You might also like

- International BankingDocument9 pagesInternational Bankingshahd naserNo ratings yet

- What Is The Relationship Between Informal Financial Sector and Formal Financial SectorDocument13 pagesWhat Is The Relationship Between Informal Financial Sector and Formal Financial Sectoradedejigabriel894No ratings yet

- Solution Manual For Bank Management 7th Edition by Koch Complete Downloadable File atDocument7 pagesSolution Manual For Bank Management 7th Edition by Koch Complete Downloadable File atNguyễn Minh PhươngNo ratings yet

- Intro To Formal and Informal FinancialDocument11 pagesIntro To Formal and Informal Financialadedejigabriel894No ratings yet

- Banking Law - Mid-Term ExaminationDocument8 pagesBanking Law - Mid-Term ExaminationM.Zaigham RazaNo ratings yet

- Commercial Banking System and Role of RBI PG QP JUNE 2024 PDFDocument4 pagesCommercial Banking System and Role of RBI PG QP JUNE 2024 PDFBalamuralikrishna YadavNo ratings yet

- Bank Management Koch 8th Edition Solutions ManualDocument8 pagesBank Management Koch 8th Edition Solutions ManualAnna Young100% (24)

- Management of Financial InstitutionDocument14 pagesManagement of Financial InstitutionShailesh SapariyaNo ratings yet

- Porter Five Forces On Banking, Finance IndustryDocument3 pagesPorter Five Forces On Banking, Finance Industryavinash singh71% (7)

- CSCF T7 - P23Document23 pagesCSCF T7 - P23sk2p7tsf5cNo ratings yet

- Care Report - Case 8.WIPDocument2 pagesCare Report - Case 8.WIPHeng RyanNo ratings yet

- ComplexitiesDocument2 pagesComplexitiesHassan AliNo ratings yet

- Lesson 10 Expanding The Boundaries of BankingDocument29 pagesLesson 10 Expanding The Boundaries of Bankingshai291321No ratings yet

- Group Work A.docx 2135Document20 pagesGroup Work A.docx 2135Addaa WondimeNo ratings yet

- Bank Management Koch 8th Edition Solutions ManualDocument8 pagesBank Management Koch 8th Edition Solutions Manualmeghantaylorxzfyijkotm100% (48)

- Bank Management Koch 8th Edition Solutions ManualDocument36 pagesBank Management Koch 8th Edition Solutions Manualcaroteel.buyer.b8rg100% (45)

- Direct Lending: Benefits, Risks and Opportunities: OaktreeDocument13 pagesDirect Lending: Benefits, Risks and Opportunities: OaktreeIshan ShuklaNo ratings yet

- Challenges & Opportunities - Banking Reforms in IndiaDocument5 pagesChallenges & Opportunities - Banking Reforms in IndiaJAGRITI SINGHNo ratings yet

- Universal BankingDocument25 pagesUniversal BankingRahul SethNo ratings yet

- Assignment On NBFI Sector in BangladeshDocument10 pagesAssignment On NBFI Sector in BangladeshFarhan Ashraf SaadNo ratings yet

- Chapter Five Regulation of Financial SystemDocument41 pagesChapter Five Regulation of Financial SystemAbdiNo ratings yet

- Universal Banking: Prepared By: Priyanka Khandelwal PG20095094Document10 pagesUniversal Banking: Prepared By: Priyanka Khandelwal PG20095094Priyanka KhandelwalNo ratings yet

- DocumentDocument12 pagesDocumenttyagimegha309No ratings yet

- MCM Tutorial 2Document3 pagesMCM Tutorial 2SHU WAN TEHNo ratings yet

- Week 1 Practice Questions Solution-2Document5 pagesWeek 1 Practice Questions Solution-2Caroline FrisciliaNo ratings yet

- Rural Banking and Financial Inclusion Reflection Memo # 3 Shivani Tannu, 1811439Document2 pagesRural Banking and Financial Inclusion Reflection Memo # 3 Shivani Tannu, 1811439Harshal WankhedeNo ratings yet

- CH 1 An Overview of The Financial System (Part 1A)Document32 pagesCH 1 An Overview of The Financial System (Part 1A)Sherif ElSheemyNo ratings yet

- Mixed Banking:: System Refers To That Banking System Under Which TheDocument7 pagesMixed Banking:: System Refers To That Banking System Under Which TheLOKESH RAMNo ratings yet

- Chapter 8Document4 pagesChapter 8John FrandoligNo ratings yet

- Director AssignmentDocument16 pagesDirector AssignmentUma VermaNo ratings yet

- Universal BankingDocument30 pagesUniversal Bankingdarshan71219892205100% (1)

- Commercial Banking Structure, Regulation and PerformanceDocument21 pagesCommercial Banking Structure, Regulation and PerformanceJhilik PradhanNo ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter ThreeDocument3 pagesSolutions For End-of-Chapter Questions and Problems: Chapter Threejl123123No ratings yet

- Unit 4 Management of Risk in Financial Services: ObjectivesDocument23 pagesUnit 4 Management of Risk in Financial Services: ObjectivesSHYAM GOELNo ratings yet

- XI. Summary On Finance For Small Borrowers: Microcredits and Internal MarketsDocument2 pagesXI. Summary On Finance For Small Borrowers: Microcredits and Internal MarketsKirsty Jane DilleraNo ratings yet

- Factors Affecting Bank Credit in India: 6.1 Principles of LendingDocument18 pagesFactors Affecting Bank Credit in India: 6.1 Principles of LendingTalha A SiddiquiNo ratings yet

- Financial Institutions Management - Solutions - Chap001Document10 pagesFinancial Institutions Management - Solutions - Chap001Samra AfzalNo ratings yet

- Credit MarketDocument64 pagesCredit MarketNiket DattaniNo ratings yet

- FIN2339 CH8-An Economic Analysis of Financial StructureDocument9 pagesFIN2339 CH8-An Economic Analysis of Financial StructureJasleen GillNo ratings yet

- Case 6 MicrofinanceDocument2 pagesCase 6 MicrofinanceJean Xandra Sabud Veloso100% (1)

- 3 Bank Based vs. Market BasedDocument9 pages3 Bank Based vs. Market BasedLinh TranNo ratings yet

- Finance CompanyDocument3 pagesFinance CompanyNhi HoangNo ratings yet

- Chapter Four: Regulating The Financial SystemDocument43 pagesChapter Four: Regulating The Financial SystemYismawNo ratings yet

- A Case StudyDocument10 pagesA Case StudyAvila SimonNo ratings yet

- Chapter Five 5) Financial Market Regulation: Regulatory StandardsDocument6 pagesChapter Five 5) Financial Market Regulation: Regulatory StandardsSeid KassawNo ratings yet

- Managing The Lending Portfolio of BanksDocument44 pagesManaging The Lending Portfolio of BanksgurudumaNo ratings yet

- Project Report On Indian Banking Sector and Barclays: Submitted To: Pranav Sir Submitted By: Lalit Tiwari (DM10B19Document25 pagesProject Report On Indian Banking Sector and Barclays: Submitted To: Pranav Sir Submitted By: Lalit Tiwari (DM10B19lit143No ratings yet

- Corporate Finace LawDocument11 pagesCorporate Finace LawRamNo ratings yet

- Savings: Role of The Financial System in Economic DevelopmentDocument6 pagesSavings: Role of The Financial System in Economic DevelopmentMurari NayuduNo ratings yet

- Prospects and Problems of Bond MarketDocument12 pagesProspects and Problems of Bond MarketMoushumi Sarker0% (1)

- Bab 1 FRMDocument11 pagesBab 1 FRMartaninditaNo ratings yet

- Acknowledgement: Sunil Kumar Tyagi Under Whose Guidance and Supervision Project ReportDocument75 pagesAcknowledgement: Sunil Kumar Tyagi Under Whose Guidance and Supervision Project Reportsheery_ank007899No ratings yet

- A Manual On Non Banking Financial Institutions: 9. Anti Money Laundering StandardsDocument143 pagesA Manual On Non Banking Financial Institutions: 9. Anti Money Laundering StandardsRahul JagwaniNo ratings yet

- Non-Bank Financial InstitutionsDocument11 pagesNon-Bank Financial InstitutionsCristineNo ratings yet

- Assignment Banking-1Document8 pagesAssignment Banking-1Al RafiNo ratings yet

- Unclaimed Benefits NorthwestDocument45 pagesUnclaimed Benefits NorthwestBenny MoingotliNo ratings yet

- Tranzact Insurance 7-06Document1 pageTranzact Insurance 7-06julissaNo ratings yet

- MPL FLEX Application Form2Document3 pagesMPL FLEX Application Form2emmanuel cantones, jr.No ratings yet

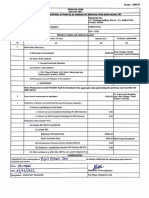

- Form 12BBDocument1 pageForm 12BBBiranchi DasNo ratings yet

- Eng'g Econ ProbsetDocument1 pageEng'g Econ ProbsetJiever AustriaNo ratings yet

- Public Speech. The Importance of Financial Literacy in SchoolsDocument2 pagesPublic Speech. The Importance of Financial Literacy in SchoolsSaule Janonyte100% (1)

- APR, EAR and Period Rates - ExplainedDocument2 pagesAPR, EAR and Period Rates - ExplainedblazeNo ratings yet

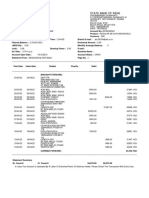

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancerashikaNo ratings yet

- Image 2Document20 pagesImage 2Ramesh chand MeenaNo ratings yet

- Statement 20221101 20221129Document7 pagesStatement 20221101 20221129Chan PhengNo ratings yet

- Chase Bank Statement Template (1) 2 - PDF - Cheque - Deposit AccountDocument1 pageChase Bank Statement Template (1) 2 - PDF - Cheque - Deposit AccountworldwidelpcleNo ratings yet

- Can We Claim HRA and Home LoanDocument5 pagesCan We Claim HRA and Home LoanBipin PatilNo ratings yet

- STATEMENT Format SviDocument4 pagesSTATEMENT Format SviSUMIT SAHANo ratings yet

- PDF Document - BankwestDocument1 pagePDF Document - Bankwestsattazee1992No ratings yet

- Credit ReportDocument19 pagesCredit ReportJaimee Tepper100% (3)

- Ino-RacunDocument1 pageIno-RacunNikšićko TamnoNo ratings yet

- FC 1285Document1 pageFC 1285Dostogir sarkarNo ratings yet

- Credit Cards PresentationDocument9 pagesCredit Cards PresentationSonu GiriNo ratings yet

- A G R E E M E N T - Heirs of Hernandez & Joel YaoDocument3 pagesA G R E E M E N T - Heirs of Hernandez & Joel Yaomarietta calladaNo ratings yet

- FM ReportDocument2 pagesFM Reportcaiden dumpNo ratings yet

- Module 1Document2 pagesModule 1Unknown Engr.No ratings yet

- AnnuityDocument42 pagesAnnuityJeus ManaloNo ratings yet

- e-StatementBRImo 606001040066533 Jan2024 20240111 180339Document2 pagese-StatementBRImo 606001040066533 Jan2024 20240111 180339GEN RLNo ratings yet

- Evaluating Consumer LoanDocument80 pagesEvaluating Consumer LoanNadiaNo ratings yet

- 6.accounting For DebenturesDocument22 pages6.accounting For Debenturestripatjotkaur757No ratings yet

- StatementDocument5 pagesStatementpese022No ratings yet

- Yes First Eclectic Debit Card SocDocument2 pagesYes First Eclectic Debit Card Socraghav mehraNo ratings yet

- DMI0037803259 Final Delivery OrderDocument2 pagesDMI0037803259 Final Delivery OrderRahul PramanikNo ratings yet

- SOA WineDocument2 pagesSOA WinePharmastar Int'l Trading Corp.No ratings yet

- Simple Loan Calculator: Loan Values Loan SummaryDocument11 pagesSimple Loan Calculator: Loan Values Loan Summarypile raftNo ratings yet