You might also like

- BioPharma Case StudyDocument4 pagesBioPharma Case StudyNaman Chhaya100% (3)

- Use Investing in People Financial Impact of Human Resources Initiatives by Cascio and BoudreauDocument3 pagesUse Investing in People Financial Impact of Human Resources Initiatives by Cascio and BoudreauDoreen0% (1)

- Upper Intermediate Unit Test 5: Grammar VocabularyDocument2 pagesUpper Intermediate Unit Test 5: Grammar VocabularyAléxia DinizNo ratings yet

- The Impact of Intangible Assets On Financial Policy With Assets Size and Leverage As Control VariablesDocument7 pagesThe Impact of Intangible Assets On Financial Policy With Assets Size and Leverage As Control VariablesaijbmNo ratings yet

- Ijebmr 847Document16 pagesIjebmr 847Amal MobarakiNo ratings yet

- 31-42 Mubarok & SiregarDocument12 pages31-42 Mubarok & Siregarmoses olanrewajuNo ratings yet

- Roa CR Der THP Hs Inter DividenDocument15 pagesRoa CR Der THP Hs Inter Dividenumar YPUNo ratings yet

- iJARS 520Document16 pagesiJARS 520Sasi KumarNo ratings yet

- Jurnal Pendukung 17 (LN)Document12 pagesJurnal Pendukung 17 (LN)Natanael PranataNo ratings yet

- ENDLESS Fida+Isti+Qur'ani Nanda+PAYMENTDocument11 pagesENDLESS Fida+Isti+Qur'ani Nanda+PAYMENTcreacion impresionesNo ratings yet

- Paper 2Document13 pagesPaper 2Richard SesaNo ratings yet

- Analysis of Financial InvestmentsDocument9 pagesAnalysis of Financial InvestmentsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Denijuliasari, 12-17 Aditya Teguh NugrohoDocument6 pagesDenijuliasari, 12-17 Aditya Teguh Nugrohoanhnp21409No ratings yet

- Effect of Financial Gearing and Financial Structure On Firm's Financial Performance Evidence From PakistanDocument13 pagesEffect of Financial Gearing and Financial Structure On Firm's Financial Performance Evidence From PakistanInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- 1106-Article Text-3172-4-10-20210519Document24 pages1106-Article Text-3172-4-10-20210519hoaintt0122No ratings yet

- The Influence of Financial Performance On Company Value With Capital Structure As A Mediation VariableDocument8 pagesThe Influence of Financial Performance On Company Value With Capital Structure As A Mediation VariableInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- The Effect of Dividend Policy, Liquidity, Profitability and Firm Size on Firm Value in Financial Service SectorDocument11 pagesThe Effect of Dividend Policy, Liquidity, Profitability and Firm Size on Firm Value in Financial Service SectorGufranNo ratings yet

- Jurnal Inggris LalaDocument12 pagesJurnal Inggris LalaRAFIF fadhlurrahmanNo ratings yet

- Capital Structure and Financial Performance Evidence From Listed Firms in The Oil and Gas Sector in NigeriaDocument8 pagesCapital Structure and Financial Performance Evidence From Listed Firms in The Oil and Gas Sector in NigeriaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Audit and Accounting Review (AAR) : Issn: 2790-8267 ISSN: 2790-8275 HomepageDocument24 pagesAudit and Accounting Review (AAR) : Issn: 2790-8267 ISSN: 2790-8275 HomepageAudit and Accounting ReviewNo ratings yet

- 891-Article Text-4801-5134-10-20220629Document25 pages891-Article Text-4801-5134-10-20220629Yosr TliliNo ratings yet

- The Mediating Effect of Debt Equity Ratio On The Effect of Current Ratio, Return On Equity and Total Asset Turnover On Price To Book ValueDocument16 pagesThe Mediating Effect of Debt Equity Ratio On The Effect of Current Ratio, Return On Equity and Total Asset Turnover On Price To Book ValueNovita DewiNo ratings yet

- Liquidity Profitability Trade Off A Panel Study of Listed Non Financial Firms in GhanaDocument14 pagesLiquidity Profitability Trade Off A Panel Study of Listed Non Financial Firms in GhanaEditor IJTSRDNo ratings yet

- Financial Ratio Interpretation (ITC)Document12 pagesFinancial Ratio Interpretation (ITC)Gorantla SindhujaNo ratings yet

- Fixed Asset Revaluation Decision MakingDocument7 pagesFixed Asset Revaluation Decision MakingYosr TliliNo ratings yet

- Stock Liquidity and Stock Returns The Moderating RDocument14 pagesStock Liquidity and Stock Returns The Moderating RMONIQ VSNo ratings yet

- Jurnal Pendukung 13 (LN)Document16 pagesJurnal Pendukung 13 (LN)Natanael PranataNo ratings yet

- 66-105-1-SM (1)Document9 pages66-105-1-SM (1)s3979517No ratings yet

- Ac 2020 118Document8 pagesAc 2020 118Phạm Bảo DuyNo ratings yet

- 1 PBDocument12 pages1 PBsainada osaNo ratings yet

- Manuscript Redy Et AlDocument7 pagesManuscript Redy Et Aldwi intan lestari 4220058No ratings yet

- Factors in Capital Structure and Its Influence On Total Debt Ratio of Automotive IndutryDocument8 pagesFactors in Capital Structure and Its Influence On Total Debt Ratio of Automotive IndutryVIORENSTIA NERYNo ratings yet

- Fundamental Analysis and Stock Returns: An Indian Evidence: Full Length Research PaperDocument7 pagesFundamental Analysis and Stock Returns: An Indian Evidence: Full Length Research PaperMohana SundaramNo ratings yet

- 478-Article Text-1844-1836-10-20231230Document20 pages478-Article Text-1844-1836-10-20231230erikNo ratings yet

- 145-Article Text-429-1-10-20210803Document12 pages145-Article Text-429-1-10-20210803(FPTU HCM) Phạm Anh Thiện TùngNo ratings yet

- The Impact of Capital Structure and Firm Size On Financial Performance of Commercial Banks in NepalDocument10 pagesThe Impact of Capital Structure and Firm Size On Financial Performance of Commercial Banks in NepalPushpa Shree PandeyNo ratings yet

- Jurnal Inter 4Document8 pagesJurnal Inter 4STEFFANINo ratings yet

- Financialconditionworkingcapitalpolicyandprofitability Emerald (1)Document38 pagesFinancialconditionworkingcapitalpolicyandprofitability Emerald (1)HkNo ratings yet

- Quantitative Analysis On Financial Performance of Merger and Acquisition of Indian CompaniesDocument6 pagesQuantitative Analysis On Financial Performance of Merger and Acquisition of Indian CompaniesPoonam KilaniyaNo ratings yet

- 2021 001 A Critical Assessment of Interrelationship Among CG, Financial Performance, Refined Economic VA To Firm ValueDocument42 pages2021 001 A Critical Assessment of Interrelationship Among CG, Financial Performance, Refined Economic VA To Firm ValueNidia Anggreni DasNo ratings yet

- Liquidity and Financial Performance A Correlational Analysis of Quoted Non Financial Firms in GhanaDocument11 pagesLiquidity and Financial Performance A Correlational Analysis of Quoted Non Financial Firms in GhanaEditor IJTSRDNo ratings yet

- Cost of Capital and Profitability Analysis (A Case Study of Telecommunication Industry)Document9 pagesCost of Capital and Profitability Analysis (A Case Study of Telecommunication Industry)Preet PreetNo ratings yet

- NI LUH 2021 Company Value Profitability ROADocument11 pagesNI LUH 2021 Company Value Profitability ROAFitra Ramadhana AsfriantoNo ratings yet

- Accounting: Corporate Governance and Firm PerformanceDocument10 pagesAccounting: Corporate Governance and Firm PerformanceKhả Ái ĐặngNo ratings yet

- Analysis of The Financial Performance of Processors and Glass Applications "Yoonly Glass"Document6 pagesAnalysis of The Financial Performance of Processors and Glass Applications "Yoonly Glass"aijbmNo ratings yet

- Jurnal Tesis - Edwin GunawanDocument10 pagesJurnal Tesis - Edwin GunawanEdwin GunawanNo ratings yet

- scipg,+Journal+manager,+JABFR 2020 9 (2) 50 56Document7 pagesscipg,+Journal+manager,+JABFR 2020 9 (2) 50 56Alamin Rahman JuwelNo ratings yet

- Journal Int 4Document6 pagesJournal Int 4Jeremia Duta PerdanakasihNo ratings yet

- Ijbel24.isu 6 910Document8 pagesIjbel24.isu 6 910BaekkichanNo ratings yet

- The Financial Ratios and Institutional Ownership Impact On Healthcare Firm's ValueDocument8 pagesThe Financial Ratios and Institutional Ownership Impact On Healthcare Firm's ValueInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Financial Statement Analysis As A Tool For Investment Decisions and Assessment of Companies' PerformanceDocument18 pagesFinancial Statement Analysis As A Tool For Investment Decisions and Assessment of Companies' PerformanceCinta Rizkia Zahra LubisNo ratings yet

- Key Financial Ratios Analysis For Manufacturing Companies - A Bibliometric AnalysisDocument17 pagesKey Financial Ratios Analysis For Manufacturing Companies - A Bibliometric AnalysisAhmadi AliNo ratings yet

- Profitability, Capital Structure, Managerial Ownership and Firm Value (Empirical Study of Manufacturing Companies in Indonesia 2016 - 2020)Document7 pagesProfitability, Capital Structure, Managerial Ownership and Firm Value (Empirical Study of Manufacturing Companies in Indonesia 2016 - 2020)International Journal of Innovative Science and Research TechnologyNo ratings yet

- Effect of Return On Assets and Asset Structure Against Debt To Equity Ratio Banking Companies On The Indonesia Stock ExchangeDocument3 pagesEffect of Return On Assets and Asset Structure Against Debt To Equity Ratio Banking Companies On The Indonesia Stock ExchangeInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Melpa Riani: Keywords:-Stock Prices, CR, DER, TATO, NPM, ROEDocument8 pagesMelpa Riani: Keywords:-Stock Prices, CR, DER, TATO, NPM, ROEInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Literature Review of The ImpacDocument23 pagesLiterature Review of The Impac155- Salsabila GadingNo ratings yet

- 65-Article Text-171-1-10-20200331Document6 pages65-Article Text-171-1-10-20200331mia muchia desdaNo ratings yet

- Complementarity of Equity and Debt Capital On Profitability of Quoted Consumer Goods Firms in NigeriaDocument11 pagesComplementarity of Equity and Debt Capital On Profitability of Quoted Consumer Goods Firms in NigeriaEditor IJTSRDNo ratings yet

- Analysis of Financial Performance of Plantation SubSector Companies Listed On The Indonesia StockDocument8 pagesAnalysis of Financial Performance of Plantation SubSector Companies Listed On The Indonesia StockInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Muhammad Khalis - 1901102010056 - Artikel MetopenDocument13 pagesMuhammad Khalis - 1901102010056 - Artikel MetopenMuhammad KhalisNo ratings yet

- Ijsred V2i1p36Document14 pagesIjsred V2i1p36IJSREDNo ratings yet

- SSRN Id3834213Document14 pagesSSRN Id3834213Ranveer kumarNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- Caso Carvajal S.A.Document22 pagesCaso Carvajal S.A.Indrenetk Leon100% (1)

- SW One DXP Cost Sheet (4.5BHK+Utility) Phase 2Document1 pageSW One DXP Cost Sheet (4.5BHK+Utility) Phase 2assetcafe7No ratings yet

- Communication Plan September 27Document24 pagesCommunication Plan September 27Rosemarie T. BrionesNo ratings yet

- Tata Tea - FADocument27 pagesTata Tea - FASagar BsNo ratings yet

- MRB Approves Nonconforming PartsDocument3 pagesMRB Approves Nonconforming PartsMiguel RodriguezNo ratings yet

- The Ultimate Guide to Achieving ISO 27001 CertificationDocument21 pagesThe Ultimate Guide to Achieving ISO 27001 CertificationTaraj O KNo ratings yet

- Samir Samuel Site Engineer 2021Document2 pagesSamir Samuel Site Engineer 2021Samir SamuelNo ratings yet

- Nabanita Das - Senior Integration (Software AG Webmethods) Consultant 03242023Document12 pagesNabanita Das - Senior Integration (Software AG Webmethods) Consultant 03242023vipul tiwariNo ratings yet

- PPM02 Project Portfolio Prioritization Matrix - AdvancedDocument5 pagesPPM02 Project Portfolio Prioritization Matrix - AdvancedHazqanNo ratings yet

- reading_sample_sap_press_reporting_with_sap_s4hanaDocument32 pagesreading_sample_sap_press_reporting_with_sap_s4hanaCharles SantosNo ratings yet

- K WaterDocument113 pagesK WaterAmri Rifki FauziNo ratings yet

- Training in Human Resource ManagementDocument21 pagesTraining in Human Resource ManagementAlok kumarNo ratings yet

- Jurnal Penelitian Dosen Fikom (UNDA) Vol.10 No.2, November 2019, ISSNDocument8 pagesJurnal Penelitian Dosen Fikom (UNDA) Vol.10 No.2, November 2019, ISSNkiki rifkiNo ratings yet

- Sample Paper Speaking BEC PreliminaryDocument2 pagesSample Paper Speaking BEC PreliminaryPham Van Khoa100% (1)

- Pre ProductionDocument2 pagesPre ProductionRajrupa SahaNo ratings yet

- Agile Development: © Lpu:: Cap437: Software Engineering Practices: Ashwani Kumar TewariDocument28 pagesAgile Development: © Lpu:: Cap437: Software Engineering Practices: Ashwani Kumar TewariAnanth KallamNo ratings yet

- 7 Eleven Store Nantun District - Google SearchDocument1 page7 Eleven Store Nantun District - Google SearchArleen MallillinNo ratings yet

- Terminate Utilities AccountDocument1 pageTerminate Utilities AccountVimal FranklinNo ratings yet

- GE Nine-Cell Planning Grid TechniqueDocument10 pagesGE Nine-Cell Planning Grid Techniquevarun rajNo ratings yet

- LABOR STANDARDS REVIEW MCQDocument5 pagesLABOR STANDARDS REVIEW MCQLiza MelgarNo ratings yet

- RBI's Vital Role in Regulating India's Economy and Financial SystemDocument2 pagesRBI's Vital Role in Regulating India's Economy and Financial SystemSimran hreraNo ratings yet

- Types of POS SystemsDocument3 pagesTypes of POS SystemsCabdulahi CumarNo ratings yet

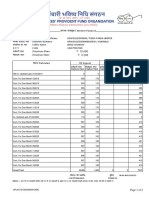

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Nasarawa Pre Qualified FacilitatorsDocument15 pagesNasarawa Pre Qualified FacilitatorsAzeez victorNo ratings yet

- Quotation - Householders - LAPSONDocument1 pageQuotation - Householders - LAPSONCredsureNo ratings yet

- CV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Document11 pagesCV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Agus NugrahaNo ratings yet

- Quiz Manajemen Pengadaan - Nisrina Zalfa Farida - 21B505041003Document5 pagesQuiz Manajemen Pengadaan - Nisrina Zalfa Farida - 21B505041003Kuro DitNo ratings yet