You might also like

- Spending Habits Among Malaysian UniversiDocument21 pagesSpending Habits Among Malaysian UniversiNajmi Sidik100% (1)

- Final Research ProposalDocument9 pagesFinal Research ProposalSunil Rawat100% (1)

- Financial Literacy Among The Millennial Generation - RelationshipsDocument16 pagesFinancial Literacy Among The Millennial Generation - RelationshipsYuslia Nandha Anasta SariNo ratings yet

- Financial LiteracyDocument39 pagesFinancial Literacyahire.krutika100% (2)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument33 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceamika goyalNo ratings yet

- INTRODUCTIONDocument12 pagesINTRODUCTIONDevika DasNo ratings yet

- Scenario Analysis, Stress and Reverse Stress TestingDocument19 pagesScenario Analysis, Stress and Reverse Stress TestingIRM IndiaNo ratings yet

- Theoretical FrameworkDocument7 pagesTheoretical Frameworkranny began100% (1)

- Final ReportDocument36 pagesFinal ReportNor Syahirah MohamadNo ratings yet

- Form 16 Fy 19 20 Part BDocument3 pagesForm 16 Fy 19 20 Part BMilind MoreNo ratings yet

- Study 3Document24 pagesStudy 3Angelika PanilagNo ratings yet

- RM Ag9 SybbajDocument32 pagesRM Ag9 Sybbajtrisha sinhaNo ratings yet

- RM Assignment 1 8 SYBBA Div D-1Document8 pagesRM Assignment 1 8 SYBBA Div D-1NAMYA ARORANo ratings yet

- BRM ReportDocument31 pagesBRM ReporthannNo ratings yet

- Research Proposal Key WordsDocument4 pagesResearch Proposal Key WordsLorainne ParungaoNo ratings yet

- IntroductionDocument50 pagesIntroductionjbum93257No ratings yet

- Mba SYNOPSISDocument9 pagesMba SYNOPSIShimanshu kumarNo ratings yet

- Financial Literacy of Public School Teachers in City of KoronadalDocument11 pagesFinancial Literacy of Public School Teachers in City of KoronadalJan Dave OgatisNo ratings yet

- Local Media1683093690696683162Document24 pagesLocal Media1683093690696683162fearl evangelistaNo ratings yet

- Course: Business Research MethodsDocument9 pagesCourse: Business Research MethodsBhuvnesh KumawatNo ratings yet

- Financial Behavior Amongst Undergraduate Students With and Without Financial Education: A Case Among University Malaysia Sabah UndergradesDocument15 pagesFinancial Behavior Amongst Undergraduate Students With and Without Financial Education: A Case Among University Malaysia Sabah UndergradesNajmi AimanNo ratings yet

- 4.0 Objectives of The StudyDocument2 pages4.0 Objectives of The StudyNor Syahirah MohamadNo ratings yet

- Saving Behavior in Generation ZDocument10 pagesSaving Behavior in Generation ZJanssen Sugiarto100% (1)

- Imron+Nur+Khusaini 5057-5068Document12 pagesImron+Nur+Khusaini 5057-5068ebdscholarship2023No ratings yet

- Research Concept Note-1Document2 pagesResearch Concept Note-1Fadhil ChiwangaNo ratings yet

- Learning Finance, Financial Literacy and Financial Technology As Predictors of Student Financial Behavior in The Covid-19 Pandemic EraDocument7 pagesLearning Finance, Financial Literacy and Financial Technology As Predictors of Student Financial Behavior in The Covid-19 Pandemic EraGabbie RevoñaNo ratings yet

- Research SummaryDocument4 pagesResearch SummaryChristian Clyde Zacal ChingNo ratings yet

- Article OnDocument11 pagesArticle OnBala subramanianNo ratings yet

- The Effect of Financial LiteracyDocument17 pagesThe Effect of Financial Literacynoorzia341No ratings yet

- Chap 1&2 Gram IDocument9 pagesChap 1&2 Gram IHenja PearlNo ratings yet

- Financila Literacy Amoung The Sellf Finance Group Mini Project ReportDocument31 pagesFinancila Literacy Amoung The Sellf Finance Group Mini Project ReportaccounitngNo ratings yet

- San Mateo Senior High School: The Problem and Its BackgroundDocument39 pagesSan Mateo Senior High School: The Problem and Its BackgroundAljhon PanganibanNo ratings yet

- Colleage ProjectDocument29 pagesColleage ProjectBusiness ManNo ratings yet

- Research PaperDocument4 pagesResearch Paperneelashi maruNo ratings yet

- Traya Et Al. 2023.docx 2Document14 pagesTraya Et Al. 2023.docx 2Felmer ReforsadoNo ratings yet

- According To Rafi DRAFTDocument11 pagesAccording To Rafi DRAFTRogemae LorenNo ratings yet

- Journal (Jaya College) - Investment Awareness of Working Women Investors in Chennai CityDocument12 pagesJournal (Jaya College) - Investment Awareness of Working Women Investors in Chennai CityMythili Karthikeyan100% (1)

- A Survey On Financial Literacy Among Young Professionals of Bogo CityDocument37 pagesA Survey On Financial Literacy Among Young Professionals of Bogo CityRenz LephoenixNo ratings yet

- Impact of Financial Literacy On Investment Decision of Working WomenDocument13 pagesImpact of Financial Literacy On Investment Decision of Working WomenRITESH SHINDENo ratings yet

- Determinants of Financial Literacy in The PhilippinesDocument31 pagesDeterminants of Financial Literacy in The PhilippinesMae MinggoyNo ratings yet

- Financial LiteracyDocument10 pagesFinancial LiteracyBehroozNo ratings yet

- DocumentDocument13 pagesDocumentjaziljazi99No ratings yet

- Chapter 1Document7 pagesChapter 1ALZIE CYRHILLE PLENONo ratings yet

- A Correlation Study: Demographic Profile and Individual Financial Performance of Working Students in Stratford International SchoolDocument13 pagesA Correlation Study: Demographic Profile and Individual Financial Performance of Working Students in Stratford International SchoolWILLIAM III ZEALORNo ratings yet

- ProjectDocument5 pagesProjectvarunrajmanchala18No ratings yet

- Microsoft Word - A Survey On Financial Literacy Among Young Professionals of Bogo City PDFDocument37 pagesMicrosoft Word - A Survey On Financial Literacy Among Young Professionals of Bogo City PDFRenz LephoenixNo ratings yet

- Inquires Investigation and Immersion - PresentationDocument30 pagesInquires Investigation and Immersion - PresentationerikjohnpabuaNo ratings yet

- Jurnal MK 2Document6 pagesJurnal MK 2Clarissa Duika AugustaNo ratings yet

- Relationship Between Financial Literacy and Investment Behavior of Salaried IndividualsDocument7 pagesRelationship Between Financial Literacy and Investment Behavior of Salaried IndividualsBala VigneshNo ratings yet

- The Influence of Socio-Demographic and Financial Knowledge Factors On Financial Management Practices of MalaysiansDocument18 pagesThe Influence of Socio-Demographic and Financial Knowledge Factors On Financial Management Practices of MalaysiansMary AngelieNo ratings yet

- Nonchalant SDocument16 pagesNonchalant SPinky Dela Cruz AballeNo ratings yet

- Financial Literacy in Nepal: A Survey Analysis From College StudentsDocument27 pagesFinancial Literacy in Nepal: A Survey Analysis From College StudentsKersten BarnedoNo ratings yet

- Study 3Document24 pagesStudy 3Kaye Jay EnriquezNo ratings yet

- Chapter - 3 Research MethodologyDocument11 pagesChapter - 3 Research Methodologynagsen thokeNo ratings yet

- Study On Financial Literacy Among StudentsDocument8 pagesStudy On Financial Literacy Among StudentsFaisalNo ratings yet

- Cess RRLDocument2 pagesCess RRLPrincess Regidor100% (1)

- Financial LiteracyDocument6 pagesFinancial LiteracykousikpaikNo ratings yet

- Life Plan As Investment Option of Young Adult Senior High School Teachers in Silang CaviteDocument9 pagesLife Plan As Investment Option of Young Adult Senior High School Teachers in Silang CaviteJenine SipaganNo ratings yet

- RRL (Foreign Literature)Document6 pagesRRL (Foreign Literature)Joy QuitorianoNo ratings yet

- Learning to Manage Money: Financial Education from Childhood to Adolescence. Teaching Your Children to Save, Spend, and Invest WiselyFrom EverandLearning to Manage Money: Financial Education from Childhood to Adolescence. Teaching Your Children to Save, Spend, and Invest WiselyNo ratings yet

- "Man-Up" Institute Guide: Motivating Attitudes That Nurture an Understanding of Your PotentialFrom Everand"Man-Up" Institute Guide: Motivating Attitudes That Nurture an Understanding of Your PotentialNo ratings yet

- Auditing Problem Assignment Lyeca JoieDocument12 pagesAuditing Problem Assignment Lyeca JoieEsse ValdezNo ratings yet

- HSBC Vs Sps Galang, GR 199565, June 30, 2021Document16 pagesHSBC Vs Sps Galang, GR 199565, June 30, 2021Catherine DimailigNo ratings yet

- 11 & 12 Economics Split-UpDocument9 pages11 & 12 Economics Split-UpMadhuryaNo ratings yet

- Nefas Silk Poly Technic College: Learning GuideDocument43 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuNo ratings yet

- Accpd9629e 2023Document5 pagesAccpd9629e 2023wordsinditeNo ratings yet

- Entrepreneurship DevelopmentDocument26 pagesEntrepreneurship DevelopmentAkanksha NalawadeNo ratings yet

- Addis Ababa Universityschool of Graduate StudiesDocument15 pagesAddis Ababa Universityschool of Graduate StudiesEdlawit AwegchewNo ratings yet

- Company Profile and Project Status Reporting Form For Consultant: SupervisionDocument18 pagesCompany Profile and Project Status Reporting Form For Consultant: SupervisionAbaa MacaaNo ratings yet

- IMS Proschool IFRS EbookDocument143 pagesIMS Proschool IFRS EbookhariinshrNo ratings yet

- Factories of The FutureDocument3 pagesFactories of The FutureKonstantina DumitruNo ratings yet

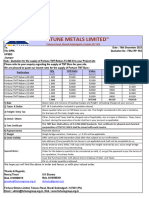

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Document1 page"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaNo ratings yet

- Ogilvy - Social CRM AnalysisDocument49 pagesOgilvy - Social CRM AnalysisFlorin BucaNo ratings yet

- Doctrine of MarshallingDocument4 pagesDoctrine of MarshallingchitraNo ratings yet

- Chapter 16 2021Document2 pagesChapter 16 2021Rabie HarounNo ratings yet

- Diagnostic ExamDocument22 pagesDiagnostic ExamCid DaclesNo ratings yet

- A Study of Bachat Gat & Women Empowerment in Nagpur City: October 2019Document5 pagesA Study of Bachat Gat & Women Empowerment in Nagpur City: October 2019Chaitali VartheNo ratings yet

- Interest Rates and Currency SwapsDocument24 pagesInterest Rates and Currency SwapsQuoc AnhNo ratings yet

- Transactions List: Ciprian-Nicolae Frigioi RO27BRDE180SV70010251800 RON Ciprian-Nicolae FrigioiDocument3 pagesTransactions List: Ciprian-Nicolae Frigioi RO27BRDE180SV70010251800 RON Ciprian-Nicolae FrigioiCiprian FrigioiNo ratings yet

- Chapter 5 InvestmentDocument49 pagesChapter 5 InvestmentmeenNo ratings yet

- New RHFL Schemes & Forms - May 2022Document36 pagesNew RHFL Schemes & Forms - May 2022Surya PmlNo ratings yet

- APISWA Report 280923 DigitalDocument31 pagesAPISWA Report 280923 DigitaldashaNo ratings yet

- IBO 1 - 10yearsDocument37 pagesIBO 1 - 10yearsManuNo ratings yet

- Baye Janson Unit 1 Part 1Document28 pagesBaye Janson Unit 1 Part 1Sudhanshu Sharma bchd21No ratings yet

- Wardian BrochureDocument79 pagesWardian Brochurerudy_wadhera4933No ratings yet

- Cash Oriented Business ActivitiesDocument5 pagesCash Oriented Business ActivitiesVenus AreolaNo ratings yet

- Reporting Sec. 900-913Document17 pagesReporting Sec. 900-913CLARK LOUISE PALOMARESNo ratings yet

- SMFBPO101 005 BPO-Operations-Management Slide-Deck 01062013 012-VerDocument54 pagesSMFBPO101 005 BPO-Operations-Management Slide-Deck 01062013 012-VerYumi ChangNo ratings yet