You might also like

- Data Analytics For Accounting Third Edition - RichardsonDocument1,237 pagesData Analytics For Accounting Third Edition - RichardsonMaría Elena Escobar-Avila100% (2)

- Data Analytics For Accounting: Vernon J. RichardsonDocument39 pagesData Analytics For Accounting: Vernon J. RichardsonNORSYAHMIZA BINTI ABDU-LATIF100% (1)

- UntitledDocument1,437 pagesUntitledsalsabila ry1No ratings yet

- Indicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesDocument1 pageIndicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesJul A.No ratings yet

- Central Recordkeeping AgencyDocument3 pagesCentral Recordkeeping AgencyKaran RamchandaniNo ratings yet

- Big Data Analytics Opportunity or Threat PDFDocument39 pagesBig Data Analytics Opportunity or Threat PDFYenny ChandraNo ratings yet

- Sample SizeDocument21 pagesSample SizeAshfaNo ratings yet

- Data Presentation and Analysis in Research PaperDocument5 pagesData Presentation and Analysis in Research Paperlrqylwznd100% (1)

- Presentation and Interpretation of Data in Research PaperDocument5 pagesPresentation and Interpretation of Data in Research PapergwjbmbvkgNo ratings yet

- Managing Customer Services: Human Resource Practices, Turnover, and Sales GrowthDocument31 pagesManaging Customer Services: Human Resource Practices, Turnover, and Sales GrowthIrbah MufidahNo ratings yet

- Managing Customer Services: Human Resource Practices, Turnover, and Sales GrowthDocument31 pagesManaging Customer Services: Human Resource Practices, Turnover, and Sales GrowthIrbah MufidahNo ratings yet

- Mcrider Journal Manager 124Document25 pagesMcrider Journal Manager 124Wilfred MartinezNo ratings yet

- Configuration Verbunden Effort Conception With Autoevalution of Intellectual Running ON Data Processor of The Sun TrackerDocument23 pagesConfiguration Verbunden Effort Conception With Autoevalution of Intellectual Running ON Data Processor of The Sun Trackersulthan_81No ratings yet

- Thesis With Factor AnalysisDocument4 pagesThesis With Factor Analysispsmxiiikd100% (2)

- Data Science EssayDocument2 pagesData Science EssayHina ShahzadiNo ratings yet

- Thesis Managerial ImplicationsDocument5 pagesThesis Managerial Implicationsashleyallenshreveport100% (1)

- Research Paper Interpretation of DataDocument7 pagesResearch Paper Interpretation of Dataafmchxxyo100% (1)

- Cappelli Tambe 2019Document30 pagesCappelli Tambe 2019bruno.vieira.iaNo ratings yet

- Online Early - Preprint of Accepted ManuscriptDocument53 pagesOnline Early - Preprint of Accepted Manuscriptsamon sumulongNo ratings yet

- Thesis Accounting SystemDocument5 pagesThesis Accounting SystemCustomPapersForCollegeUK100% (2)

- Journal of Management: Staffing in The 21st Century: New Challenges and Strategic OpportunitiesDocument31 pagesJournal of Management: Staffing in The 21st Century: New Challenges and Strategic OpportunitiesNóra FarkasNo ratings yet

- Article 2 - Big Data Analytics Opportunity or Threat For The Accounting ProfessionDocument18 pagesArticle 2 - Big Data Analytics Opportunity or Threat For The Accounting ProfessionFakhmol RisepdoNo ratings yet

- Thesis Service Dominant LogicDocument5 pagesThesis Service Dominant Logicfbyx8sck100% (1)

- Thesis On Statistical Quality Control PDFDocument5 pagesThesis On Statistical Quality Control PDFbethhalloverlandpark100% (2)

- Dissertation Topics For Hospital AdministrationDocument5 pagesDissertation Topics For Hospital AdministrationWriteMyThesisPaperDenver100% (1)

- Data Analytics For Accounting Third Edition Vernon J Richardson Full ChapterDocument67 pagesData Analytics For Accounting Third Edition Vernon J Richardson Full Chapterwhitney.mcconnel182100% (2)

- Plymouth Uni Coursework Cover SheetDocument8 pagesPlymouth Uni Coursework Cover Sheetiuhvgsvcf100% (2)

- Chapter 3 Thesis Statistical Treatment of DataDocument6 pagesChapter 3 Thesis Statistical Treatment of Datadnnpkqzw100% (2)

- MSC Dissertation Assessment CriteriaDocument6 pagesMSC Dissertation Assessment CriteriaWriteMySociologyPaperSingapore100% (1)

- Evaluating Electronic Health Record Systems: A System Dynamics SimulationDocument11 pagesEvaluating Electronic Health Record Systems: A System Dynamics Simulationkartiz008No ratings yet

- Services Science Journey: Foundations, Progress, and ChallengesDocument7 pagesServices Science Journey: Foundations, Progress, and ChallengesBoogii EnkhboldNo ratings yet

- Editorial For The Special Issue On Business Analytics ApplicationsDocument3 pagesEditorial For The Special Issue On Business Analytics Applicationssrin89No ratings yet

- Ba Business Management Dissertation TopicsDocument6 pagesBa Business Management Dissertation TopicsWhatIsTheBestPaperWritingServiceOverlandPark100% (1)

- Thesis System DocumentationDocument5 pagesThesis System Documentationfc3kh880100% (2)

- PHD Thesis On Mobile BankingDocument5 pagesPHD Thesis On Mobile BankingWriteMyPaperCanadaLubbock100% (3)

- SSRN-id3107182Document76 pagesSSRN-id3107182Kiều Lê Nhật ĐôngNo ratings yet

- Sample Thesis Data Analysis and InterpretationDocument8 pagesSample Thesis Data Analysis and Interpretationnicolesavoielafayette100% (2)

- J Accinf 2008 06 001Document14 pagesJ Accinf 2008 06 001jinNo ratings yet

- Conell Price CVDocument3 pagesConell Price CVLynn Conell-PriceNo ratings yet

- Kuali Research NeedsDocument71 pagesKuali Research NeedsADELIA FILDZAH NADHILAHNo ratings yet

- Understanding The Importance & Impact of Technology in An AccountDocument31 pagesUnderstanding The Importance & Impact of Technology in An Accounttaehyung kimNo ratings yet

- Research Paper Topics For Business StatisticsDocument8 pagesResearch Paper Topics For Business Statisticssemizizyvyw3100% (1)

- Victoria University Thesis SubmissionDocument8 pagesVictoria University Thesis Submissionxmlzofhig100% (1)

- Big Data Literature ReviewDocument5 pagesBig Data Literature Reviewafmztsqbdnusia100% (1)

- BDAC FPER RBV Most CitationsDocument37 pagesBDAC FPER RBV Most CitationssherazNo ratings yet

- How To Present Data Analysis in Research PaperDocument7 pagesHow To Present Data Analysis in Research PapergqsrcuplgNo ratings yet

- Online Early - Preprint of Accepted ManuscriptDocument68 pagesOnline Early - Preprint of Accepted ManuscriptD ANo ratings yet

- Business Analytics Communicating With Numbers 1E 1St Edition Sanjiv Jaggia Full ChapterDocument67 pagesBusiness Analytics Communicating With Numbers 1E 1St Edition Sanjiv Jaggia Full Chaptermichael.lynch155100% (5)

- Ngovinda@nmsu EduDocument17 pagesNgovinda@nmsu Edusuljo atlagicNo ratings yet

- Thesis Presentation Analysis and Interpretation of DataDocument5 pagesThesis Presentation Analysis and Interpretation of Dataavismalavebridgeport100% (2)

- The Need For Skeptical' Accountants in The Era of Big Data PDFDocument18 pagesThe Need For Skeptical' Accountants in The Era of Big Data PDFDeanne ColeenNo ratings yet

- Business Analytics - FoundationDocument12 pagesBusiness Analytics - FoundationNishchay Edmund PaschalNo ratings yet

- Bouten Cho Michelon RobertsDocument57 pagesBouten Cho Michelon Robertstijis25390No ratings yet

- Online Enrollment System Thesis Related LiteratureDocument6 pagesOnline Enrollment System Thesis Related LiteratureBuyingPapersOnlineCollegeCanada100% (2)

- Accounting RankingsDocument29 pagesAccounting RankingsasaNo ratings yet

- S06-Management Deception PDFDocument64 pagesS06-Management Deception PDFanderson oliveiraNo ratings yet

- CSR Dissertation QuestionsDocument5 pagesCSR Dissertation QuestionsWriteMyPaperCanadaSingapore100% (1)

- Quantitative Data Analysis Literature ReviewDocument4 pagesQuantitative Data Analysis Literature Reviewafmzbufoeifoof100% (1)

- Research Paper of Management AccountingDocument5 pagesResearch Paper of Management Accountingskpcijbkf100% (1)

- Mba Thesis PDF DownloadDocument4 pagesMba Thesis PDF Downloadwhitneyturnerlittlerock100% (2)

- Minding the Machines: Building and Leading Data Science and Analytics TeamsFrom EverandMinding the Machines: Building and Leading Data Science and Analytics TeamsNo ratings yet

- Guidelines For Conducting Mixed-Methods ResearchDocument60 pagesGuidelines For Conducting Mixed-Methods Researchlive roseNo ratings yet

- The Delphi Method As A Research Tool: An Example, Design Considerations and ApplicationsDocument20 pagesThe Delphi Method As A Research Tool: An Example, Design Considerations and ApplicationsRishelle BelardoNo ratings yet

- A Meta-Analysis Based Modified Unified Theory of Acceptance and Use (Meta-Utaut) - AreviewDocument9 pagesA Meta-Analysis Based Modified Unified Theory of Acceptance and Use (Meta-Utaut) - Areviewlive roseNo ratings yet

- Enablers and Inhibitors of AI-Powered Voice Assistants A Dual-Factor Approach by Integrating The StaDocument22 pagesEnablers and Inhibitors of AI-Powered Voice Assistants A Dual-Factor Approach by Integrating The Stalive roseNo ratings yet

- Preparing and Conducting Interviews To Collect DataDocument11 pagesPreparing and Conducting Interviews To Collect Datalive roseNo ratings yet

- Preparing and Conducting Interviews To Collect DataDocument11 pagesPreparing and Conducting Interviews To Collect Datalive roseNo ratings yet

- John Cockerill Industry BrochureDocument15 pagesJohn Cockerill Industry BrochureEstelle CordeiroNo ratings yet

- Entrepreneurship: It Is A Strategic Process of Innovation & New Venture CreationDocument23 pagesEntrepreneurship: It Is A Strategic Process of Innovation & New Venture CreationsalsabilNo ratings yet

- Typeform Invoice BTLWMgTYQCPq91RjvDocument1 pageTypeform Invoice BTLWMgTYQCPq91RjvAakash vermaNo ratings yet

- Toppan Merrill Technology ListDocument2 pagesToppan Merrill Technology ListKilty ONealNo ratings yet

- Coti GIW Rep 26x28LSA PDFDocument3 pagesCoti GIW Rep 26x28LSA PDFjohan diazNo ratings yet

- Math 2nd Grading 1st SummativeDocument4 pagesMath 2nd Grading 1st SummativeAubrey Gay SarabosquezNo ratings yet

- Module 3Document79 pagesModule 3kakimog738No ratings yet

- QC Senior Compliance Attorney in Washington DC Resume Tina GreeneDocument2 pagesQC Senior Compliance Attorney in Washington DC Resume Tina GreeneTinaGreeneNo ratings yet

- Parag FoodsDocument122 pagesParag FoodsKamalapati BeheraNo ratings yet

- Proof of Residence LeaseDocument13 pagesProof of Residence Leaseapi-366174595No ratings yet

- L.C.Gupta Committee PurposeDocument3 pagesL.C.Gupta Committee PurposeAbhishek Kumar SinghNo ratings yet

- e-StatementBRImo 585401009753509 Jul2023 20230731 081457Document2 pagese-StatementBRImo 585401009753509 Jul2023 20230731 08145709. BUNGA NUR YUNITA SARINo ratings yet

- BO - Code BO - Name BO - Add BO - Pin Div - Code Div - NameDocument20 pagesBO - Code BO - Name BO - Add BO - Pin Div - Code Div - NameSuvashreePradhan100% (1)

- Customer Satisfaction Analysis For A Service Industry of Al-Arafah Islami Bank LimitedDocument25 pagesCustomer Satisfaction Analysis For A Service Industry of Al-Arafah Islami Bank LimitedOmor FarukNo ratings yet

- LEGAL ETHICS. Canon 2Document27 pagesLEGAL ETHICS. Canon 25h1tfac3No ratings yet

- State of Afghan Cities 2015 Volume - 1Document156 pagesState of Afghan Cities 2015 Volume - 1United Nations Human Settlements Programme (UN-HABITAT)No ratings yet

- Invitation To CPD On Predicting Corporate FailureDocument6 pagesInvitation To CPD On Predicting Corporate Failureyakubu I saidNo ratings yet

- Manager Yun Chen enDocument14 pagesManager Yun Chen enAleksandra MarkovaNo ratings yet

- What Is SIMBOX?Document6 pagesWhat Is SIMBOX?Ayoub ZahraouiNo ratings yet

- Master in Business Administration: Join Our Global CommunityDocument8 pagesMaster in Business Administration: Join Our Global Communityfrans1593No ratings yet

- Sample Business Impact AssessmentDocument2 pagesSample Business Impact AssessmentbdfbgrdfbbuiwefNo ratings yet

- Study Regarding Innovation and Entrepreneurship in Romanian SmesDocument6 pagesStudy Regarding Innovation and Entrepreneurship in Romanian SmesAlex ObrejanNo ratings yet

- 30 Pantry Organization Ideas and Tricks - How To Organize A PantryDocument1 page30 Pantry Organization Ideas and Tricks - How To Organize A PantryCKNo ratings yet

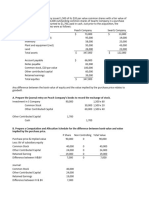

- Consolidated Financial Statement Excercise 3-4Document2 pagesConsolidated Financial Statement Excercise 3-4Winnie TanNo ratings yet

- Practice Question (Accounting Cycle) With Solution v2Document17 pagesPractice Question (Accounting Cycle) With Solution v2Laiba ManzoorNo ratings yet

- Consumer Behaviour Swiggy ZomatoDocument11 pagesConsumer Behaviour Swiggy ZomatowhoreNo ratings yet

- SIP Report Atharva SableDocument68 pagesSIP Report Atharva Sable7s72p3nswtNo ratings yet

- 18mel76 CimDocument4 pages18mel76 CimSushant NaikNo ratings yet