You might also like

- Principles of MicroeconomicsDocument16 pagesPrinciples of MicroeconomicsAnonymous GAulxiI100% (4)

- Macroeconomics Test BankDocument108 pagesMacroeconomics Test BankRaghav100% (1)

- ECO 111 - Tutorial Questions - October 2021Document8 pagesECO 111 - Tutorial Questions - October 2021Nɩʜɩɭɩstic Ucʜɩʜʌ SʌsʋĸɘNo ratings yet

- Test Bank For Managerial Economics Applications Strategy and Tactics 12th Edition by McGuiganDocument4 pagesTest Bank For Managerial Economics Applications Strategy and Tactics 12th Edition by McGuiganPatriniaRupestrisNo ratings yet

- Mock Test 7 Suggested SolutionDocument10 pagesMock Test 7 Suggested SolutionHung SarahNo ratings yet

- Real Estate Economics - ReadingsDocument5 pagesReal Estate Economics - ReadingsCoursePinNo ratings yet

- Business Finance ReviewerDocument5 pagesBusiness Finance ReviewerGela May SadianNo ratings yet

- ECN 104 FINAL ExamDocument19 pagesECN 104 FINAL Examzodiac1b1100% (1)

- Managerial EconomicsDocument3 pagesManagerial EconomicsnaeemakhtaracmaNo ratings yet

- Sample Review Questions For FinalDocument17 pagesSample Review Questions For FinalJon Mckenzie GoNo ratings yet

- Revision For Business Final Work SheetDocument9 pagesRevision For Business Final Work SheetCynthia HarbNo ratings yet

- Midterm PracticeDocument9 pagesMidterm PracticeIzza NaseerNo ratings yet

- Practice Exam 1Document4 pagesPractice Exam 1JamieNo ratings yet

- Model Test Paper - IDocument9 pagesModel Test Paper - IAkashdeep MukherjeeNo ratings yet

- Sample - Question For HS 108Document5 pagesSample - Question For HS 108Anonymous 001No ratings yet

- Principles of Economics Test 2 BPA 1205Document3 pagesPrinciples of Economics Test 2 BPA 1205Alinaitwe GodfreyNo ratings yet

- Bahria University (Karachi Campus) : Assignment Guidelines by The TeacherDocument4 pagesBahria University (Karachi Campus) : Assignment Guidelines by The TeacherAbdullah EhsanNo ratings yet

- B) Economics Studies How To Choose The Best Alternative When Coping With ScarcityDocument7 pagesB) Economics Studies How To Choose The Best Alternative When Coping With ScarcityDexter BordajeNo ratings yet

- INQUISITIVE TO STUDY - Set 5Document7 pagesINQUISITIVE TO STUDY - Set 5richmannkansahNo ratings yet

- Economics Sample Paper 1Document3 pagesEconomics Sample Paper 1L IneshNo ratings yet

- BHRM Test One Micro Final Marking GuideDocument6 pagesBHRM Test One Micro Final Marking GuideEsther NerimaNo ratings yet

- Price Elasticity of Demand and Supply: Key Concepts Practice Quiz Internet ExercisesDocument103 pagesPrice Elasticity of Demand and Supply: Key Concepts Practice Quiz Internet ExercisesPamela CabangNo ratings yet

- Sample Paper 1Document6 pagesSample Paper 1Umesh BhardwajNo ratings yet

- Economics Exam Paper 1 Term 1 (Econs 1)Document10 pagesEconomics Exam Paper 1 Term 1 (Econs 1)Rose VelvetNo ratings yet

- Introduction To Economics and Finance: MOCK (Spring 2013) Section: B 100 Marks-3hoursDocument5 pagesIntroduction To Economics and Finance: MOCK (Spring 2013) Section: B 100 Marks-3hoursANo ratings yet

- ECO2144 Micro Theory I 2007 Final ExamDocument5 pagesECO2144 Micro Theory I 2007 Final ExamTeachers OnlineNo ratings yet

- Economics QuestionsDocument123 pagesEconomics QuestionsMamush kasimoNo ratings yet

- Assignment 4Document2 pagesAssignment 4bluestacks3874No ratings yet

- MTP Economics 11thDocument4 pagesMTP Economics 11thiamaarushdevsharmaNo ratings yet

- HUL212 MODERN MICROECONOMICS - IIT Delhi - Minor-1 - Engineering - Year-2008 - 106Document3 pagesHUL212 MODERN MICROECONOMICS - IIT Delhi - Minor-1 - Engineering - Year-2008 - 106Sachin BatwaniNo ratings yet

- Imi611s-Intermediate Microeconomics-1st Opp-June 2022Document7 pagesImi611s-Intermediate Microeconomics-1st Opp-June 2022Smart Academic solutionsNo ratings yet

- Assignment On Managerial EconomicsDocument5 pagesAssignment On Managerial EconomicsMustefa NuredinNo ratings yet

- Group AssignmDocument2 pagesGroup AssignmJibril JundiNo ratings yet

- GiẠI Quiz VI MãDocument25 pagesGiẠI Quiz VI MãhaNo ratings yet

- Practice Exercise Ch.6 BECN 150 (ST) F-21)Document11 pagesPractice Exercise Ch.6 BECN 150 (ST) F-21)brinthaNo ratings yet

- Problem Set 5Document6 pagesProblem Set 5Thulasi 2036No ratings yet

- Tutorial Questions - EconomicsDocument3 pagesTutorial Questions - EconomicsBoago Motswà GoleNo ratings yet

- Eco 162 Microeconomics PDFDocument22 pagesEco 162 Microeconomics PDFjungkook wifeNo ratings yet

- Eco XiDocument3 pagesEco XiRekha DeviNo ratings yet

- Econ 1550 Sem 20304Document14 pagesEcon 1550 Sem 20304M Aminuddin AnwarNo ratings yet

- SSE108 Final ExaminationDocument14 pagesSSE108 Final ExaminationjasminNo ratings yet

- ECON 247 Practice Midterm ExaminationDocument9 pagesECON 247 Practice Midterm ExaminationRobyn ShirvanNo ratings yet

- Economics Class - XII Time - 3 Hours. Maximum Marks - 100 Notes: 1. 2. 3. 4. 5. 6. 7Document12 pagesEconomics Class - XII Time - 3 Hours. Maximum Marks - 100 Notes: 1. 2. 3. 4. 5. 6. 7sahilNo ratings yet

- Online Assessment For ECO120 Principles of Economics (Oct 2021 To Feb 2022)Document9 pagesOnline Assessment For ECO120 Principles of Economics (Oct 2021 To Feb 2022)AIN ZULLAIKHANo ratings yet

- Problem Set 2 (Econ210 Microeconomics) EditedDocument10 pagesProblem Set 2 (Econ210 Microeconomics) Editedtuana aNo ratings yet

- Time Allowed: 3 Hours Maximum Marks: 100 General InstructionsDocument3 pagesTime Allowed: 3 Hours Maximum Marks: 100 General InstructionsManminder SinghNo ratings yet

- Microeconomics Practice ExamDocument15 pagesMicroeconomics Practice ExamVera van GansewinkelNo ratings yet

- Multiple Choice Quiz Chapter 3 4Document9 pagesMultiple Choice Quiz Chapter 3 4Linh Tran PhuongNo ratings yet

- MCQ and Conceptual QuestionsDocument14 pagesMCQ and Conceptual QuestionsAbhisek MishraNo ratings yet

- Answer: ADocument7 pagesAnswer: AusjaamNo ratings yet

- Exam1-A - No Answer KeyDocument6 pagesExam1-A - No Answer KeyTrung Kiên NguyễnNo ratings yet

- Assingment BEDocument3 pagesAssingment BERavi Prakash VermaNo ratings yet

- Assignment 1ADocument5 pagesAssignment 1Agreatguy_070% (1)

- Econs Trial QuestionsDocument5 pagesEcons Trial Questionsdemajesty12No ratings yet

- Mid Term BeDocument7 pagesMid Term BeBách HuyNo ratings yet

- BAM 040 P2 Long Quiz Answer Key 2Document4 pagesBAM 040 P2 Long Quiz Answer Key 2mkrisnaharq99No ratings yet

- MBS 1st Sem Model Question 2019Document14 pagesMBS 1st Sem Model Question 2019prakash chauagainNo ratings yet

- CAF-Business Economics PDFDocument40 pagesCAF-Business Economics PDFadnan sheikNo ratings yet

- Modern Principles Macroeconomics 3rd Edition Cowen Test Bank 1Document86 pagesModern Principles Macroeconomics 3rd Edition Cowen Test Bank 1george100% (50)

- Modern Principles Macroeconomics 3Rd Edition Cowen Test Bank Full Chapter PDFDocument36 pagesModern Principles Macroeconomics 3Rd Edition Cowen Test Bank Full Chapter PDFbilly.koenitzer727100% (11)

- Tutorial Set 5 - Microeconomics UGBS 201-2Document7 pagesTutorial Set 5 - Microeconomics UGBS 201-2FrizzleNo ratings yet

- Exercises Chapter 1Document19 pagesExercises Chapter 1D LVNo ratings yet

- Class Exercise 4Document4 pagesClass Exercise 4ghorbelfatma12No ratings yet

- MULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionDocument14 pagesMULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionTunahan KüçükerNo ratings yet

- Regional and Global StrategyDocument32 pagesRegional and Global Strategycooljani01No ratings yet

- WG 1 Sep7 Problem SetDocument2 pagesWG 1 Sep7 Problem SetJotham HensenNo ratings yet

- Labor Demand ElasticitiesDocument21 pagesLabor Demand ElasticitiesAnit Jacob PhilipNo ratings yet

- Long-Term Asset and Liability ManagementDocument27 pagesLong-Term Asset and Liability ManagementImtiaz MasroorNo ratings yet

- Production With Multiple Inputs: Solutions For Microeconomics: An IntuitiveDocument22 pagesProduction With Multiple Inputs: Solutions For Microeconomics: An IntuitiveKarolina KaczmarekNo ratings yet

- SIP ReportDocument111 pagesSIP ReportDesarollo OrganizacionalNo ratings yet

- Public Finance MCQDocument23 pagesPublic Finance MCQHarshit Tripathi100% (1)

- Ioriatti Resume PDFDocument1 pageIoriatti Resume PDFnioriatti8924No ratings yet

- Economic Order, Private Law and Public Policy The Freiburg School of Law and Economics in Perspective Manfred StreitDocument21 pagesEconomic Order, Private Law and Public Policy The Freiburg School of Law and Economics in Perspective Manfred StreitFalalaNo ratings yet

- ECO1001 Economics For Decision Making 2021 Session 2 EXAMDocument7 pagesECO1001 Economics For Decision Making 2021 Session 2 EXAMIzack FullerNo ratings yet

- Economic IntegrationDocument3 pagesEconomic Integrationatta_tahirNo ratings yet

- Analysis of China's Primary Wood Products Market (Minli Wan) PDFDocument129 pagesAnalysis of China's Primary Wood Products Market (Minli Wan) PDFthaonguyen1993No ratings yet

- 2.2 How Markets Work: Igcse /O Level EconomicsDocument24 pages2.2 How Markets Work: Igcse /O Level EconomicsAditya GhoshNo ratings yet

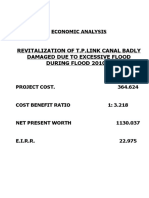

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- UntitledDocument28 pagesUntitledMaricar TelanNo ratings yet

- Week 13 WorksheetDocument9 pagesWeek 13 WorksheetKonstantin FrankNo ratings yet

- University of Pune, Pune Department of Management Sciences (Pumba), Structure of Mba++ Course (Credit System With Trimester Pattern)Document81 pagesUniversity of Pune, Pune Department of Management Sciences (Pumba), Structure of Mba++ Course (Credit System With Trimester Pattern)Amit ShuklaNo ratings yet

- Session 19Document3 pagesSession 19marialynnette lusterioNo ratings yet

- Presented By:: Mohit Chuahan Surabhi Das Pankaj Sharma Deepika Jhamtani Dheeraj ChabbraDocument10 pagesPresented By:: Mohit Chuahan Surabhi Das Pankaj Sharma Deepika Jhamtani Dheeraj ChabbraSumit BhatnagarNo ratings yet

- Chapter 6 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 6-1Document6 pagesChapter 6 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 6-1Ivern BautistaNo ratings yet

- Mkt501 - Marketing ManagementDocument11 pagesMkt501 - Marketing Management18375No ratings yet

- Planning in IndiaDocument7 pagesPlanning in IndiaAbigail Sipho Siziba (Abby)No ratings yet

- Solved The Following Relations Describe Monthly Demand and Supply Conditions inDocument1 pageSolved The Following Relations Describe Monthly Demand and Supply Conditions inM Bilal SaleemNo ratings yet

- The Limits of Arbitrage: Andrei Shleifer And Robert W.Vishny 商学院 周 美 & 杜慧卿Document22 pagesThe Limits of Arbitrage: Andrei Shleifer And Robert W.Vishny 商学院 周 美 & 杜慧卿Babar AdeebNo ratings yet

- M1 Foundation in Financial Planning and Tax Planning Syllabus FinalDocument10 pagesM1 Foundation in Financial Planning and Tax Planning Syllabus FinalCalvin YeohNo ratings yet