You might also like

- Internship Report On Soneri Bank LimitedDocument78 pagesInternship Report On Soneri Bank LimitedZubair Khan50% (2)

- DRAT Appeal DraftDocument10 pagesDRAT Appeal Draftadvsaurabhmandlik100% (1)

- Closing Bank Account LetterDocument1 pageClosing Bank Account Letterriddleridden78% (23)

- Asterisk-Free Checking Account Account: - 7392: Brad Sergi 3819 Plane Tree DR W COLUMBUS OH 43228-3560Document2 pagesAsterisk-Free Checking Account Account: - 7392: Brad Sergi 3819 Plane Tree DR W COLUMBUS OH 43228-3560Glenda0% (1)

- FICO Credit ScoreDocument4 pagesFICO Credit ScoreCarol100% (1)

- Handover NotesDocument4 pagesHandover NotesYAKUBU BABA TIJANINo ratings yet

- WS For GuarantorDocument36 pagesWS For GuarantorBunny AnandNo ratings yet

- CMM Mumbai section 14 SARFAESI ORDER VS Pappu MalikDocument5 pagesCMM Mumbai section 14 SARFAESI ORDER VS Pappu MalikbharatlegaltechNo ratings yet

- LawFinder 2067895 PDFDocument4 pagesLawFinder 2067895 PDFSyed FaisalNo ratings yet

- CRL.R.P.No.1053/2014 C/W CRL.R.P.No.1052/2014 Between:: Case Citation: (2023) Ibclaw - in 196 HCDocument27 pagesCRL.R.P.No.1053/2014 C/W CRL.R.P.No.1052/2014 Between:: Case Citation: (2023) Ibclaw - in 196 HCBarira ParvezNo ratings yet

- Display PDF - PHPDocument8 pagesDisplay PDF - PHPshraddhaahir1998No ratings yet

- Vimal Chandra Grover Vs Bank of India 26042000 SC0906s000514COM80164Document10 pagesVimal Chandra Grover Vs Bank of India 26042000 SC0906s000514COM80164Rocking MeNo ratings yet

- Gujarat HC Mortgage 426294Document15 pagesGujarat HC Mortgage 426294vaishnaviNo ratings yet

- Chembeti Brahmaiah Chowdary Vs The State Bank of Hyderabad Rep. ... On 13 April, 2010Document4 pagesChembeti Brahmaiah Chowdary Vs The State Bank of Hyderabad Rep. ... On 13 April, 2010marxman001No ratings yet

- Bank EMD Forfeiture ChallengedDocument9 pagesBank EMD Forfeiture ChallengedBhanushree JainNo ratings yet

- Vayam Tech Vs HPDocument7 pagesVayam Tech Vs HPThankamKrishnanNo ratings yet

- High Court of Judicature For Rajasthan Bench at Jaipur: (Downloaded On 14/04/2021 at 09:16:33 PM)Document8 pagesHigh Court of Judicature For Rajasthan Bench at Jaipur: (Downloaded On 14/04/2021 at 09:16:33 PM)ApoorvnujsNo ratings yet

- L&T FinanceDocument17 pagesL&T FinanceSandeep KhuranaNo ratings yet

- jkl-hc-cpc-444148hahaDocument11 pagesjkl-hc-cpc-444148hahaqasimnasir699No ratings yet

- ALM MootDocument12 pagesALM MootGENERAL SECRETARYNo ratings yet

- Supreme Court case on bank negligence and surety dischargeDocument14 pagesSupreme Court case on bank negligence and surety dischargeRam Kumar YadavNo ratings yet

- Test 8 (1)Document5 pagesTest 8 (1)KONINIKA BHATTACHARJEE 1950350No ratings yet

- Delhi HC JudgmentDocument6 pagesDelhi HC JudgmentKaranKrNo ratings yet

- Kailash Art International Vs Central Bank of India - AspxDocument56 pagesKailash Art International Vs Central Bank of India - AspxanillegalmailsNo ratings yet

- b'B.Shanmugam Vs Union Bank of India On 19 December, 2007'Document14 pagesb'B.Shanmugam Vs Union Bank of India On 19 December, 2007'Bruce AlmightyNo ratings yet

- DRT DRAFT Case 1Document14 pagesDRT DRAFT Case 1Dvs Suraj100% (1)

- Civil Case 4Document11 pagesCivil Case 4Amy CharlesNo ratings yet

- Supreme Court Judgment on Limitation Period for IBC PetitionsDocument73 pagesSupreme Court Judgment on Limitation Period for IBC PetitionsAnirudh PNo ratings yet

- Written Statement of Defences 10.06Document28 pagesWritten Statement of Defences 10.06Bunny AnandNo ratings yet

- 2022 8 1505 47486 Judgement 09-Oct-2023Document37 pages2022 8 1505 47486 Judgement 09-Oct-2023shivaayshaluNo ratings yet

- Jayant JulkaDocument36 pagesJayant JulkaAmit GoelNo ratings yet

- DPC Assignment - 1 SuitsDocument51 pagesDPC Assignment - 1 SuitsAKHILA.SURESHNo ratings yet

- Mascot DRAT 2020 - para 15 and 19 Communications Convey That Possession Is TakenDocument5 pagesMascot DRAT 2020 - para 15 and 19 Communications Convey That Possession Is TakenPival K. PeddireddiNo ratings yet

- Vasu P. Shetty v. Hotel Vandana Palace & OrsDocument26 pagesVasu P. Shetty v. Hotel Vandana Palace & OrsSuraj AgarwalNo ratings yet

- 2018 9 1501 21186 Judgement 28-Feb-2020Document28 pages2018 9 1501 21186 Judgement 28-Feb-2020HunnuNo ratings yet

- Chemstar Organics v. Bank of BarodaDocument20 pagesChemstar Organics v. Bank of BarodaNikhil HansNo ratings yet

- State Bank of India Vs Premco Saw Mill Ahmedabad Ag840068COM216139Document6 pagesState Bank of India Vs Premco Saw Mill Ahmedabad Ag840068COM216139Aastha PatelNo ratings yet

- Bank Loan Recovery CaseDocument9 pagesBank Loan Recovery CaseSanjukta MajumdarNo ratings yet

- Plaint FormatDocument12 pagesPlaint FormatanmolNo ratings yet

- Signature Not VerifiedDocument19 pagesSignature Not VerifiedChandra Sekhar Kakarla100% (1)

- Union of India v. Rccivl-Litl (JV), 2022 SCC Online Del 4340Document11 pagesUnion of India v. Rccivl-Litl (JV), 2022 SCC Online Del 4340saket bansalNo ratings yet

- Prestige Lights LTD Vs State Bank of India 2008200S070902COM979683Document11 pagesPrestige Lights LTD Vs State Bank of India 2008200S070902COM979683Deon FernandesNo ratings yet

- J. Bhuyyan Dr. Subir Bannerjee vs. Neetu SinghDocument3 pagesJ. Bhuyyan Dr. Subir Bannerjee vs. Neetu SinghSangram ChinnappaNo ratings yet

- Bank ordered to release gratuity paymentDocument15 pagesBank ordered to release gratuity paymentsumitkejriwalNo ratings yet

- MischiefDocument9 pagesMischiefRahulNo ratings yet

- Bank recovery proceedings against guarantors can continue despite moratorium under IBCDocument29 pagesBank recovery proceedings against guarantors can continue despite moratorium under IBCChristina ShajuNo ratings yet

- DRT 501373Document26 pagesDRT 501373Prasad VaidyaNo ratings yet

- Writ Court Cannot Examine Transactions Between Borrower and BankDocument20 pagesWrit Court Cannot Examine Transactions Between Borrower and BankTrivikram Chitturu100% (1)

- 2022 Livelaw (SC) 496: in The Supreme Court of IndiaDocument9 pages2022 Livelaw (SC) 496: in The Supreme Court of IndiaKailash KhaliNo ratings yet

- J 2014 SCC OnLine Del 1057 Payalrajput2123 Gmailcom 20231218 124128 1 4Document4 pagesJ 2014 SCC OnLine Del 1057 Payalrajput2123 Gmailcom 20231218 124128 1 4payal.rajput.official065No ratings yet

- In The High Court of Sindh Circuit Court Hyderabad.: Sindh Small Industries CorporationDocument12 pagesIn The High Court of Sindh Circuit Court Hyderabad.: Sindh Small Industries CorporationMike KaloNo ratings yet

- Uma Maheswari - ITAT ChennaiDocument6 pagesUma Maheswari - ITAT ChennaiLakshmivenkataraman T.SNo ratings yet

- Icy Y: Volume - IDocument120 pagesIcy Y: Volume - INeha MakeoversNo ratings yet

- CYGNUS CIRP ORDERDocument26 pagesCYGNUS CIRP ORDERNikhil MaanNo ratings yet

- Arvind Kumar Nirala - Anticipatory BailDocument7 pagesArvind Kumar Nirala - Anticipatory BailabhipravNo ratings yet

- Kotak Mahindra Bank LTD Vs A Balakrishnan On 30 May 2022Document23 pagesKotak Mahindra Bank LTD Vs A Balakrishnan On 30 May 2022Surya Veer SinghNo ratings yet

- 534 Kotak Mahindra Bank LTD V A Balakrishna 30 May 2022 420033Document22 pages534 Kotak Mahindra Bank LTD V A Balakrishna 30 May 2022 420033Vidushi RaiNo ratings yet

- J 2021 SCC OnLine Kar 12934 AIR 2021 Kar 155 2021 4 AI 20221109 095745 1 8Document8 pagesJ 2021 SCC OnLine Kar 12934 AIR 2021 Kar 155 2021 4 AI 20221109 095745 1 8SAI SUVEDHYA RNo ratings yet

- Urban Improvement Trust Vs Magha Ram NCDRC DelhiDocument6 pagesUrban Improvement Trust Vs Magha Ram NCDRC DelhirelaxyouknowitNo ratings yet

- CYGNUS - 13.12.2023 ORDERDocument59 pagesCYGNUS - 13.12.2023 ORDERNikhil MaanNo ratings yet

- Cholamandalam Vs SARANJEET SINGH SODhi (Noida)Document11 pagesCholamandalam Vs SARANJEET SINGH SODhi (Noida)jitendra singhNo ratings yet

- Bhavdipbhai Arunbhai Dave Vs Kotak Mahindra Bank LGJ2022090222165556143COM189934Document16 pagesBhavdipbhai Arunbhai Dave Vs Kotak Mahindra Bank LGJ2022090222165556143COM189934Sakshi ShettyNo ratings yet

- Baidhar Broiler & ChickenDocument12 pagesBaidhar Broiler & ChickenK SANMUKHA PATRANo ratings yet

- BetweenDocument5 pagesBetweenMS Law AdvocatesNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Form Three AssignmentDocument5 pagesForm Three AssignmentKennedy Odhiambo OchiengNo ratings yet

- Banking Awareness Hand Book by Er. G C Nayak PDFDocument86 pagesBanking Awareness Hand Book by Er. G C Nayak PDFTapas Kumar NandiNo ratings yet

- Performance Analysis of IFIC Bank Limited PDFDocument40 pagesPerformance Analysis of IFIC Bank Limited PDFTusher HasanNo ratings yet

- Request Jud Not W Motion Joinder 4-29-13 0Document518 pagesRequest Jud Not W Motion Joinder 4-29-13 0Nancy Duffy McCarronNo ratings yet

- HDFC Bank Freedom Credit CardDocument9 pagesHDFC Bank Freedom Credit CardKuldeep rajakNo ratings yet

- Expert Witness DiscloseDocument4 pagesExpert Witness Discloseexpretwitness100% (1)

- Money market rolesDocument2 pagesMoney market rolesAilaJeanineNo ratings yet

- Note Mate:: Working Capital DogsDocument7 pagesNote Mate:: Working Capital Dogsdon faperNo ratings yet

- Loan Application Cash Advance BonusDocument1 pageLoan Application Cash Advance BonusSharlene338No ratings yet

- Reddy 1Document15 pagesReddy 1Vara Prasad AvulaNo ratings yet

- Mukesh Surana's Balance Sheet and Profit & Loss StatementDocument5 pagesMukesh Surana's Balance Sheet and Profit & Loss StatementSURANA1973No ratings yet

- Berjamin, Eric Brian - BSA - IA - Act (Journal)Document3 pagesBerjamin, Eric Brian - BSA - IA - Act (Journal)Eric BerjaminNo ratings yet

- Ebesun Co4Document8 pagesEbesun Co4Chidinma NnoliNo ratings yet

- Rupay Vs VisaDocument5 pagesRupay Vs VisaSriya KannegantiNo ratings yet

- Statistics On Scheduled Banks in PakistanDocument28 pagesStatistics On Scheduled Banks in PakistanThe KAHNo ratings yet

- Ramon K. Ilusorio, Petitioner, vs. Hon. Court of AppealsDocument2 pagesRamon K. Ilusorio, Petitioner, vs. Hon. Court of AppealsrdNo ratings yet

- Meaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofDocument32 pagesMeaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofPunya KrishnaNo ratings yet

- "Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnDocument81 pages"Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnASIT EKKANo ratings yet

- G Izekf - KR FD K TKRK Gs FD BL Foi DK Vko' D Bunzkt DS'K CQD O Fmiksftv JFTLVJ Esa DJ FN K X K GsaaDocument4 pagesG Izekf - KR FD K TKRK Gs FD BL Foi DK Vko' D Bunzkt DS'K CQD O Fmiksftv JFTLVJ Esa DJ FN K X K GsaaRakesh AryaNo ratings yet

- PALTOK CREDIT COOPERATIVE ACCOUNT VERIFICATIONDocument2 pagesPALTOK CREDIT COOPERATIVE ACCOUNT VERIFICATIONDaenarys VeranoNo ratings yet

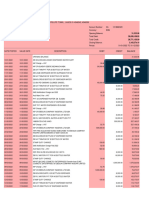

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument5 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancegaurav kumarNo ratings yet

- PPDP KPU KANUPATEN TOLITOLIDocument54 pagesPPDP KPU KANUPATEN TOLITOLISuhaeni EniNo ratings yet

- Certificate of Deposit and Commercial PaperDocument5 pagesCertificate of Deposit and Commercial Paperkapil98180No ratings yet

- INLAND LETTER OF CREDITDocument7 pagesINLAND LETTER OF CREDITDeepak MishraNo ratings yet

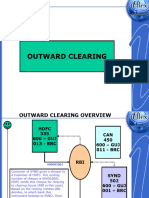

- 5-SETTLEMENT-Outward Clearing 1Document21 pages5-SETTLEMENT-Outward Clearing 1ola.cloudsNo ratings yet