You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Session 7Document20 pagesSession 7Hamza BennisNo ratings yet

- Tutorial 2 - SolutionsDocument15 pagesTutorial 2 - SolutionsLijing CheNo ratings yet

- Solutions For CH 9 2-26-14Document15 pagesSolutions For CH 9 2-26-14Rafael Ricardo VilleroNo ratings yet

- Solution Cost and Management AccountingDocument7 pagesSolution Cost and Management AccountingbillNo ratings yet

- Static and Flexible Budget ExampleDocument12 pagesStatic and Flexible Budget ExampleAFSYARINA BT ZUNAIDI50% (2)

- Marginal and Absorption CostingDocument8 pagesMarginal and Absorption CostingEniola OgunmonaNo ratings yet

- Absorption Costing GclassDocument4 pagesAbsorption Costing GclassDoromal, Jerome A.No ratings yet

- Variable Costing April Revenues 8,400,000Document10 pagesVariable Costing April Revenues 8,400,000Hiền NguyễnNo ratings yet

- Adriel Company toy car costing and profit analysisDocument4 pagesAdriel Company toy car costing and profit analysisLerma MarianoNo ratings yet

- BFD Class NotesDocument20 pagesBFD Class NotesAnas KhanNo ratings yet

- OverheadsDocument22 pagesOverheadsOlha LNo ratings yet

- Application of Marginal Costing: Prof. Madhumathi Kristu Jayanti College BangaloreDocument10 pagesApplication of Marginal Costing: Prof. Madhumathi Kristu Jayanti College BangaloreMs. Madhumathi T KNo ratings yet

- ACC1511 MT Sem2 1516 AnswerDocument8 pagesACC1511 MT Sem2 1516 AnswerBeni ZakariaNo ratings yet

- AAMDocument7 pagesAAMsarah josephNo ratings yet

- AccountingDocument5 pagesAccountingAndrea Joy PekNo ratings yet

- Manufacturing Account (With Answers) : Advanced LevelDocument15 pagesManufacturing Account (With Answers) : Advanced LevelMomoh Kebiru0% (1)

- Marginal and Absorption Costing TechniqueDocument4 pagesMarginal and Absorption Costing TechniqueADEYANJU AKEEMNo ratings yet

- I. All Questions Are Compulsory. Ii. Q. 2 To Q. 6 Have Internal Options. Iii. Figures To The Right Indicate Full MarksDocument7 pagesI. All Questions Are Compulsory. Ii. Q. 2 To Q. 6 Have Internal Options. Iii. Figures To The Right Indicate Full MarksshrikantNo ratings yet

- Manufacturing A LevelDocument21 pagesManufacturing A LevelSheraz AhmadNo ratings yet

- Variable Costing and Absorption Costing AnalysisDocument6 pagesVariable Costing and Absorption Costing AnalysisNugrah LesmanaNo ratings yet

- Contribution Approach 2Document16 pagesContribution Approach 2kualler80% (5)

- Problem Unit 4Document7 pagesProblem Unit 4meenasaratha100% (1)

- Master Budget Formulas Module 6 Management AccountingDocument14 pagesMaster Budget Formulas Module 6 Management AccountingcykablyatNo ratings yet

- Lecture 1. Basic Costing CVPDocument14 pagesLecture 1. Basic Costing CVPTân NguyênNo ratings yet

- Cost Accounting: The Institute of Chartered Accountants of PakistanDocument4 pagesCost Accounting: The Institute of Chartered Accountants of PakistanShehrozSTNo ratings yet

- Cost AccountingDocument29 pagesCost Accountingsino akoNo ratings yet

- 160 P16MC42 2020061304365276Document11 pages160 P16MC42 2020061304365276Tithi jainNo ratings yet

- Absorption and Variable CostingDocument5 pagesAbsorption and Variable CostingKIM RAGANo ratings yet

- Exercises Absorption and Variable CostingPAUL ANTHONY DE JESUSDocument4 pagesExercises Absorption and Variable CostingPAUL ANTHONY DE JESUSMeng DanNo ratings yet

- Cost Accounting Test 2Document3 pagesCost Accounting Test 2Faizan Sir's TutorialsNo ratings yet

- Cost Acc Nov06Document27 pagesCost Acc Nov06api-3825774No ratings yet

- AFAR Pre-Board - Set B Overhead Costing ProblemsDocument11 pagesAFAR Pre-Board - Set B Overhead Costing ProblemsRence Gonzales0% (2)

- Understand Variance Analysis for Improved Managerial Decision MakingDocument92 pagesUnderstand Variance Analysis for Improved Managerial Decision MakingChezka HerminigildoNo ratings yet

- Assgnment 2 (f5) 10341Document11 pagesAssgnment 2 (f5) 10341Minhaj AlbeezNo ratings yet

- TUT 3 - Relevant Information&decision MakingDocument10 pagesTUT 3 - Relevant Information&decision MakingKim Chi LeNo ratings yet

- Try Yourself: Q. No.10 The Following Information Is Given by Z LTDDocument2 pagesTry Yourself: Q. No.10 The Following Information Is Given by Z LTDAnkit Jung RayamajhiNo ratings yet

- About MyselfDocument2 pagesAbout MyselfAnkit Jung RayamajhiNo ratings yet

- Flexible Budget SolutionsDocument16 pagesFlexible Budget Solutionscijasa7002No ratings yet

- Accounting Assignment CardiffDocument12 pagesAccounting Assignment CardiffpavanihirushaNo ratings yet

- Exercise 7-3 To 7-6Document6 pagesExercise 7-3 To 7-6Nhel AlvaroNo ratings yet

- Module 5 AssignmentDocument5 pagesModule 5 AssignmentMayNo ratings yet

- Just in Time and Backflush Costing With Illustrative Problem Docx Compress 1Document7 pagesJust in Time and Backflush Costing With Illustrative Problem Docx Compress 1Danica Kaye MorcellosNo ratings yet

- P1 Solution CMA JUNE 2020Document5 pagesP1 Solution CMA JUNE 2020Awal ShekNo ratings yet

- Cost Accounting: Rs. Rs. Rs. Rs. Rs. RsDocument8 pagesCost Accounting: Rs. Rs. Rs. Rs. Rs. RsShehrozSTNo ratings yet

- Final CMAC (NA) Midterm Solution Aut-23Document11 pagesFinal CMAC (NA) Midterm Solution Aut-23Hassan TanveerNo ratings yet

- Activity Based CostingDocument7 pagesActivity Based CostingCzar Ysmael RabayaNo ratings yet

- MAS.05 Drill Variable and Absorption CostingDocument5 pagesMAS.05 Drill Variable and Absorption Costingace ender zeroNo ratings yet

- Cost Behavior ExerciseDocument3 pagesCost Behavior ExerciseIftekhar Uddin M.D EisaNo ratings yet

- STANDARD COSTING (1)Document11 pagesSTANDARD COSTING (1)yatharthlmdNo ratings yet

- Prob 2Document2 pagesProb 2Elliot RichardNo ratings yet

- Tut 5_9.23Document4 pagesTut 5_9.23Thanh MaiNo ratings yet

- COAGA2 - Week 5 - Standard CostingDocument28 pagesCOAGA2 - Week 5 - Standard CostingAllen28No ratings yet

- Chapter 6 Accting For Spoilage, Defective Units & ScrapDocument33 pagesChapter 6 Accting For Spoilage, Defective Units & ScrapAlex HaymeNo ratings yet

- UTS AkutansiDocument24 pagesUTS AkutansiAbraham KristiyonoNo ratings yet

- JUST IN TIME AND BACKFLUSH COSTING With Illustrative ProblemDocument7 pagesJUST IN TIME AND BACKFLUSH COSTING With Illustrative Problemenzo0% (1)

- Variableabsorption CostingDocument77 pagesVariableabsorption Costingandrea arapocNo ratings yet

- Fundamentals of Variance AnalysisDocument22 pagesFundamentals of Variance Analysissalsabila ry1No ratings yet

- LEVEL 2 Online Quiz - Answers SET ADocument10 pagesLEVEL 2 Online Quiz - Answers SET AVincent Larrie MoldezNo ratings yet

- Session 12Document28 pagesSession 12Hamza BennisNo ratings yet

- Les Adjectifs Et Les Pronoms PossessifsDocument1 pageLes Adjectifs Et Les Pronoms PossessifsHamza BennisNo ratings yet

- Uvaf1349 PcsDocument17 pagesUvaf1349 PcsHamza BennisNo ratings yet

- Example Chapter 3Document6 pagesExample Chapter 3Hamza BennisNo ratings yet

- Continuous TimeDocument46 pagesContinuous TimeHamza BennisNo ratings yet

- Markov ChainsDocument54 pagesMarkov ChainsHamza BennisNo ratings yet

- Martingales ExplainedDocument46 pagesMartingales ExplainedHamza BennisNo ratings yet

- Accounting For ManagersDocument286 pagesAccounting For Managersritesh_aladdinNo ratings yet

- 1107-920-46-3559 e ADDENDUM2Document171 pages1107-920-46-3559 e ADDENDUM2asharani_ckNo ratings yet

- FMGT 2152 Team Project Report GuideDocument3 pagesFMGT 2152 Team Project Report GuideKCNo ratings yet

- Auditing 1 (ACMR 311) Week 6.Document26 pagesAuditing 1 (ACMR 311) Week 6.Ewhidar Yulis Ria La'iaNo ratings yet

- Practice Problem Set #5 - Adjusting Entries and Adjusted Trial BalanceDocument5 pagesPractice Problem Set #5 - Adjusting Entries and Adjusted Trial BalanceSHS, Marian PolancoNo ratings yet

- Objectives of Cost AccountingDocument2 pagesObjectives of Cost AccountingPatrice ScottNo ratings yet

- Reflective Excercise 1Document4 pagesReflective Excercise 1Raja SimhanNo ratings yet

- 151 0106Document37 pages151 0106api-27548664No ratings yet

- Accounting Compress PDFDocument9 pagesAccounting Compress PDFJade jade jadeNo ratings yet

- Debit and Credit EnteriesDocument18 pagesDebit and Credit EnteriesSuffian NaeemNo ratings yet

- Investigation StagesDocument4 pagesInvestigation StagesIbiaye Bob-manuelNo ratings yet

- Mind Map 5Document1 pageMind Map 5darylle roblesNo ratings yet

- Consolidation Q80Document5 pagesConsolidation Q80Nolan TitusNo ratings yet

- Solution Far450 UITM - Jan 2013Document8 pagesSolution Far450 UITM - Jan 2013Rosaidy SudinNo ratings yet

- Big Picture: Week 1-3: Unit Learning Outcomes (ULO) : at The End of The Unit, You AreDocument51 pagesBig Picture: Week 1-3: Unit Learning Outcomes (ULO) : at The End of The Unit, You Arekakao50% (2)

- Study Guide: Part One-Identifying Accounting TermsDocument4 pagesStudy Guide: Part One-Identifying Accounting TermsJames SargentNo ratings yet

- Hotel Audit Work ProgramDocument60 pagesHotel Audit Work ProgramJean-Paul Hazoume100% (4)

- Management Accounting SampleDocument29 pagesManagement Accounting SampleJamilah Edward100% (2)

- 80641Document25 pages80641Sita RamNo ratings yet

- Chapter 9 Final Accounts (With Adjustment)Document100 pagesChapter 9 Final Accounts (With Adjustment)priyam.200409No ratings yet

- Worksheet ProblemDocument4 pagesWorksheet Problemusernames358No ratings yet

- Ofag Fam 2019 FinalDocument161 pagesOfag Fam 2019 FinalHamse MahirNo ratings yet

- Far 1Document2 pagesFar 1Stephanie Jane0% (1)

- Analysis of Financial StatementsDocument7 pagesAnalysis of Financial StatementsThakur Anmol RajputNo ratings yet

- CMPR0102 318107922 PDFDocument1 pageCMPR0102 318107922 PDFratih kusumaNo ratings yet

- With Comparative Figures For CY 2010Document8 pagesWith Comparative Figures For CY 2010sandra bolokNo ratings yet

- Break-Even Analysis/Cvp AnalysisDocument41 pagesBreak-Even Analysis/Cvp AnalysisMehwish ziadNo ratings yet

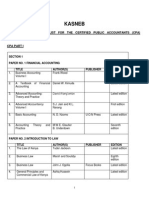

- CPA Reading ListDocument8 pagesCPA Reading ListKongere O KongereNo ratings yet

- Management Advisory Services NotesDocument2 pagesManagement Advisory Services NotesKyla RoxasNo ratings yet

- Form 20FDocument398 pagesForm 20FNguyen KyNo ratings yet