You might also like

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- 19 - Ch4 Weekly QuestionsDocument10 pages19 - Ch4 Weekly QuestionsCamilo ToroNo ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Cash Budget AnalysisDocument23 pagesCash Budget Analysisarjun sachdevNo ratings yet

- Financial Planning Tools and Concepts: Lesson 3Document21 pagesFinancial Planning Tools and Concepts: Lesson 3chacha caberNo ratings yet

- Questions On Cash Budget-2Document7 pagesQuestions On Cash Budget-2Mpolokeng HlabanaNo ratings yet

- Finance Report Group 2Document35 pagesFinance Report Group 2AbigailNo ratings yet

- Cash Budget October-DecemberDocument3 pagesCash Budget October-DecemberAJNo ratings yet

- TM - Activity 2 Problem - Ditchon, John MarDocument10 pagesTM - Activity 2 Problem - Ditchon, John MarJohn Mar DitchonNo ratings yet

- Solutions To Chapter 15 Questions - Managing Current AssetsDocument5 pagesSolutions To Chapter 15 Questions - Managing Current AssetsSyeda MiznaNo ratings yet

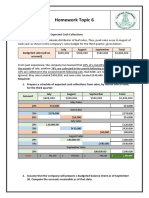

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- SophisticatesDocument3 pagesSophisticatesLuis Melquiades P. GarciaNo ratings yet

- 3 Months PlanDocument8 pages3 Months PlanWaleed ZakariaNo ratings yet

- Exercises Budgeting ACCT2105 3s2010Document7 pagesExercises Budgeting ACCT2105 3s2010Hanh Bui0% (1)

- Financial Plan: Important AssumptionsDocument15 pagesFinancial Plan: Important AssumptionsjehooniesunshineNo ratings yet

- Magma Minerals Case StudyDocument6 pagesMagma Minerals Case StudyJoyce De LunaNo ratings yet

- Reviewer For Midterm XFINMAR A224and A225Document5 pagesReviewer For Midterm XFINMAR A224and A225ralph11240308No ratings yet

- CBA Corporation Cash Budget AnalysisDocument16 pagesCBA Corporation Cash Budget AnalysisLysss EpssssNo ratings yet

- 2009-02-27 005030 SharpeDocument6 pages2009-02-27 005030 SharpeAndrea RobinsonNo ratings yet

- Group Assignment 3 (CB Telaga Hijau BHD)Document5 pagesGroup Assignment 3 (CB Telaga Hijau BHD)Syafiqah AmranNo ratings yet

- Cash Receipts and Disbursements ScheduleDocument10 pagesCash Receipts and Disbursements ScheduleSYED ANEES ALINo ratings yet

- 5-Year Financial Projections for New BusinessDocument6 pages5-Year Financial Projections for New BusinessCedric JohnsonNo ratings yet

- Sam and Sara DebtDocument46 pagesSam and Sara DebtAk Rana10% (10)

- Isfi Nuraida - Anggaran KasDocument86 pagesIsfi Nuraida - Anggaran KasGhinaNo ratings yet

- Planning and Budgeting Case StudyDocument3 pagesPlanning and Budgeting Case StudyRichie Donato100% (1)

- Planning and Budgeting Case StudyDocument3 pagesPlanning and Budgeting Case StudyRichie DonatoNo ratings yet

- Master budget for electronics companyDocument8 pagesMaster budget for electronics companyBlackBunny103No ratings yet

- 108 Efe 94 F 05642 C 6 BcfeDocument11 pages108 Efe 94 F 05642 C 6 BcfeKryzha RemojoNo ratings yet

- Case Study #1: Bigger Isn't Always Better!Document4 pagesCase Study #1: Bigger Isn't Always Better!Marilou GabayaNo ratings yet

- Cash Management QuestionsDocument5 pagesCash Management QuestionsManasi Jamsandekar100% (1)

- Automotive Shop and DesigningDocument8 pagesAutomotive Shop and DesigningMore, Mary RuthNo ratings yet

- FileDocument5 pagesFileRonnel RosalesNo ratings yet

- Sales-BudgetDocument57 pagesSales-BudgetBea NicoleNo ratings yet

- Total Cash Inflow: PaymentsDocument12 pagesTotal Cash Inflow: PaymentsLikith RNo ratings yet

- Case 8-31: April May June QuarterDocument2 pagesCase 8-31: April May June QuarterileviejoieNo ratings yet

- Case Study #2: Growing PainsDocument3 pagesCase Study #2: Growing PainsMissey Grace PuntalNo ratings yet

- Short Term Financial PlanningDocument8 pagesShort Term Financial PlanningHassan MohsinNo ratings yet

- Foundations of Financial Management: Spreadsheet TemplatesDocument9 pagesFoundations of Financial Management: Spreadsheet Templatesalaa_h1100% (1)

- Compare Financial Statements of Two CompaniesDocument9 pagesCompare Financial Statements of Two CompaniesLuvnica VermaNo ratings yet

- Cash Budgeting QuestionsDocument5 pagesCash Budgeting QuestionsAnissa GeddesNo ratings yet

- Business Finance (Quarter 1 - Weeks 3 & 4)Document11 pagesBusiness Finance (Quarter 1 - Weeks 3 & 4)Francine Dominique CollantesNo ratings yet

- RF Ltd Cash BudgetDocument26 pagesRF Ltd Cash BudgetRiaz Baloch Notezai100% (1)

- Financial Management PORTFOLIO MidDocument8 pagesFinancial Management PORTFOLIO MidMyka Marie CruzNo ratings yet

- Financial Management PORTFOLIO MidDocument8 pagesFinancial Management PORTFOLIO MidMyka Marie CruzNo ratings yet

- IA3 Chapter 12 21Document12 pagesIA3 Chapter 12 21ZicoNo ratings yet

- The Sharpe Corporation's ProjectedDocument3 pagesThe Sharpe Corporation's Projectedmadnansajid8765No ratings yet

- Financial PlanningDocument6 pagesFinancial Planningakimasa raizeNo ratings yet

- ACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVDocument6 pagesACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVmy VinayNo ratings yet

- Cash Budgeting and Fraud Management: Topic 4Document16 pagesCash Budgeting and Fraud Management: Topic 4sv03No ratings yet

- Cash Management Chapter SummaryDocument4 pagesCash Management Chapter SummaryMukul KadyanNo ratings yet

- 2018-Spring-Fin - Acct.-Final ALTERNATE Exam-1Document6 pages2018-Spring-Fin - Acct.-Final ALTERNATE Exam-1RealGenius (Carl)No ratings yet

- Form of Ownership Chosen and ReasoningDocument14 pagesForm of Ownership Chosen and ReasoningSheikh MarufNo ratings yet

- Cash ManagementDocument16 pagesCash ManagementdhruvNo ratings yet

- Analysis and Interpretation of Financial Statements: What's NewDocument16 pagesAnalysis and Interpretation of Financial Statements: What's NewJanna Gunio50% (2)

- BSIE_2-2_ACT4Document3 pagesBSIE_2-2_ACT4-st3v3craft-No ratings yet

- Accounting for Special Partnership TransactionsDocument15 pagesAccounting for Special Partnership TransactionsJessaNo ratings yet

- Project Two. Process Financial Transactions and Prepare Financial The Accounts in The Ledger ofDocument11 pagesProject Two. Process Financial Transactions and Prepare Financial The Accounts in The Ledger ofGetahunNo ratings yet

- Solutions Guide: Capital Budgeting Case StudyDocument5 pagesSolutions Guide: Capital Budgeting Case StudySri SardiyantiNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- Ramatex AGM noticeDocument26 pagesRamatex AGM noticeMohd Shareen Ezzry Mohd SomNo ratings yet

- Capital Budgeting at MakeMyTripDocument82 pagesCapital Budgeting at MakeMyTripPratik Jalan100% (1)

- Basel Disclosure Ashad2080Document4 pagesBasel Disclosure Ashad2080Na Bee NaNo ratings yet

- Ratio Analysis Profit and Loss StatementDocument7 pagesRatio Analysis Profit and Loss StatementAsaf RajputNo ratings yet

- Circualr No.217Document17 pagesCircualr No.217Raghavendra M RNo ratings yet

- Capital Structure UploadDocument17 pagesCapital Structure UploadLakshmi Harshitha mNo ratings yet

- Last Assignment of PRC-04 December 2022Document94 pagesLast Assignment of PRC-04 December 2022mudassar saeedNo ratings yet

- Companies Act and Mergers & Acquisitions GuideDocument9 pagesCompanies Act and Mergers & Acquisitions GuideAbhishek KumarNo ratings yet

- MPS 1941669 1202490 16026890L 04 2023Document2 pagesMPS 1941669 1202490 16026890L 04 2023Ajay AhlawatNo ratings yet

- Final Audit CA SJ Short Notes AC CG FullDocument18 pagesFinal Audit CA SJ Short Notes AC CG FullsimranNo ratings yet

- Macd OngcDocument8 pagesMacd Ongcraju RJNo ratings yet

- Questions - Income Tax Divyastra CH 7 - PGBPDocument19 pagesQuestions - Income Tax Divyastra CH 7 - PGBPArjun ThawaniNo ratings yet

- Midland asset beta estimatesDocument4 pagesMidland asset beta estimatessumeet kumarNo ratings yet

- ENTREPRENEURSHIP DEVELOPMENT - QB Part BDocument4 pagesENTREPRENEURSHIP DEVELOPMENT - QB Part Bparandaman.mechNo ratings yet

- Dr.G.R.Damodaran College of Science Financial Management Multiple Choice QuestionsDocument20 pagesDr.G.R.Damodaran College of Science Financial Management Multiple Choice Questionsshuhal AhmedNo ratings yet

- (5032) - OFFICIALLY Assignment 1Document19 pages(5032) - OFFICIALLY Assignment 1Nguyen Khanh Ly (FGW HN)No ratings yet

- Chapter 5-Financial Instruments CA P.S. Beniwal-9990301165Document12 pagesChapter 5-Financial Instruments CA P.S. Beniwal-9990301165antonydonNo ratings yet

- Financial Accounting Canadian 6th Edition Libby Solutions Manual DownloadDocument69 pagesFinancial Accounting Canadian 6th Edition Libby Solutions Manual DownloadDarla Escudero100% (23)

- Impairment of Assets by The ICAIDocument59 pagesImpairment of Assets by The ICAIHeena KhandelwalNo ratings yet

- Question Test Far560 June 2017 Csofp DragonDocument3 pagesQuestion Test Far560 June 2017 Csofp DragonhdyhNo ratings yet

- Chapter 2Document42 pagesChapter 2AynurNo ratings yet

- Ventura, Mary Mickaella R - Chapter9 (No.4,5,7,8,9,10,16)Document4 pagesVentura, Mary Mickaella R - Chapter9 (No.4,5,7,8,9,10,16)Mary VenturaNo ratings yet

- Mayes 8e CH01 Problem SetDocument12 pagesMayes 8e CH01 Problem SetRamez AhmedNo ratings yet

- Full Download Financial Reporting and Analysis 5th Edition Revsine Solutions ManualDocument20 pagesFull Download Financial Reporting and Analysis 5th Edition Revsine Solutions Manualkarolynzwilling100% (44)

- Tata Motors Last 5years Balance SheetDocument2 pagesTata Motors Last 5years Balance SheetSuman Sarkar100% (1)

- Notes Cfa Fixed Income R42Document30 pagesNotes Cfa Fixed Income R42Ayah AkNo ratings yet

- Module Title: International Finance: Module Handbook 2020/21 Module Code: BMG704 (86966)Document19 pagesModule Title: International Finance: Module Handbook 2020/21 Module Code: BMG704 (86966)Osman IqbalNo ratings yet

- Chapter Two International Public Sector Accounting Standard (Ipsas) Ipsas 1 Presentation of Financial StatementsDocument21 pagesChapter Two International Public Sector Accounting Standard (Ipsas) Ipsas 1 Presentation of Financial StatementsSara NegashNo ratings yet

- Term Sheet Negotiations For Trendsetter IncDocument24 pagesTerm Sheet Negotiations For Trendsetter Inc53570076100% (4)

- The Value Line Investment Survey - Selection & Opinion: Product GuideDocument9 pagesThe Value Line Investment Survey - Selection & Opinion: Product GuideJamie GiannaNo ratings yet