNo ratings yet

- Research On Banking Sector by Witty AdvisoryDocument141 pagesResearch On Banking Sector by Witty AdvisoryAnkit GuptaNo ratings yet

- Trust Bank ICAAP ReportDocument16 pagesTrust Bank ICAAP ReportG117100% (2)

- Leverage and Risk - : Leveraged SolvencyDocument6 pagesLeverage and Risk - : Leveraged SolvencyMitu RanaNo ratings yet

- BAV Lecture 4Document25 pagesBAV Lecture 4Fluid TrapsNo ratings yet

- Working Capital: AccountancyDocument11 pagesWorking Capital: Accountancybabumba95No ratings yet

- Rose Hudgins Eighth Edition Power Point Chapter 15 JimDocument76 pagesRose Hudgins Eighth Edition Power Point Chapter 15 JimJordan FaselNo ratings yet

- UBL AnalysisDocument19 pagesUBL Analysismuhammad akramNo ratings yet

- Financial Risk Management Assignment: Submitted byDocument5 pagesFinancial Risk Management Assignment: Submitted byAnkita RathiNo ratings yet

- Concept ChecksDocument8 pagesConcept ChecksAshraful AlamNo ratings yet

- The Industry Handbook - The Banking Industry: Back To Industry ListDocument6 pagesThe Industry Handbook - The Banking Industry: Back To Industry ListVijay DevillivedNo ratings yet

- Finance Question BankDocument10 pagesFinance Question BankSameer WableNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- What is Financial Accounting and BookkeepingFrom EverandWhat is Financial Accounting and BookkeepingRating: 4 out of 5 stars4/5 (10)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- LetterDocument1 pageLetterAasim Bin BakrNo ratings yet

- Class 05Document2 pagesClass 05Aasim Bin BakrNo ratings yet

- Class 08Document2 pagesClass 08Aasim Bin BakrNo ratings yet

- Class 10Document2 pagesClass 10Aasim Bin BakrNo ratings yet

- G 2Document8 pagesG 2Aasim Bin BakrNo ratings yet

- Class 23Document4 pagesClass 23Aasim Bin BakrNo ratings yet

- G 2Document8 pagesG 2Aasim Bin BakrNo ratings yet

- Invictus: A Case Study On Online Subscription Based ServicesDocument7 pagesInvictus: A Case Study On Online Subscription Based ServicesAasim Bin BakrNo ratings yet

- Gbe MemoDocument2 pagesGbe MemoAasim Bin BakrNo ratings yet

- Roll12 BiologyDocument5 pagesRoll12 BiologyAasim Bin BakrNo ratings yet

- NMDFC PresentationDocument12 pagesNMDFC PresentationbhawakshiNo ratings yet

- How To Save Money - 8 Simple Ways To Start Saving Money PDFDocument6 pagesHow To Save Money - 8 Simple Ways To Start Saving Money PDFMark ANo ratings yet

- Memo of UnderstandingDocument4 pagesMemo of UnderstandingRaheem Drayton100% (1)

- Forbes USA - 07 October 2013Document300 pagesForbes USA - 07 October 2013Bramantyo Nugros100% (1)

- San Jose/Silicon Valley Market Report and ForecastDocument40 pagesSan Jose/Silicon Valley Market Report and ForecastNNMSANo ratings yet

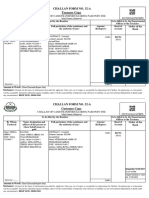

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheDocument1 pageChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into Theآرنولڈ دا فینNo ratings yet

- November 2010 India DailyDocument147 pagesNovember 2010 India DailymitbanNo ratings yet

- Math 1090 Present and Future Value Project EportfolioDocument5 pagesMath 1090 Present and Future Value Project Eportfolioapi-273422040No ratings yet

- The Adventure of The Beryl Coronet: Arthur Conan DoyleDocument13 pagesThe Adventure of The Beryl Coronet: Arthur Conan Doyleumila omalNo ratings yet

- Associated Bank v. TanDocument1 pageAssociated Bank v. TanAngie JapitanNo ratings yet

- Final Thesis Report-Yilebes A Submitted To AAUDocument122 pagesFinal Thesis Report-Yilebes A Submitted To AAUAhmed MohamedNo ratings yet

- Civ - Zuniga Notes - CreditDocument175 pagesCiv - Zuniga Notes - CreditLirio IringanNo ratings yet

- Varonis and PCI DSSDocument4 pagesVaronis and PCI DSSnchavezgNo ratings yet

- International Monetary FundDocument3 pagesInternational Monetary FundanjaliNo ratings yet

- Dork Carding 2017Document6 pagesDork Carding 2017owen011111No ratings yet

- Document ChecklistDocument2 pagesDocument ChecklistSuresh IndhumathiNo ratings yet

- FDIC Deposit Insurance CoverageDocument2 pagesFDIC Deposit Insurance CoverageSucreNo ratings yet

- SKS Microfinance Cse ReportDocument10 pagesSKS Microfinance Cse ReportKomal JainNo ratings yet

- Irrevocable TrustDocument11 pagesIrrevocable Trustamazing_pinoy50% (2)

- 7'P S of Banking in MarketingDocument15 pages7'P S of Banking in MarketingAvdhesh ChauhanNo ratings yet

- The AffidavitDocument20 pagesThe AffidavitCharlton Butler100% (1)

- Tutorial 1Document4 pagesTutorial 1Thuận Nguyễn Thị KimNo ratings yet

- Trade FinanceDocument65 pagesTrade Financeanon_879138113100% (1)

- Chapter 6 ZicaDocument45 pagesChapter 6 ZicaVainess S Zulu100% (4)

- Balance of Payment MCQS: Economic & Social Issues - Multiple Choice QuestionsDocument12 pagesBalance of Payment MCQS: Economic & Social Issues - Multiple Choice QuestionsIsmat100% (1)

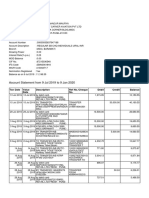

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeNo ratings yet

- Calgary Reduce: RowentaDocument44 pagesCalgary Reduce: RowentaModernBeautyNo ratings yet

- Banking Law - Law Relating To Dishonour of Cheques in India: An Analysis of Section 138 of The Negotiable Instruments ActDocument37 pagesBanking Law - Law Relating To Dishonour of Cheques in India: An Analysis of Section 138 of The Negotiable Instruments ActKashyap Kumar NaikNo ratings yet

- AchformDocument2 pagesAchformhancockmedicalsolutionsllcNo ratings yet

- Private Equity Investment Banking Hedge Funds Venture CapitalDocument26 pagesPrivate Equity Investment Banking Hedge Funds Venture Capitalpankaj_xaviersNo ratings yet