You might also like

- Oil & Gas Basics - JP Morgan (2008) PDFDocument73 pagesOil & Gas Basics - JP Morgan (2008) PDFTom van den BeltNo ratings yet

- Oil PricesDocument19 pagesOil PricesAjay KumarNo ratings yet

- Opec-Organization of Petroleum Exporting CountriesDocument32 pagesOpec-Organization of Petroleum Exporting Countriesavniattu100% (1)

- Oil - Infrastructure: D.K.Raghuwanshi Natasha Verma Parag Udas Sushil Tandon Surajit BahulikarDocument68 pagesOil - Infrastructure: D.K.Raghuwanshi Natasha Verma Parag Udas Sushil Tandon Surajit Bahulikarpranjal92pandeyNo ratings yet

- Oil Benchmarks: Implications & OpportunitiesDocument41 pagesOil Benchmarks: Implications & Opportunitiesmbw000012378No ratings yet

- SM TPDocument17 pagesSM TPdineshneruNo ratings yet

- Understanding Crude Oil and Product Markets Primer Low PDFDocument39 pagesUnderstanding Crude Oil and Product Markets Primer Low PDFrohanpujari100% (1)

- Covid 19Document11 pagesCovid 19namratagadkari03No ratings yet

- Namrata Gadkari Covid19 IMTDocument11 pagesNamrata Gadkari Covid19 IMTnamratagadkari05No ratings yet

- Galloping Oil PricesDocument17 pagesGalloping Oil Pricesashi_89No ratings yet

- Crude Oil Analysis by MACD Model Name: Institutional AffiliationDocument23 pagesCrude Oil Analysis by MACD Model Name: Institutional AffiliationmagdalineNo ratings yet

- Introduction Crude OilDocument13 pagesIntroduction Crude OilrohanpujariNo ratings yet

- TILOK Covid19Document7 pagesTILOK Covid19anshul singhalNo ratings yet

- Spe 1015 0004 Ogf PDFDocument2 pagesSpe 1015 0004 Ogf PDFWisnu ArdhiNo ratings yet

- Group Project - Sensitivity AnalysisDocument8 pagesGroup Project - Sensitivity AnalysisSalomon Cure CorreaNo ratings yet

- BE OPEC PriadarshiniDocument6 pagesBE OPEC PriadarshiniPriadarshini Subramanyam DM21B093No ratings yet

- Valuation of Oil CompaniesDocument48 pagesValuation of Oil CompaniesSnehil Tripathi100% (1)

- Oil & Gas AnalysisDocument98 pagesOil & Gas AnalysisNitin Kr banka67% (3)

- Getting Petroleum Products To Market: Crude Oil SupplyDocument4 pagesGetting Petroleum Products To Market: Crude Oil SupplySameer YounusNo ratings yet

- Crude OilDocument13 pagesCrude OilRajesh Kumar RoutNo ratings yet

- Oil & Gas Contracrs 2Document75 pagesOil & Gas Contracrs 2Manus AgereNo ratings yet

- International Oil Market and Oil Trading: Litasco SaDocument15 pagesInternational Oil Market and Oil Trading: Litasco Sasushilk28No ratings yet

- Oil and Gas Industry: An Analysis of Global Trends and the Indian ScenarioDocument5 pagesOil and Gas Industry: An Analysis of Global Trends and the Indian ScenarioAnurag KhandelwalNo ratings yet

- Basic Principles of Petroleum 7Document5 pagesBasic Principles of Petroleum 7Sunil GoriahNo ratings yet

- Energy: A Global Scan From Bangladesh Perspective: Mohammad TamimDocument59 pagesEnergy: A Global Scan From Bangladesh Perspective: Mohammad TamimRashidul Islam MasumNo ratings yet

- Causes and Impacts of Crude Oil Price VolatilityDocument83 pagesCauses and Impacts of Crude Oil Price Volatilityadhia_saurabh100% (1)

- Crude Oil Prices and FactorsDocument15 pagesCrude Oil Prices and FactorsGirish1412No ratings yet

- Supply and Demand of Tanker MarketDocument21 pagesSupply and Demand of Tanker MarketHamad Bakar Hamad100% (1)

- Oil PricingDocument68 pagesOil Pricingyash saragiya100% (2)

- Crude OilDocument35 pagesCrude OilNeha VoraNo ratings yet

- Commodities Market: Crude OilDocument20 pagesCommodities Market: Crude OilgracelillyNo ratings yet

- Oil prices under covid-19 rolesDocument19 pagesOil prices under covid-19 rolesAhmed JafferNo ratings yet

- Sukhvinderkaur_Covid19Document18 pagesSukhvinderkaur_Covid19sukhvindertaakNo ratings yet

- Intternational FinanceDocument23 pagesIntternational FinancessamminaNo ratings yet

- Petroleum Fiscal Systems Nigeria - UKDocument51 pagesPetroleum Fiscal Systems Nigeria - UKJaysonn KayNo ratings yet

- Assignment # 1 - PENG 6011Document12 pagesAssignment # 1 - PENG 6011Sachin MaharajNo ratings yet

- SPE 92888 OPEC: Floating Supply For A Balanced & Stable Market, Part IDocument6 pagesSPE 92888 OPEC: Floating Supply For A Balanced & Stable Market, Part Imsmsoft90No ratings yet

- Case StudyDocument14 pagesCase StudyBhavik RathodNo ratings yet

- The Dawn of A New Era For US Energy: Fact, Fiction and The Investment Case For MLPs in Public Retirement PlansDocument61 pagesThe Dawn of A New Era For US Energy: Fact, Fiction and The Investment Case For MLPs in Public Retirement PlansPointeCapitalNo ratings yet

- Crude Oil Forecast: Q2 2020: Christopher Vecchio, Cfa, Senior Strategist Rich Dvorak, AnalystDocument8 pagesCrude Oil Forecast: Q2 2020: Christopher Vecchio, Cfa, Senior Strategist Rich Dvorak, AnalystBob BlythNo ratings yet

- Petro Retailing BusinessDocument117 pagesPetro Retailing BusinessPavan Kumar ChNo ratings yet

- CaseOPECandtheWorldMarket 6c063fa4 663c 41fa 8bf9 F9a504ac665c 36843Document2 pagesCaseOPECandtheWorldMarket 6c063fa4 663c 41fa 8bf9 F9a504ac665c 36843Its SabinNo ratings yet

- Petroleum Product Pricing MechanismDocument20 pagesPetroleum Product Pricing MechanismSonu PatelNo ratings yet

- Oil ETF GuideDocument1 pageOil ETF GuideTe-yu OuNo ratings yet

- Oil & Gas Report Sector - IndiaDocument10 pagesOil & Gas Report Sector - IndiaDada_bitsNo ratings yet

- Covid19 Submission TemplateDocument8 pagesCovid19 Submission Templatevijay anandNo ratings yet

- Oil Price Benchmarks: Legal DisclaimerDocument53 pagesOil Price Benchmarks: Legal Disclaimersushilk28No ratings yet

- Pakistan State Oil (PSO) Industry and Financial (Ratio) AnalysisDocument13 pagesPakistan State Oil (PSO) Industry and Financial (Ratio) Analysism.tarik88% (8)

- IMT Covid19 PDFDocument6 pagesIMT Covid19 PDFbetter traderNo ratings yet

- Task 2 - ImplementationDocument6 pagesTask 2 - ImplementationIndianagrofarmsNo ratings yet

- TheoilsectorDocument24 pagesTheoilsectorjamilkhannNo ratings yet

- Oil Price Report Analysis of Supply, Demand, and EconomyDocument12 pagesOil Price Report Analysis of Supply, Demand, and EconomyShivank JasoriaNo ratings yet

- International Oil Market-Final - Part One FinalDocument26 pagesInternational Oil Market-Final - Part One FinalMora MikhailNo ratings yet

- Getting Petroleum Products to Market: A Brief Overview of the Supply ChainDocument4 pagesGetting Petroleum Products to Market: A Brief Overview of the Supply ChainSon GokuNo ratings yet

- Transocean, Inc (RIG) : HFAC Stock Pitch April 24th, 2008Document28 pagesTransocean, Inc (RIG) : HFAC Stock Pitch April 24th, 2008MohamedSaidNo ratings yet

- Rise & Impact of Crude Oil Price in IndiaDocument10 pagesRise & Impact of Crude Oil Price in IndiaRandal SchroederNo ratings yet

- Refinery MarketDocument4 pagesRefinery MarketAsif KhanNo ratings yet

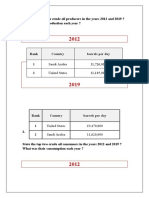

- State The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?Document6 pagesState The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?laoy aolNo ratings yet

- Oil's Endless Bid: Taming the Unreliable Price of Oil to Secure Our EconomyFrom EverandOil's Endless Bid: Taming the Unreliable Price of Oil to Secure Our EconomyNo ratings yet

- An Introduction to Petroleum Technology, Economics, and PoliticsFrom EverandAn Introduction to Petroleum Technology, Economics, and PoliticsNo ratings yet

- Coca-Cola Financial AnalysisDocument6 pagesCoca-Cola Financial AnalysisAditya Pal Singh Mertia RMNo ratings yet

- Astra Microwave Products LTD PDFDocument4 pagesAstra Microwave Products LTD PDFAwakash DixitNo ratings yet

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- A Study on Assets Management by Mutual Fund in India with Special Reference to Kotak Mahindra Asset Management CompanyDocument71 pagesA Study on Assets Management by Mutual Fund in India with Special Reference to Kotak Mahindra Asset Management CompanyShailesh Bandooni50% (2)

- Dividend Growth Model Valuation of ToysRusDocument5 pagesDividend Growth Model Valuation of ToysRusIrinaHaqueNo ratings yet

- Ratio Analysis of VoltasDocument11 pagesRatio Analysis of Voltasriya guptaNo ratings yet

- Citigroup - Hot Corporate Finance Topics in 2006Document36 pagesCitigroup - Hot Corporate Finance Topics in 2006darkstar314No ratings yet

- Zomato - Detailed IPODocument11 pagesZomato - Detailed IPOsaurabhNo ratings yet

- Financial Analysis of Himalayan BankDocument31 pagesFinancial Analysis of Himalayan Banksuraj banNo ratings yet

- Capital StructureDocument11 pagesCapital StructureSathya Bharathi100% (1)

- Nov Dec3rd VTH Sem 2021Document25 pagesNov Dec3rd VTH Sem 2021Anushka MalikNo ratings yet

- Charles Ega 3203017162 Case Study Working Capital Management Assessing Roche Publishing Companys Cash Management EfficiencyDocument4 pagesCharles Ega 3203017162 Case Study Working Capital Management Assessing Roche Publishing Companys Cash Management EfficiencyCharles 10No ratings yet

- How To Become Rich and Happy: by Prasenjit Kumar PaulDocument22 pagesHow To Become Rich and Happy: by Prasenjit Kumar PaulSatish KumarNo ratings yet

- GARP 2023 FRM PART I-Book 3 - Financial Markets and ProductsDocument298 pagesGARP 2023 FRM PART I-Book 3 - Financial Markets and Productsivan arista100% (1)

- Avoid Bases That Make Too Deep A DropDocument2 pagesAvoid Bases That Make Too Deep A DropAndraReiNo ratings yet

- NSE Lecture NotesDocument10 pagesNSE Lecture NotesarmailgmNo ratings yet

- CBSE Class 12 Accountancy Accounting For Share Capital and Debenture WorksheetDocument3 pagesCBSE Class 12 Accountancy Accounting For Share Capital and Debenture WorksheetJenneil CarmichaelNo ratings yet

- Launch Offshore Hedge Fund With TopAUM - Com and Tyler Capital GroupDocument5 pagesLaunch Offshore Hedge Fund With TopAUM - Com and Tyler Capital GroupJonathan T BuffaNo ratings yet

- Mindshift ChallengeDocument94 pagesMindshift ChallengeSerene Heather Renze100% (6)

- Rootstock SCI Worldwide Flexible Fund - Minimum Disclosure DocumentDocument4 pagesRootstock SCI Worldwide Flexible Fund - Minimum Disclosure DocumentMartin NelNo ratings yet

- Ifm Formula Sheet - Quantitative FinanceDocument22 pagesIfm Formula Sheet - Quantitative FinanceschuylerNo ratings yet

- (Lecture 1 & 2) - Introduction To Investment Appraisal MethodsDocument21 pages(Lecture 1 & 2) - Introduction To Investment Appraisal MethodsAjay Kumar Takiar100% (1)

- Webinar Ppt-23rd AugustDocument120 pagesWebinar Ppt-23rd AugustPraveen B100% (5)

- State Bank of India: Balance Sheet As On 31 March, 2018Document103 pagesState Bank of India: Balance Sheet As On 31 March, 2018Anonymous ckTjn7RCq8No ratings yet

- FM303 Tutorial Question Week 5Document3 pagesFM303 Tutorial Question Week 5Smriti LalNo ratings yet

- STA Guide - 2016Document3 pagesSTA Guide - 2016luis antonioNo ratings yet

- Ftee 101 13Document6 pagesFtee 101 13shenalifernando199No ratings yet

- NISM VA Chapter Wise QuestionsDocument45 pagesNISM VA Chapter Wise QuestionsAvinash JainNo ratings yet

- New Trends in Energy DerivativesDocument33 pagesNew Trends in Energy DerivativesakwoviahNo ratings yet

- Horizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2BDocument10 pagesHorizontal and Vertical Analaysis: Karysse Arielle Noel Jalao Financial Management Bsac-2BKarysse Arielle Noel JalaoNo ratings yet