You might also like

- FAR 04 - ReceivablesDocument10 pagesFAR 04 - ReceivablesSheira Mae Sulit Napoles100% (1)

- IM - Updates in Financial Reporting Standards (ACCO 40023) - Cash To AccrualDocument13 pagesIM - Updates in Financial Reporting Standards (ACCO 40023) - Cash To AccrualJasmine100% (2)

- Chapter 16 InventoriesDocument21 pagesChapter 16 InventoriesDidik DidiksterNo ratings yet

- 1 InventoriesDocument4 pages1 InventoriesJamie MarizNo ratings yet

- 04 Accounts Receivable Answer KeyDocument9 pages04 Accounts Receivable Answer Keywheein aegiNo ratings yet

- FAR 04 ReceivablesDocument10 pagesFAR 04 ReceivablesRoseNo ratings yet

- Accounts ReceivableDocument11 pagesAccounts ReceivableEun Hae100% (1)

- Preparing WorksheetDocument4 pagesPreparing Worksheet6z5qstn8wsNo ratings yet

- Financial Accounting and Reporting - Trade and Other Receivables (Recognition, Measurement, Estimation and Valuation)Document6 pagesFinancial Accounting and Reporting - Trade and Other Receivables (Recognition, Measurement, Estimation and Valuation)LuisitoNo ratings yet

- Session 6 - Comprehensive Financial Statements - (IS BS)Document9 pagesSession 6 - Comprehensive Financial Statements - (IS BS)Darrel SamueldNo ratings yet

- Cash Flow TemplateDocument19 pagesCash Flow TemplateRyou ShinodaNo ratings yet

- Merchandising Operations Part1Document49 pagesMerchandising Operations Part1keith niduelanNo ratings yet

- CHAPTER 13 Intermediate Acctng 1Document66 pagesCHAPTER 13 Intermediate Acctng 1Tessang OnongenNo ratings yet

- Accounts ReceivableDocument54 pagesAccounts ReceivableFrancine Thea M. LantayaNo ratings yet

- ACT2111 Fall 2019 Ch5 - Lecture 7&8 - StudentDocument73 pagesACT2111 Fall 2019 Ch5 - Lecture 7&8 - StudentKevinNo ratings yet

- 04 ReceivablesDocument12 pages04 ReceivablesNina100% (1)

- Cash and Accrual Basis and Single EntryDocument21 pagesCash and Accrual Basis and Single EntryJohn Mark FernandoNo ratings yet

- Cash Flow ModuleDocument5 pagesCash Flow ModuleEmzNo ratings yet

- AFB Lecture 4 Completed DeckDocument41 pagesAFB Lecture 4 Completed DeckAzure Pear HaNo ratings yet

- Cash Basis, Accrual Basis and Single Entry Method: General ConceptsDocument7 pagesCash Basis, Accrual Basis and Single Entry Method: General ConceptsNhel AlvaroNo ratings yet

- The Final Accounts of Sole Trader (Financial Statements) : Topic 5Document32 pagesThe Final Accounts of Sole Trader (Financial Statements) : Topic 5vickramravi16No ratings yet

- Receivable ManagementDocument49 pagesReceivable Managementrekha123No ratings yet

- Accounts Receivable: Notwithstanding, Are Classified As Current AssetsDocument13 pagesAccounts Receivable: Notwithstanding, Are Classified As Current AssetsAdyangNo ratings yet

- Topic 2 - Assets, Equities and LiabilitiesDocument29 pagesTopic 2 - Assets, Equities and Liabilitiesahmadamsyar083No ratings yet

- Accounting For Merchandising BusinessDocument21 pagesAccounting For Merchandising BusinessJunel PlanosNo ratings yet

- Comprehensive Income ModuleDocument5 pagesComprehensive Income ModuleMich Jerald MendiolaNo ratings yet

- Presentation of Financial Statement Income StatementDocument5 pagesPresentation of Financial Statement Income Statementgerald almencionNo ratings yet

- FUNACC - Accounting Cycle of A Merchandising BusinessDocument12 pagesFUNACC - Accounting Cycle of A Merchandising BusinessSassy GirlNo ratings yet

- Module4 AccountsReceivablePartIDocument6 pagesModule4 AccountsReceivablePartIGab OdonioNo ratings yet

- Chapter 4, 5, 6 AssignmentDocument23 pagesChapter 4, 5, 6 AssignmentSamantha Charlize VizcondeNo ratings yet

- Financial Accounting & AnalysisDocument2 pagesFinancial Accounting & AnalysisTangerine Ila TomarNo ratings yet

- Receivables Handouts PDFDocument8 pagesReceivables Handouts PDFKian BarredoNo ratings yet

- Accounting Unit 3Document12 pagesAccounting Unit 3alok beheraNo ratings yet

- Statement of Cash FlowsDocument33 pagesStatement of Cash FlowsKyriye OngilavNo ratings yet

- Accounting For MerchandisingDocument15 pagesAccounting For MerchandisingAj de CastroNo ratings yet

- Sale of Merchandise or ServicesDocument4 pagesSale of Merchandise or ServicesAngelica PagaduanNo ratings yet

- Fabm2 Law q1 Week 1 To 9Document21 pagesFabm2 Law q1 Week 1 To 9Karen, Togeno CabusNo ratings yet

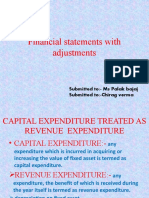

- Financial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaChiragNo ratings yet

- Module 3. Part 1 - Accounts Receivable For StudentsDocument36 pagesModule 3. Part 1 - Accounts Receivable For Studentslord kwantoniumNo ratings yet

- Cash and Accrual BasisDocument4 pagesCash and Accrual BasisSeulgi KangNo ratings yet

- Exercise Set-Intro For Merchandising BusinessDocument10 pagesExercise Set-Intro For Merchandising BusinessCha Eun WooNo ratings yet

- Installment AcctgDocument22 pagesInstallment AcctgMacie MenesesNo ratings yet

- Module - ReceivablesDocument10 pagesModule - ReceivablesJohn Lindy SorianoNo ratings yet

- Merchandising Organized As A Partnership BusinessDocument23 pagesMerchandising Organized As A Partnership BusinessIzza WrapNo ratings yet

- Boss Naik Accounti NG Series: ReceivablesDocument8 pagesBoss Naik Accounti NG Series: ReceivablesKian BarredoNo ratings yet

- Learning Module - Accounts ReceivableDocument2 pagesLearning Module - Accounts ReceivableAngelica SamonteNo ratings yet

- Merchandising Business - Sample Problem (Answers)Document4 pagesMerchandising Business - Sample Problem (Answers)Eana MabalotNo ratings yet

- Local Media-1751823765Document33 pagesLocal Media-1751823765Anonymous CuUAaRSNNo ratings yet

- Accounts Receivable (Chapter 4)Document31 pagesAccounts Receivable (Chapter 4)chingNo ratings yet

- C4 Accounts ReceivableDocument33 pagesC4 Accounts ReceivableShergie GozumNo ratings yet

- Inventories (Financial Accounting)Document2 pagesInventories (Financial Accounting)Herlyn QuintoNo ratings yet

- Financial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaChiragNo ratings yet

- Chapter 7 09302019Document38 pagesChapter 7 09302019Arjay Molina100% (1)

- Merchandising PDFDocument4 pagesMerchandising PDFAlizah BucotNo ratings yet

- Adjusted Trial BalanceDocument4 pagesAdjusted Trial BalanceMonir HossainNo ratings yet

- Week 03 - 01 - Module 06 - Accounting For Receivables (Part 1)Document10 pagesWeek 03 - 01 - Module 06 - Accounting For Receivables (Part 1)지마리No ratings yet

- Accounts Receivables 1Document6 pagesAccounts Receivables 1Ralph Renan NapalaNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Ch2-Introduction To Transaction ProcessingDocument69 pagesCh2-Introduction To Transaction ProcessingMaxene PigtainNo ratings yet

- Case Digest - Harry E. Keeler Electric Co. Vs Rodriguez, 44 Phil 19Document2 pagesCase Digest - Harry E. Keeler Electric Co. Vs Rodriguez, 44 Phil 19Maxene Pigtain100% (1)

- Case Digest - Elcano V Hill 77 SCRADocument1 pageCase Digest - Elcano V Hill 77 SCRAMaxene PigtainNo ratings yet

- Case Digest - Lopez Vito Vs Tambunting, 33 Phil 226Document1 pageCase Digest - Lopez Vito Vs Tambunting, 33 Phil 226Maxene PigtainNo ratings yet

- Case Digest - Parks Vs Prov of Tarlac, 49 Phil 142Document1 pageCase Digest - Parks Vs Prov of Tarlac, 49 Phil 142Maxene PigtainNo ratings yet

- Case Digest - Elcano V Hill 77 SCRADocument1 pageCase Digest - Elcano V Hill 77 SCRAMaxene PigtainNo ratings yet

- S.F. Alatas - On Eurocentrism and Laziness - The Thought of Jose RizalDocument8 pagesS.F. Alatas - On Eurocentrism and Laziness - The Thought of Jose RizalMaxene PigtainNo ratings yet

- A Leadership With Vision: LeadeshipDocument2 pagesA Leadership With Vision: LeadeshipMaxene PigtainNo ratings yet

- Case Digest - Filipino Pipe and Foundry Corp Vs NAWASADocument2 pagesCase Digest - Filipino Pipe and Foundry Corp Vs NAWASAMaxene Pigtain100% (1)

- AQUINO - 2020027331 - B.1.3. Good Citizenship Values PDFDocument1 pageAQUINO - 2020027331 - B.1.3. Good Citizenship Values PDFMaxene PigtainNo ratings yet

- Just Because You Feel Fine, Doesn'T Mean You AreDocument1 pageJust Because You Feel Fine, Doesn'T Mean You AreMaxene PigtainNo ratings yet

- Development Outside The Science: ProtestanismDocument4 pagesDevelopment Outside The Science: ProtestanismMaxene PigtainNo ratings yet

- Solve Using Polya's Four-Step Problem Solving StrategiesDocument2 pagesSolve Using Polya's Four-Step Problem Solving StrategiesMaxene PigtainNo ratings yet