You might also like

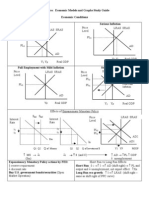

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- CRM Practices in BanksDocument26 pagesCRM Practices in BanksIshtiaz MahmoodNo ratings yet

- Bank ReconciliationDocument41 pagesBank ReconciliationKarl Mendez100% (2)

- Ivylorainepenriquez: Page1of4 248brgymaahas 0 9 1 9 - 2 8 2 5 - 1 7 Lagunalosbanos 4 0 3 0Document4 pagesIvylorainepenriquez: Page1of4 248brgymaahas 0 9 1 9 - 2 8 2 5 - 1 7 Lagunalosbanos 4 0 3 0ivy loraine enriquezNo ratings yet

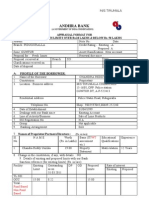

- Andhra Bank: Appraisal Format For Advances With Limits Over Rs.10 Lakhs & Below Rs. 50 LakhsDocument9 pagesAndhra Bank: Appraisal Format For Advances With Limits Over Rs.10 Lakhs & Below Rs. 50 LakhsSivaramakrishna NeelamNo ratings yet

- StatementDocument2 pagesStatementKekanda FauziNo ratings yet

- Recent Trends in BankingDocument4 pagesRecent Trends in Bankingsuresh50% (2)

- A Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (Accf)Document56 pagesA Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (Accf)Saurabh Chawla100% (1)

- Role of IT in BankingDocument11 pagesRole of IT in BankingManjrekar RohanNo ratings yet

- Credit Risk Management at HDFC Project Report Mba FinanceDocument102 pagesCredit Risk Management at HDFC Project Report Mba FinanceShrishant Gaynewar82% (17)

- E-Banking: Submitted By:-Aditi Mangal Harsha Srivastava Nakul AgarwalDocument45 pagesE-Banking: Submitted By:-Aditi Mangal Harsha Srivastava Nakul AgarwalAditi MangalNo ratings yet

- Pdic QuestionsDocument8 pagesPdic QuestionsdemosreaNo ratings yet

- Server Swift Abbygb2l-1Document3 pagesServer Swift Abbygb2l-1planetamundo2017No ratings yet

- Impact of Government Policy and Regulations in BankingDocument65 pagesImpact of Government Policy and Regulations in BankingNiraj ThapaNo ratings yet

- E Banking Report - Punjab National BankDocument65 pagesE Banking Report - Punjab National BankParveen ChawlaNo ratings yet

- A Strategic Analysis On Digital Banking With Reference To HDFC BankDocument63 pagesA Strategic Analysis On Digital Banking With Reference To HDFC Bankjoju felixNo ratings yet

- Core BankingDocument37 pagesCore Bankingnwani25No ratings yet

- Role of IT in Banking SectorDocument9 pagesRole of IT in Banking SectorChitral Mistry50% (2)

- Chapter 1: Introduction To Digital BankingDocument9 pagesChapter 1: Introduction To Digital BankingPriyanka JNo ratings yet

- Digital Banking in India: Recent Trends, Advantages and DisadvantagesDocument4 pagesDigital Banking in India: Recent Trends, Advantages and DisadvantagesAmazing VideosNo ratings yet

- Digital Banking and Alternative SystemsDocument31 pagesDigital Banking and Alternative SystemsRameen ZafarNo ratings yet

- Mod 1 Mbfs PDF NewDocument22 pagesMod 1 Mbfs PDF NewWalidahmad AlamNo ratings yet

- Bank Management Cia 1 Component 2: Submitted To-Parvathy V KDocument7 pagesBank Management Cia 1 Component 2: Submitted To-Parvathy V Kdivyansh khandujaNo ratings yet

- Role of Information Technology in The Banking SectorDocument4 pagesRole of Information Technology in The Banking SectorZonaeidZamanNo ratings yet

- Digital Banking: A Mini Project Report OnDocument22 pagesDigital Banking: A Mini Project Report Onvinayak mishraNo ratings yet

- A Study On Virtual FinanceDocument5 pagesA Study On Virtual FinanceThe Rookie GuitaristNo ratings yet

- Techdevelopmentsinbanking 120509205806 Phpapp01Document43 pagesTechdevelopmentsinbanking 120509205806 Phpapp01PatelMayurNo ratings yet

- Customer Perception On E-Banking Services - A Study With Reference To Private and Public Sector BanksDocument12 pagesCustomer Perception On E-Banking Services - A Study With Reference To Private and Public Sector BanksVenkat 19P259No ratings yet

- An Automated Teller Machine (ATM) Is A Computerized Telecommunications Device That EnablesDocument2 pagesAn Automated Teller Machine (ATM) Is A Computerized Telecommunications Device That EnablesParvesh GeerishNo ratings yet

- E Banking FerozpurDocument7 pagesE Banking FerozpurGunjan JainNo ratings yet

- Banking Sector - Survival of The FittestDocument9 pagesBanking Sector - Survival of The FittestSwati SinghNo ratings yet

- Manish Kumar-11541465720895Document18 pagesManish Kumar-11541465720895Kavya ReddyNo ratings yet

- Meaning of E-Banking: 3.2 Automated Teller MachineDocument16 pagesMeaning of E-Banking: 3.2 Automated Teller Machinehuneet SinghNo ratings yet

- Information Technology in The Banking Sector - Opportunities, Threats and StrategiesDocument7 pagesInformation Technology in The Banking Sector - Opportunities, Threats and StrategiesMahadi HasanNo ratings yet

- Online BankingDocument10 pagesOnline BankingVishal MittalNo ratings yet

- Increase-The Government's Encouragement To Use Electronic Wallets Has Contributed Much ToDocument3 pagesIncrease-The Government's Encouragement To Use Electronic Wallets Has Contributed Much ToMahima SharmaNo ratings yet

- Niteesh Kumar Research ReportDocument13 pagesNiteesh Kumar Research ReportBittu MallikNo ratings yet

- MKTNG Term PaperDocument22 pagesMKTNG Term Paperbinzidd007No ratings yet

- Introduction - (25838)Document28 pagesIntroduction - (25838)Anonymous itZP6kzNo ratings yet

- AWAIS Operation ManagementDocument9 pagesAWAIS Operation Managementawais tariqNo ratings yet

- TH ST STDocument8 pagesTH ST STSaloni Jain 1820343No ratings yet

- Role of e - Banking in Current ScenarioDocument5 pagesRole of e - Banking in Current ScenarioInternational Jpurnal Of Technical Research And ApplicationsNo ratings yet

- Mentorship Report On Digitization in BankingDocument46 pagesMentorship Report On Digitization in BankingravneetNo ratings yet

- Full PaperDocument11 pagesFull Paperasra_ahmedNo ratings yet

- Chapter - 1: History of Digital BankingDocument18 pagesChapter - 1: History of Digital BankingArunangsu ChandaNo ratings yet

- Banking and Operation Assignment: Submitted By: Prashant Ghimire 17021141125 Batch: 2017-19Document10 pagesBanking and Operation Assignment: Submitted By: Prashant Ghimire 17021141125 Batch: 2017-19Prashant GhimireNo ratings yet

- Project Report ON "Consumer Behaviour Towards E-Banking in Private Sector BanksDocument23 pagesProject Report ON "Consumer Behaviour Towards E-Banking in Private Sector BanksRAHULNo ratings yet

- Assign 1Document3 pagesAssign 1Aakash VighnuNo ratings yet

- Project FileDocument5 pagesProject FileRavi JadonNo ratings yet

- IT in BankingDocument11 pagesIT in BankingTanyaJhaNo ratings yet

- FIS Banking INDUSTRYDocument27 pagesFIS Banking INDUSTRYNamyenya MaryNo ratings yet

- e-CRM in Banks: Four Key Areas of Business: Strategy, People, Technology and Process. The Processes in TheDocument5 pagese-CRM in Banks: Four Key Areas of Business: Strategy, People, Technology and Process. The Processes in ThePoojaNo ratings yet

- Chapter 1.editedDocument15 pagesChapter 1.editedamrozia mazharNo ratings yet

- Evolution Mobile BankingDocument7 pagesEvolution Mobile Bankingtsri0405No ratings yet

- Problems Encountered and Level of Customer Satisfaction On The Use of Mobile Banking Application of Selected Consumers in City of San FernandoDocument17 pagesProblems Encountered and Level of Customer Satisfaction On The Use of Mobile Banking Application of Selected Consumers in City of San FernandoHazel Andrea Garduque LopezNo ratings yet

- Introduction To DigitalizationDocument11 pagesIntroduction To Digitalizationdolly guptaNo ratings yet

- 7th Page BodyDocument50 pages7th Page BodybhawanachitlangiaNo ratings yet

- Ms. Rabaya Bosri Assistant Professor of Finance and Course Coordinator (MBA Program)Document14 pagesMs. Rabaya Bosri Assistant Professor of Finance and Course Coordinator (MBA Program)MAMUN AlNo ratings yet

- 3799 - 08.Ms - Neeta & Dr. V.k.bakshiDocument7 pages3799 - 08.Ms - Neeta & Dr. V.k.bakshiBeena SadhwaniNo ratings yet

- Fpoha17074 Complete WorkDocument15 pagesFpoha17074 Complete WorkPrince TreasureNo ratings yet

- Karan Tolani (FC) Project 2022Document14 pagesKaran Tolani (FC) Project 2022Karan TolaniNo ratings yet

- The Impact of E-Banking On Customers in IndiaDocument77 pagesThe Impact of E-Banking On Customers in Indiataslimr191No ratings yet

- 10 - Chapter 3Document24 pages10 - Chapter 3Eloysa CarpoNo ratings yet

- Chapter - IDocument6 pagesChapter - IUzairKhanNo ratings yet

- A Project Report On Virtual Banking 1Document54 pagesA Project Report On Virtual Banking 1vaibhav shuklaNo ratings yet

- Mobile Banking and Customer SatisfactionDocument8 pagesMobile Banking and Customer SatisfactionVDC CommerceNo ratings yet

- Lending Policy of Nepal Bank by Nabina RegmiDocument45 pagesLending Policy of Nepal Bank by Nabina RegmiKaran Pandey50% (2)

- Black Book Summer InternshipDocument52 pagesBlack Book Summer InternshipDhwani PrajapatiNo ratings yet

- George Soros Kubo Kohut 4.BDocument21 pagesGeorge Soros Kubo Kohut 4.BkohutNo ratings yet

- Modification Form: Customer Account Type: For Bank UseDocument2 pagesModification Form: Customer Account Type: For Bank UseAniket PandeyNo ratings yet

- New Vendor Registration Form - VER - 2 3Document4 pagesNew Vendor Registration Form - VER - 2 3keyurNo ratings yet

- Multinational Corporations: Some of Characteristics of Mncs AreDocument7 pagesMultinational Corporations: Some of Characteristics of Mncs AreMuskan KaurNo ratings yet

- Factura Vtex Abril 2021Document1 pageFactura Vtex Abril 2021Rayssita espinozaNo ratings yet

- Asian Development Bank: Project Completion ReportDocument34 pagesAsian Development Bank: Project Completion ReportsanthoshkumarkrNo ratings yet

- Examination Report From Assoc Prof Fock Siew Tong BF326 Bank Financing & Credit Management Semester 2 AY2010-11Document2 pagesExamination Report From Assoc Prof Fock Siew Tong BF326 Bank Financing & Credit Management Semester 2 AY2010-11Felecia Sabtuharini HandrawanNo ratings yet

- Report On Dutch Bangla Bank Ratio AnalysisDocument32 pagesReport On Dutch Bangla Bank Ratio AnalysisMishuNo ratings yet

- Private Equity Deal-Making 101 - Evaluation, Structuring, and RestructuringDocument4 pagesPrivate Equity Deal-Making 101 - Evaluation, Structuring, and RestructuringUnited States Private Equity CouncilNo ratings yet

- DocxDocument7 pagesDocxSaoxalo ONo ratings yet

- Dwnload Full Accounting Information Systems 14th Edition Romney Test Bank PDFDocument36 pagesDwnload Full Accounting Information Systems 14th Edition Romney Test Bank PDFmoinsorzalv100% (16)

- Unit 23: Regulating The Financial Sector: Lead inDocument3 pagesUnit 23: Regulating The Financial Sector: Lead inMinh Châu Tạ ThịNo ratings yet

- Mfi AssignmentDocument5 pagesMfi Assignmentdeepika singhNo ratings yet

- Quiz 5Document8 pagesQuiz 5Putin Phy0% (1)

- DownloadDocument1 pageDownloadambi cNo ratings yet

- Asset Based FinancingDocument64 pagesAsset Based FinancingChintan Shah100% (1)

- Retail Job Interview Questions To AskDocument7 pagesRetail Job Interview Questions To AskaskmeeNo ratings yet

- IT Audit ManagerDocument3 pagesIT Audit Managerapi-77385233No ratings yet