You might also like

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- Gross Income With Answer KeyDocument4 pagesGross Income With Answer KeyFallaria Paulo A.No ratings yet

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Income Taxation Exclusions and Gross IncomeDocument6 pagesIncome Taxation Exclusions and Gross IncomeJane TuazonNo ratings yet

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- PDF 2Document8 pagesPDF 2ronnelNo ratings yet

- 09.19.22 TaxationDocument3 pages09.19.22 TaxationLeizzamar BayadogNo ratings yet

- Gross Income Tax Exclusions and InclusionsDocument7 pagesGross Income Tax Exclusions and Inclusionsceline marasiganNo ratings yet

- Gross Income PDFDocument7 pagesGross Income PDFNikolai Danielovich100% (1)

- Gross Income With Answer Key PDF FreeDocument8 pagesGross Income With Answer Key PDF Freepaolo suaresNo ratings yet

- 87 07 Gross Income NotesDocument9 pages87 07 Gross Income NotesVianney Claire RabeNo ratings yet

- TAX-07-GROSS-INCOME (With Answers)Document12 pagesTAX-07-GROSS-INCOME (With Answers)Kendrew SujideNo ratings yet

- TAXATION (Gross IncomeDocument13 pagesTAXATION (Gross IncomeMarc CastilloNo ratings yet

- TAX EXCLUSIONS UNDER 40Document13 pagesTAX EXCLUSIONS UNDER 40Dea Lyn BaculaNo ratings yet

- Take Home Quiz Income TaxationDocument5 pagesTake Home Quiz Income TaxationMae Astoveza100% (3)

- Banana BBQ CPA Dentist Partnership Tax QuestionsDocument4 pagesBanana BBQ CPA Dentist Partnership Tax QuestionsBarbara IgnacioNo ratings yet

- No 3Document4 pagesNo 3Barbara IgnacioNo ratings yet

- Finals - I. Gross Income ProblemsDocument8 pagesFinals - I. Gross Income ProblemsJovince Daño DoceNo ratings yet

- 92-07 - Gross IncomeDocument10 pages92-07 - Gross IncomeaudreyNo ratings yet

- Taxable partnerships and income tax deductionsDocument4 pagesTaxable partnerships and income tax deductionsBarbara IgnacioNo ratings yet

- 91-07 Gross IncomeDocument8 pages91-07 Gross IncomeNova PogadoNo ratings yet

- Tax 1 - Quiz #6 - Gross Income (With Inclusions and Exclusions)Document5 pagesTax 1 - Quiz #6 - Gross Income (With Inclusions and Exclusions)Mary CuisonNo ratings yet

- Final Examination Income TaxDocument11 pagesFinal Examination Income TaxKristine Lumanaog100% (1)

- Exclusion from gross incomeDocument11 pagesExclusion from gross incomeMychie Lynne MayugaNo ratings yet

- TAX - Gross IncomeDocument7 pagesTAX - Gross IncomeThunder StickNo ratings yet

- Income Taxation Term Assessment 2 SEM SY 2019 - 2020: Coverage: Chapter 8 - 11Document4 pagesIncome Taxation Term Assessment 2 SEM SY 2019 - 2020: Coverage: Chapter 8 - 11Nhel AlvaroNo ratings yet

- Philippine Christian University: Income Taxation (Midterm Exam)Document5 pagesPhilippine Christian University: Income Taxation (Midterm Exam)Michael Brian Torres100% (1)

- Income Tax Semifinals ExamDocument5 pagesIncome Tax Semifinals ExamFeelingerang MAYoraNo ratings yet

- Taxation PDFDocument15 pagesTaxation PDFJaneNo ratings yet

- Usiness AW Axation: Easy RoundDocument5 pagesUsiness AW Axation: Easy RoundYllana GierNo ratings yet

- Usiness AW Axation: Easy RoundDocument5 pagesUsiness AW Axation: Easy RoundYllana GierNo ratings yet

- Tax CPAR Final Pre Board2Document4 pagesTax CPAR Final Pre Board2Khatneeze Ghem Buhente DulnuanNo ratings yet

- Final Examination in Income TaxationDocument6 pagesFinal Examination in Income TaxationJoyce Ann Cortez100% (2)

- Tax CPAR Final Pre Board2Document5 pagesTax CPAR Final Pre Board2Floyd delMundo100% (1)

- App III Summer Final ExamDocument7 pagesApp III Summer Final ExamCharmaine PamintuanNo ratings yet

- App III Summer Final ExamDocument7 pagesApp III Summer Final ExamPamela SantosNo ratings yet

- 025774085Document12 pages025774085Karla Cathrina FernandoNo ratings yet

- PALAWAN STATE UNIVERSITY MID-TERM EXAMDocument8 pagesPALAWAN STATE UNIVERSITY MID-TERM EXAMEppie SeverinoNo ratings yet

- Comprehensive Exam-Income TaxationDocument5 pagesComprehensive Exam-Income TaxationKaren May JimenezNo ratings yet

- CPA review school Philippines tax questionsDocument9 pagesCPA review school Philippines tax questionsNah HamzaNo ratings yet

- Chapter 3,4,5,6 (Income Tax)Document14 pagesChapter 3,4,5,6 (Income Tax)Txos Vaj50% (4)

- CHAPTER 8 (AutoRecovered)Document58 pagesCHAPTER 8 (AutoRecovered)Isabel MalicdanNo ratings yet

- This Study Resource Was: GROSS INCOME (Inclusions and Exclusions)Document3 pagesThis Study Resource Was: GROSS INCOME (Inclusions and Exclusions)Business MatterNo ratings yet

- Income Tax DeductionsDocument31 pagesIncome Tax DeductionsJane Tuazon50% (2)

- Multiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationDocument34 pagesMultiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationJay GalleroNo ratings yet

- ACC 311 Income Tax ReviewDocument6 pagesACC 311 Income Tax ReviewRussel Jay CardeñoNo ratings yet

- Multiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationDocument34 pagesMultiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationAngel May L. LopezNo ratings yet

- Tax On Ind-QuizDocument34 pagesTax On Ind-QuizKathleen Jane Solmayor100% (2)

- 06 Gross IncomeDocument23 pages06 Gross IncomeEloisa MonatoNo ratings yet

- Quiz 3 Taxation 111Document3 pagesQuiz 3 Taxation 111Sara Mae Albina-Dela CruzNo ratings yet

- Multiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationDocument34 pagesMultiple Choice Questions CPA Reviewer in Taxation Income Taxation of Individuals & CorporationTrixia SiribanNo ratings yet

- Income Taxation QuizzerDocument41 pagesIncome Taxation QuizzerMarriz Tan100% (4)

- Income Tax MCQDocument10 pagesIncome Tax MCQGlem Maquiling JosolNo ratings yet

- Tax QuizDocument8 pagesTax Quizcleofe janeNo ratings yet

- Taxation of Individuals QuizzerDocument37 pagesTaxation of Individuals QuizzerJc QuismundoNo ratings yet

- INCOME TAXATION OF INDIVIDUALS & CORPORATIONSDocument26 pagesINCOME TAXATION OF INDIVIDUALS & CORPORATIONSarkisha100% (1)

- Second PB Acctg 203BDocument12 pagesSecond PB Acctg 203BBella AyabNo ratings yet

- Taxation of Individuals QuizzerDocument38 pagesTaxation of Individuals Quizzerlorenceabad07No ratings yet

- Review Problems 1rDocument8 pagesReview Problems 1rYousefNo ratings yet

- Time Value of MoneyDocument1 pageTime Value of MoneyAlelie dela CruzNo ratings yet

- Question Paper For The Position: Audit & Accounts Officer TimeDocument2 pagesQuestion Paper For The Position: Audit & Accounts Officer TimeM A Fazal & Co.No ratings yet

- Match Each Definition With Its Related Term or Abbreviation byDocument2 pagesMatch Each Definition With Its Related Term or Abbreviation byHassan JanNo ratings yet

- Re: Bank of Baroda - Reviewed Standalone & Consolidated Financial Results - Q2 (FY2022-23) - Regulation 33 of SEBI (LODR) Regulations, 2015Document43 pagesRe: Bank of Baroda - Reviewed Standalone & Consolidated Financial Results - Q2 (FY2022-23) - Regulation 33 of SEBI (LODR) Regulations, 2015Mahesh DhalNo ratings yet

- Cash Flow Statement Presentation)Document12 pagesCash Flow Statement Presentation)Arun GuleriaNo ratings yet

- Q3 2021 - Investor LetterDocument2 pagesQ3 2021 - Investor LetterMessina04No ratings yet

- INtraday Trading Methods For NiftyDocument4 pagesINtraday Trading Methods For Niftymuddisetty umamaheswar100% (1)

- HDFC Bank Balance Sheet and Profit & Loss AnalysisDocument8 pagesHDFC Bank Balance Sheet and Profit & Loss AnalysisIshanviyaNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelSSSNIPDNo ratings yet

- Working Capital Project ReportDocument91 pagesWorking Capital Project ReportSupash AlawadiNo ratings yet

- Specialised Accouning Ques BankDocument31 pagesSpecialised Accouning Ques BankMayra AzharNo ratings yet

- Conceptual Framework: & Accounting StandardsDocument26 pagesConceptual Framework: & Accounting StandardsBritnys NimNo ratings yet

- Account Balance(s) As at 30 June 2023: Receiving Your Statements by Post?Document5 pagesAccount Balance(s) As at 30 June 2023: Receiving Your Statements by Post?abdizamed14No ratings yet

- Chapter One: Introduction: How Do Variable Life Insurance Policies Work?Document43 pagesChapter One: Introduction: How Do Variable Life Insurance Policies Work?exonyeoshidae 05No ratings yet

- Principles of AccountsDocument38 pagesPrinciples of AccountsRAMZAN TNo ratings yet

- Chapter01 Introduction To Commercial BanksDocument35 pagesChapter01 Introduction To Commercial BanksĐoàn Trần Ngọc AnhNo ratings yet

- FM CH 07 PDFDocument72 pagesFM CH 07 PDFLayatmika SahooNo ratings yet

- CFAB - Accounting - QB - Chapter 12Document13 pagesCFAB - Accounting - QB - Chapter 12Huy NguyenNo ratings yet

- Strategic Disinvestment ProcessDocument35 pagesStrategic Disinvestment ProcesstomsraoNo ratings yet

- List of Approved Vietnamese Sending Organization - Moc: Sending Tits "Care Worker"Document248 pagesList of Approved Vietnamese Sending Organization - Moc: Sending Tits "Care Worker"tamchau nguyenngocNo ratings yet

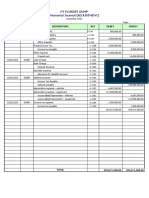

- PT Florist Gump December 2020 Financial StatementDocument9 pagesPT Florist Gump December 2020 Financial StatementSu MiniNo ratings yet

- 11 Stock Valuation and RiskDocument44 pages11 Stock Valuation and RiskPaula Ella BatasNo ratings yet

- Effective Management of Small BusinessDocument21 pagesEffective Management of Small Businessmurugesh_mbahit100% (2)

- CPAR TOA Pre-Board FinalDocument10 pagesCPAR TOA Pre-Board FinalJericho Pedragosa100% (1)

- Statement of Income: P&L Account Can Also Be Named AsDocument5 pagesStatement of Income: P&L Account Can Also Be Named Asanand sanilNo ratings yet

- FAR 4320 Book Value Per Share Earnings Per Share PDFDocument3 pagesFAR 4320 Book Value Per Share Earnings Per Share PDFAnjolina BautistaNo ratings yet

- Cost of Debt Calculations PDFDocument2 pagesCost of Debt Calculations PDFhukaNo ratings yet

- StatementsDocument5 pagesStatementsAdeelNo ratings yet

- Douglas KinghornDocument24 pagesDouglas KinghornAnonymous 3DG7N5No ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Streetsmart Financial Basics for Nonprofit Managers: 4th EditionFrom EverandStreetsmart Financial Basics for Nonprofit Managers: 4th EditionRating: 3.5 out of 5 stars3.5/5 (3)

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Other People's Money: The Real Business of FinanceFrom EverandOther People's Money: The Real Business of FinanceRating: 4 out of 5 stars4/5 (34)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)