You might also like

- Travel Insurance Final Project Yash NaikDocument57 pagesTravel Insurance Final Project Yash NaikVedant Mahajan80% (5)

- Exploring Wildlife: Stock Market GitaDocument10 pagesExploring Wildlife: Stock Market Gita01ankuNo ratings yet

- Functional Definition of Insurance: MeaningDocument6 pagesFunctional Definition of Insurance: MeaningShubham DhimaanNo ratings yet

- 7 P's of Insurance IndustryDocument13 pages7 P's of Insurance IndustryFazlur RahmanNo ratings yet

- Iom Concept of InsuranceDocument4 pagesIom Concept of Insuranceowuor PeterNo ratings yet

- Insurance CompaniesDocument11 pagesInsurance CompaniesPricia AbellaNo ratings yet

- Chapter 1: Basics of Insurance: Let's BeginDocument27 pagesChapter 1: Basics of Insurance: Let's BeginAviNo ratings yet

- Chapter 1: Basics of Insurance: Let's BeginDocument27 pagesChapter 1: Basics of Insurance: Let's BeginAviNo ratings yet

- Basics of Insurance in 40 CharactersDocument27 pagesBasics of Insurance in 40 CharactersDipesh ShuklaNo ratings yet

- Pbi Module 4Document18 pagesPbi Module 4Sweta BastiaNo ratings yet

- Chapter 1-What Is Insurance?Document20 pagesChapter 1-What Is Insurance?Akshada Chitnis100% (2)

- Insurance NotesDocument46 pagesInsurance NotespuruNo ratings yet

- Pbi Module 4Document18 pagesPbi Module 4SUBHECHHA MOHAPATRANo ratings yet

- Child Insurance PlanDocument72 pagesChild Insurance PlanAnvesh Pulishetty -BNo ratings yet

- INSURANCE (Updated)Document50 pagesINSURANCE (Updated)annafray7No ratings yet

- Business Services - Part 3: ObjectivesDocument14 pagesBusiness Services - Part 3: ObjectivesSanta GlenmarkNo ratings yet

- Chapter 05 RMIDocument16 pagesChapter 05 RMISudipta BaruaNo ratings yet

- Basics of Business Insurance - NotesDocument41 pagesBasics of Business Insurance - Notesjeganrajraj100% (1)

- InsuranceDocument3 pagesInsuranceMonique McfarlaneNo ratings yet

- History and Types of Insurance in IndiaDocument72 pagesHistory and Types of Insurance in India6338250% (4)

- 1571208536-INSURANCELAWDocument136 pages1571208536-INSURANCELAWStuti SinhaNo ratings yet

- New Microsoft Office Word DocumentDocument63 pagesNew Microsoft Office Word DocumentAmin HoqNo ratings yet

- Introduction To InsuranceDocument15 pagesIntroduction To InsuranceInza NsaNo ratings yet

- Final DraftDocument71 pagesFinal DraftPayal RaghorteNo ratings yet

- INTRODUCTIONDocument20 pagesINTRODUCTIONLEARN WITH AGALYANo ratings yet

- Insurance Is A Means of Protection From Financial Loss. It Is A Form of Risk Management PrimarilyDocument7 pagesInsurance Is A Means of Protection From Financial Loss. It Is A Form of Risk Management PrimarilyPramila ChauhanNo ratings yet

- Kuch BhiDocument13 pagesKuch BhiSAUMYANo ratings yet

- Definition of Insurance Insurance PremiumDocument3 pagesDefinition of Insurance Insurance Premiumshefallidhuria7No ratings yet

- What Is Insurance and Why You Need It!Document2 pagesWhat Is Insurance and Why You Need It!FACTS- WORLDNo ratings yet

- Insurance ProvisionDocument8 pagesInsurance ProvisionJake GuataNo ratings yet

- InsuranceDocument18 pagesInsuranceDRUVA KIRANNo ratings yet

- Insurance: 1 Lesson 1 Introduction To InsuranceDocument14 pagesInsurance: 1 Lesson 1 Introduction To Insurancevipul sutharNo ratings yet

- Apollo MunichDocument52 pagesApollo MunichSumit ManglaniNo ratings yet

- Definition of InsuranceDocument11 pagesDefinition of InsurancePuru SharmaNo ratings yet

- Principles of Insurance: Risk Management, To HedgeDocument7 pagesPrinciples of Insurance: Risk Management, To HedgeifthisamNo ratings yet

- Banking and Insurance Unit III Study NotesDocument13 pagesBanking and Insurance Unit III Study NotesSekar M KPRCAS-CommerceNo ratings yet

- 3 Principles of InsuranceDocument15 pages3 Principles of InsuranceZerin Hossain100% (1)

- Insurance and Risk Management Unit IDocument9 pagesInsurance and Risk Management Unit Ipooranim1976No ratings yet

- Art InsuranceDocument54 pagesArt InsuranceLove Aute100% (1)

- Insurance and Risk ManagementDocument10 pagesInsurance and Risk Managementhitesh gargNo ratings yet

- Reliance Life InsuranceDocument101 pagesReliance Life InsuranceVicky Mishra100% (2)

- Chapter - 5 ModuleDocument7 pagesChapter - 5 ModuleAllyjen SampangNo ratings yet

- Insurance PrinicilesDocument9 pagesInsurance PrinicilesEmmanuella ChantengNo ratings yet

- Bus Law Insu. PartDocument23 pagesBus Law Insu. PartBona IbrahimNo ratings yet

- INSURANCEDocument11 pagesINSURANCESashNo ratings yet

- 18BCO32C-U1Document14 pages18BCO32C-U1Vipul TyagiNo ratings yet

- Insurance CompanyDocument9 pagesInsurance CompanyMD Abdur RahmanNo ratings yet

- Daniel AyoolaDocument10 pagesDaniel AyoolaSalim SulaimanNo ratings yet

- ppt4Document64 pagesppt4EdenNo ratings yet

- Mhatre 30Document98 pagesMhatre 30sandeepNo ratings yet

- Introduction To Insurance: Asstt. Professor, SRCC, University of DelhiDocument30 pagesIntroduction To Insurance: Asstt. Professor, SRCC, University of DelhikanikaNo ratings yet

- Art InsuranceDocument52 pagesArt InsuranceYadav RahulNo ratings yet

- B.Com(Hons.) Semester-III Personal Finance and PlanningDocument59 pagesB.Com(Hons.) Semester-III Personal Finance and PlanningsonuNo ratings yet

- Insurance - 2013Document25 pagesInsurance - 2013Crazy KamaNo ratings yet

- InsuranceDocument7 pagesInsuranceraghunaikaNo ratings yet

- 4ec5ebfi - Module 4, Insurance Insts.Document17 pages4ec5ebfi - Module 4, Insurance Insts.chauhanpankajNo ratings yet

- My ProjectDocument30 pagesMy ProjectPriyanka satamNo ratings yet

- Institution That Offers A Person, Company, or Other Entity Reimbursement or Financial Protection Against Possible Future Losses or DamagesDocument16 pagesInstitution That Offers A Person, Company, or Other Entity Reimbursement or Financial Protection Against Possible Future Losses or DamagesHrishikesh DharNo ratings yet

- Insurance Principles, Types and Industry in IndiaDocument10 pagesInsurance Principles, Types and Industry in IndiaAroop PalNo ratings yet

- Short Not2Document11 pagesShort Not2Tilahun GirmaNo ratings yet

- Fin221 Ca1Document22 pagesFin221 Ca1Devanshi SharmaNo ratings yet

- 7 InsuranceDocument10 pages7 InsuranceLynner Anne DeytaNo ratings yet

- "A Comprehensive Study of Currency Market in India.": A Dissertation Report ONDocument64 pages"A Comprehensive Study of Currency Market in India.": A Dissertation Report ONBerkshire Hathway coldNo ratings yet

- 17 Insurance Essay by BankershalaDocument13 pages17 Insurance Essay by BankershalaDAX LABORATORYNo ratings yet

- Allen Overy 3 49729Document10 pagesAllen Overy 3 49729Jose CarterNo ratings yet

- Vstoxx Jun01Document22 pagesVstoxx Jun01maixoroNo ratings yet

- Module 5 Basic Time Value of MoneyDocument33 pagesModule 5 Basic Time Value of Moneylord kwantoniumNo ratings yet

- Forward and Futures MarketDocument51 pagesForward and Futures MarketHarsh DaniNo ratings yet

- Business Law AssignmentDocument4 pagesBusiness Law AssignmentTho LaNo ratings yet

- P5 Formulae SheetDocument2 pagesP5 Formulae Sheet21000021No ratings yet

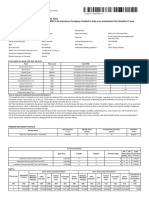

- Number of Instalments and Payment Mode Received Date Coll. Br. Serv. Br. Premium/ Additional Premium Amount Service Tax / GST Amount ReceivedDocument1 pageNumber of Instalments and Payment Mode Received Date Coll. Br. Serv. Br. Premium/ Additional Premium Amount Service Tax / GST Amount ReceivedSaumy VishwakarmaNo ratings yet

- Fire InsuranceDocument4 pagesFire Insuranceজাহিদ হৃদয়No ratings yet

- Insurance History and Reforms in IndiaDocument34 pagesInsurance History and Reforms in Indiarahul krishnaNo ratings yet

- International student insurance SpainDocument2 pagesInternational student insurance SpainFares BencheikhNo ratings yet

- 121-Article Text-199-1-10-20200219Document10 pages121-Article Text-199-1-10-20200219Kepal MiloNo ratings yet

- Basic Principles of InsuranceDocument11 pagesBasic Principles of Insurancesreedevi sureshNo ratings yet

- Module 4 ECON AnnuityDocument11 pagesModule 4 ECON AnnuityMIKE ARTHUR DAVIDNo ratings yet

- Article 28 UCP 600Document8 pagesArticle 28 UCP 600Jhoo AngelNo ratings yet

- 7 United India Cashless Garages (Car) in PanchkulDocument1 page7 United India Cashless Garages (Car) in PanchkulManish Singh KhatriNo ratings yet

- TRAVEL INSURANCE CERTIFICATEDocument2 pagesTRAVEL INSURANCE CERTIFICATELusi FebriantiNo ratings yet

- Topic 8 Legal IssuesDocument106 pagesTopic 8 Legal IssuesM S A B D A L L A H ?No ratings yet

- PFRS 17 Insurance Contracts SummaryDocument32 pagesPFRS 17 Insurance Contracts SummaryVictoria CadizNo ratings yet

- Call Ratio Back SpreadDocument4 pagesCall Ratio Back SpreadsidNo ratings yet

- Template Convertible Loan Agreement 211129 Final 1Document16 pagesTemplate Convertible Loan Agreement 211129 Final 1CrisNo ratings yet

- Arm - MF - Final - Sample (From 2016)Document27 pagesArm - MF - Final - Sample (From 2016)甜瓜No ratings yet

- Chapter 1Document34 pagesChapter 1Sanjoy dasNo ratings yet

- Project:: Form 1 Owner Controlled Insurance Program Insurance Cost Information WorksheetDocument13 pagesProject:: Form 1 Owner Controlled Insurance Program Insurance Cost Information WorksheetSyed NNo ratings yet

- Benefit Illustration for HDFC SL ProGrowth FlexiDocument3 pagesBenefit Illustration for HDFC SL ProGrowth FlexiFuse BulbNo ratings yet

- Terms & Conditions: Product Name: Tata Aia Life Insurance Sampoorna Raksha Supreme - Non Pos LP/RP UIN: 110N160V02Document3 pagesTerms & Conditions: Product Name: Tata Aia Life Insurance Sampoorna Raksha Supreme - Non Pos LP/RP UIN: 110N160V02Himanshi ChauhanNo ratings yet