You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Business FinanceDocument109 pagesBusiness FinanceLuz Soriano91% (53)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Far Ifrs Study Manual 2019Document737 pagesFar Ifrs Study Manual 2019Isavic Alsina100% (6)

- FM 10.1 Working Cap - IntroDocument31 pagesFM 10.1 Working Cap - IntroKishlay SinghNo ratings yet

- BE National NotesDocument9 pagesBE National NotesKishlay SinghNo ratings yet

- FM Notes - 2020Document36 pagesFM Notes - 2020Kishlay SinghNo ratings yet

- BC - Chapter2 Business ComDocument27 pagesBC - Chapter2 Business ComKishlay SinghNo ratings yet

- Chapter - 15: Capital Structure Theory and PolicyDocument32 pagesChapter - 15: Capital Structure Theory and PolicyKlaseek100% (1)

- Gujarat Technological University: IdentifyDocument3 pagesGujarat Technological University: IdentifyVrutika Shah (207050592001)No ratings yet

- Business OpportunityDocument11 pagesBusiness OpportunityElias HaileNo ratings yet

- Engagement of Academics in University Technology Transfer - 2020 - European EcoDocument25 pagesEngagement of Academics in University Technology Transfer - 2020 - European Ecolucecita1902No ratings yet

- Anotações - GBPUSD Breakdown 1Document6 pagesAnotações - GBPUSD Breakdown 1José PaivaNo ratings yet

- Foreign Direct Investment, Net Inflows (Bop, Current Us$)Document2 pagesForeign Direct Investment, Net Inflows (Bop, Current Us$)soumyaNo ratings yet

- The Financial Crisis Inquiry ReportDocument662 pagesThe Financial Crisis Inquiry ReportInvestor ProtectionNo ratings yet

- R07 Statistical Concepts and Market ReturnsDocument34 pagesR07 Statistical Concepts and Market ReturnsBảo TrâmNo ratings yet

- ME 291 Engineering Economy: Combining FactorsDocument15 pagesME 291 Engineering Economy: Combining FactorsEhsan Ur RehmanNo ratings yet

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- Capital Expenditure (CapEx) DefinitionDocument9 pagesCapital Expenditure (CapEx) DefinitionSammyNo ratings yet

- Aditya Birla GroupDocument45 pagesAditya Birla GroupCalaghan EnthiadoNo ratings yet

- Investment Banking and Opportunities in ChinaDocument576 pagesInvestment Banking and Opportunities in ChinaAdam GellenNo ratings yet

- ch10 2Document5 pagesch10 2ghsoub777No ratings yet

- AVCJ Singapore Brochure 09Document7 pagesAVCJ Singapore Brochure 09octave bodelNo ratings yet

- Annual-Report 2018 (8.4MB) 1561269324 PDFDocument416 pagesAnnual-Report 2018 (8.4MB) 1561269324 PDFFahimNo ratings yet

- BPP P3 Step 6 AnswersDocument29 pagesBPP P3 Step 6 AnswersRavi Pall100% (1)

- K 2 Khajane 2 ChallanDocument3 pagesK 2 Khajane 2 ChallanVinutha MBNo ratings yet

- Corporate Law 2: Dr. Shakuntala Misra National Rehabilitation UniversityDocument11 pagesCorporate Law 2: Dr. Shakuntala Misra National Rehabilitation UniversityAshish pariharNo ratings yet

- Inter 2nd Year SyllabusDocument2 pagesInter 2nd Year SyllabusSri VasuNo ratings yet

- Rydal's RejectionDocument6 pagesRydal's RejectionVanessa C. RoaNo ratings yet

- MS 44Document9 pagesMS 44AnjnaKandariNo ratings yet

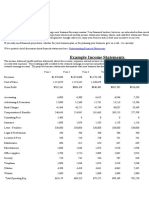

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- 6 Important Stages in The Data Processing CycleDocument15 pages6 Important Stages in The Data Processing CycleRockyLagishetty0% (1)

- When North Gold Project Seeking Investors To Develop in ZimbabweDocument20 pagesWhen North Gold Project Seeking Investors To Develop in ZimbabweMauled ResourcesNo ratings yet

- Market Outlook Oct 2013Document4 pagesMarket Outlook Oct 2013eliforu100% (1)

- Annex E: This Statement Should Be Read in Conjunction With The Accompanying NotesDocument1 pageAnnex E: This Statement Should Be Read in Conjunction With The Accompanying NotesMark Ronnier VedañaNo ratings yet

- Corporate Profile: Metropolitan Bank and Trust CompanyDocument54 pagesCorporate Profile: Metropolitan Bank and Trust CompanyAnn Camille Joaquin100% (1)