You might also like

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- Chapter 4 - Equity Markets - 2023Document32 pagesChapter 4 - Equity Markets - 202305 Phạm Hồng Diệp12.11No ratings yet

- Topic 3 - Share MarketDocument39 pagesTopic 3 - Share MarketMiera FrnhNo ratings yet

- Chapter 4Document104 pagesChapter 4biruhtesfabrightfutureNo ratings yet

- Accounting For Companies: BCM 1204: Accounting in Business IiDocument49 pagesAccounting For Companies: BCM 1204: Accounting in Business IiMaryjoy KilonzoNo ratings yet

- Accounting For Companies-1Document50 pagesAccounting For Companies-1daniel.maina2005No ratings yet

- Fin358 Individual AssignmentDocument10 pagesFin358 Individual AssignmentMūhãmmâd Åïmãñ Bïn ÂbddūllähNo ratings yet

- Capital MarketDocument12 pagesCapital MarketCma Sayeed InamdarNo ratings yet

- Capital Market OperationsDocument120 pagesCapital Market OperationsmanjapcNo ratings yet

- Investment Analysis - Chapter 2Document26 pagesInvestment Analysis - Chapter 2Linh MaiNo ratings yet

- MGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIDocument86 pagesMGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIIsmadth2918388No ratings yet

- Managerial Finance chp7Document11 pagesManagerial Finance chp7Linda Mohammad FarajNo ratings yet

- Institute: Usb Department: Bba Bachelor of Business AdministrationDocument27 pagesInstitute: Usb Department: Bba Bachelor of Business AdministrationPankajNo ratings yet

- Money Equity and Credit MarketsDocument32 pagesMoney Equity and Credit MarketsAbhijeet BhattacharyaNo ratings yet

- Chapter 5. Equity MarketsDocument150 pagesChapter 5. Equity MarketsHiếu Nhi TrịnhNo ratings yet

- Investment Models 13 - Spring 2021Document37 pagesInvestment Models 13 - Spring 2021Y HNo ratings yet

- M3 - Sources of FinanceDocument22 pagesM3 - Sources of Financehats300972No ratings yet

- Indian Equity MarketDocument26 pagesIndian Equity Marketnavu811No ratings yet

- Business Environment Chapter 07 Stock Exchanges in in Dia 1Document23 pagesBusiness Environment Chapter 07 Stock Exchanges in in Dia 1himanshu_choudhary_2No ratings yet

- Equity Securities MarketDocument23 pagesEquity Securities MarketILOVE MATURED FANSNo ratings yet

- FMI-Lecture5-Stock MarketDocument44 pagesFMI-Lecture5-Stock MarketFariha KhanNo ratings yet

- Part 4 Chapter 10 11 12 FmiDocument76 pagesPart 4 Chapter 10 11 12 FmiEffie Erica MacachorNo ratings yet

- Stock ValuationDocument46 pagesStock Valuationbisma9681No ratings yet

- International Capital Market Case Study - Part 1. Basic Knowledge of Capital MarketDocument27 pagesInternational Capital Market Case Study - Part 1. Basic Knowledge of Capital Marketmanojbhatia1220No ratings yet

- Chapter 7 Mutual FundsDocument28 pagesChapter 7 Mutual FundsMOHAMMAD BORENENo ratings yet

- Secondary Markets: Presented byDocument22 pagesSecondary Markets: Presented bytricha5605No ratings yet

- Fmi Unit 3Document26 pagesFmi Unit 3Cabdixakiim-Tiyari Cabdillaahi AadenNo ratings yet

- Indian Financial Instruments PDFDocument33 pagesIndian Financial Instruments PDFPraveen SinghNo ratings yet

- Fim - 5 Equity MarketDocument15 pagesFim - 5 Equity MarketgashukelilNo ratings yet

- Equity MarketDocument38 pagesEquity MarketEllah MaeNo ratings yet

- Capital Market: Unit II: PrimaryDocument55 pagesCapital Market: Unit II: PrimaryROHIT CHHUGANI 1823160No ratings yet

- Mutual Funds and Other Investment CompaniesDocument51 pagesMutual Funds and Other Investment CompaniesNaeemNo ratings yet

- Corporate Structure and AdministrationDocument10 pagesCorporate Structure and AdministrationDr.Sree Lakshmi KNo ratings yet

- Capital MarketsDocument16 pagesCapital MarketsChowdary PurandharNo ratings yet

- Jaiib - A 4 Capital Market PPBDocument48 pagesJaiib - A 4 Capital Market PPBKumar JayantNo ratings yet

- FM ReviewerDocument20 pagesFM ReviewerBSA - Cabangon, MerraquelNo ratings yet

- Share and Its Types, Primary and Secondary Market: Objective& Student's OutcomeDocument7 pagesShare and Its Types, Primary and Secondary Market: Objective& Student's OutcomeSethu RNo ratings yet

- Chapter 10b Long Term Finance - EquityDocument27 pagesChapter 10b Long Term Finance - EquityIvy CheekNo ratings yet

- Personal Finance Chapter 14 Part 1: CanadayDocument25 pagesPersonal Finance Chapter 14 Part 1: Canaday陈皮乌鸡No ratings yet

- An ktTqOHRIf AJ3tOuJHqn15ak r4I2mbWaf3kACa5l - NxypPFp4Ufq5 u4Ay5Ldq9UOdHTxbXPJ01LzWvsjVRHa7YzF0N 7Q3Jusa - to7rpMlFJFmBmJHhZjng5ADocument60 pagesAn ktTqOHRIf AJ3tOuJHqn15ak r4I2mbWaf3kACa5l - NxypPFp4Ufq5 u4Ay5Ldq9UOdHTxbXPJ01LzWvsjVRHa7YzF0N 7Q3Jusa - to7rpMlFJFmBmJHhZjng5AHari RNo ratings yet

- Investment Analysis and Portfolio Management: Security Markets - 1Document29 pagesInvestment Analysis and Portfolio Management: Security Markets - 1RakibImtiaz100% (1)

- General Mathematics: Activity #5 2 QuarterDocument18 pagesGeneral Mathematics: Activity #5 2 QuarterChosen Josiah HuertaNo ratings yet

- Stock Valuation Module 4.2Document98 pagesStock Valuation Module 4.2Jemille MangawanNo ratings yet

- MB II Unit Final StudentsDocument70 pagesMB II Unit Final StudentsHema vijay sNo ratings yet

- Group 1 A Stock and Bond MarketDocument16 pagesGroup 1 A Stock and Bond MarketClarky LinguisNo ratings yet

- Updated-Chp3-Direct Vs Indirect InvestingDocument24 pagesUpdated-Chp3-Direct Vs Indirect InvestingQais Qazi ZadaNo ratings yet

- Topic 2 - Long Term FinDocument25 pagesTopic 2 - Long Term FinAina KhairunnisaNo ratings yet

- Wealth Management and Personal Financial Planning 8-10 1.PptmDocument86 pagesWealth Management and Personal Financial Planning 8-10 1.PptmHargobind CoachNo ratings yet

- Mutual Funds and Other Investment CompaniesDocument5 pagesMutual Funds and Other Investment Companiespiepkuiken-knipper0jNo ratings yet

- Equity Market 1Document39 pagesEquity Market 1Rohit KattamuriNo ratings yet

- Lecture 3 Equity Market 1 PDFDocument39 pagesLecture 3 Equity Market 1 PDFJoannaNo ratings yet

- Far 410: Chapter 4: EquityDocument44 pagesFar 410: Chapter 4: EquityJung KookieNo ratings yet

- Group 7Document2 pagesGroup 7Gia BảoNo ratings yet

- Securities: Types, Features and Concepts of Asset Allocation and InvestingDocument8 pagesSecurities: Types, Features and Concepts of Asset Allocation and InvestingSandhya Darshan DasNo ratings yet

- Mutual Funds and Other Investment Companies: Bodie, Kane and MarcusDocument20 pagesMutual Funds and Other Investment Companies: Bodie, Kane and MarcusMd TowkikNo ratings yet

- Summary Sheet - Helpful For Retention For Equity MarketsDocument19 pagesSummary Sheet - Helpful For Retention For Equity Marketsdevesh chaudharyNo ratings yet

- Ch.9 - Shareholders' Equity - MHDocument41 pagesCh.9 - Shareholders' Equity - MHSamZhaoNo ratings yet

- Securities Market The BattlefieldDocument14 pagesSecurities Market The BattlefieldJagrityTalwarNo ratings yet

- VeenaDocument18 pagesVeenaveena_1585No ratings yet

- Chapter 9 UpdatedDocument9 pagesChapter 9 UpdatedabdulraufdghaybeejNo ratings yet

- Financial Statements TemplateDocument17 pagesFinancial Statements Templatevaddana haisocheatNo ratings yet

- Money Banking and Financial Markets 6E Ise 6Th Edition Stephen G Cecchetti Full ChapterDocument67 pagesMoney Banking and Financial Markets 6E Ise 6Th Edition Stephen G Cecchetti Full Chapterjessica.whitley68693% (14)

- BrochureDocument20 pagesBrochurenirmal sridharNo ratings yet

- Cost of CapitalDocument42 pagesCost of CapitalimasikudenisiahNo ratings yet

- ICAN SFM Past Questions 2014 - Nov 2023Document734 pagesICAN SFM Past Questions 2014 - Nov 2023Abdulsalam JubrilNo ratings yet

- DERVFOP - Lecture 3 (Hedging Strategies Using Futures)Document29 pagesDERVFOP - Lecture 3 (Hedging Strategies Using Futures)RedNo ratings yet

- Indonesia Lending and Secured Finance - Legal 500 - 2023Document7 pagesIndonesia Lending and Secured Finance - Legal 500 - 2023Cesar Elias SanjurNo ratings yet

- A Simple Approximation of Tobin's QDocument6 pagesA Simple Approximation of Tobin's Qwxmnxfm57wNo ratings yet

- Section 2Document2 pagesSection 2MariamHatemNo ratings yet

- V & Vi Bcom Regular Syllabus Final Nep 17-9-2023 Bos ApprovedDocument48 pagesV & Vi Bcom Regular Syllabus Final Nep 17-9-2023 Bos ApprovedChethan MallikarjunNo ratings yet

- Investor Compass September 2022Document4 pagesInvestor Compass September 2022Stefan GraterNo ratings yet

- Tax - 2nd Monthly Assessment - QuestionsDocument12 pagesTax - 2nd Monthly Assessment - QuestionsGRACELYN SOJORNo ratings yet

- Trend AnalysisDocument1 pageTrend Analysisangel caoNo ratings yet

- Paytm 2Document5 pagesPaytm 2V KaviyaNo ratings yet

- Life Insurance Handbook (English)Document12 pagesLife Insurance Handbook (English)Satyam MittalNo ratings yet

- Afar - Corporate LiquidationDocument2 pagesAfar - Corporate Liquidationfarah mae raquinioNo ratings yet

- Valenci Group PresentationDocument39 pagesValenci Group PresentationAli AbdulazizNo ratings yet

- Ha 3 2023Document3 pagesHa 3 2023xbdrsk6fbgNo ratings yet

- ACCA F7 Mock Exam 1 AnswersDocument11 pagesACCA F7 Mock Exam 1 Answershunaid.ayeshaNo ratings yet

- Foreign Exchange Dissertation TopicsDocument7 pagesForeign Exchange Dissertation TopicsBuyPapersOnlineBaltimore100% (1)

- How Can Your ETRM / CTRM Solution Help With CreditDocument7 pagesHow Can Your ETRM / CTRM Solution Help With CreditCTRM CenterNo ratings yet

- B03013 Class3 TimeValueofMoneyDocument20 pagesB03013 Class3 TimeValueofMoneyLâm Thị Như ÝNo ratings yet

- Cash Answer KeyDocument14 pagesCash Answer KeyRdeeeNo ratings yet

- Handbook of Equity Jurisprudence - Eaton 1901Document46 pagesHandbook of Equity Jurisprudence - Eaton 1901Monique NavesNo ratings yet

- Forex Trend Line Strategy CLBDocument82 pagesForex Trend Line Strategy CLBNanté RznNo ratings yet

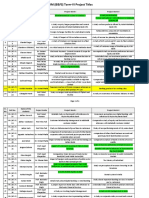

- PGDM (B&FS) Project Titles-1Document5 pagesPGDM (B&FS) Project Titles-1PranitNo ratings yet

- LKP Securities Limited Corporate PresentationDocument20 pagesLKP Securities Limited Corporate PresentationChaitanya TaloleNo ratings yet

- Herding Behavior in The Stock Market of BangladeshDocument19 pagesHerding Behavior in The Stock Market of BangladeshAman BaigNo ratings yet

- Business and Accounting Studies - Grade 11 Worksheet 5: Record The Below Transactions in AccountsDocument2 pagesBusiness and Accounting Studies - Grade 11 Worksheet 5: Record The Below Transactions in AccountsDinukshiya SelvaduraiNo ratings yet