You might also like

- Larry Williams Stock Trading and Investing Course Part 1Document64 pagesLarry Williams Stock Trading and Investing Course Part 1Hanuman Sai Majeti100% (9)

- 10 Golden Rules To Become RichDocument39 pages10 Golden Rules To Become RichAlmas K ShuvoNo ratings yet

- Trading For A Living: - Alexander ElderDocument28 pagesTrading For A Living: - Alexander ElderKABIR RAI100% (4)

- Trading The Trends - Fred McAllenDocument288 pagesTrading The Trends - Fred McAllenkhan4444100% (6)

- MR MarketDocument64 pagesMR MarketRaymondTuskNo ratings yet

- LWStock Trading Investing CourseDocument241 pagesLWStock Trading Investing CourseWorld New67% (3)

- (David Dreman) Contrarian Investment Strategies - OrgDocument34 pages(David Dreman) Contrarian Investment Strategies - Orgarunpdn80% (5)

- Yardeni Stock Market CycleDocument36 pagesYardeni Stock Market CycleOmSilence2651100% (1)

- Earned Value Analysis QuestionsDocument3 pagesEarned Value Analysis QuestionsShubham Kumar100% (1)

- GU 21 Transportation Freight CalculationDocument4 pagesGU 21 Transportation Freight Calculationvicky upreti100% (1)

- Week12-Elgin F. Hunt, David C. Colander - Social Science - An Introduction To The Study of Society-Routledge (2016) (Dragged)Document16 pagesWeek12-Elgin F. Hunt, David C. Colander - Social Science - An Introduction To The Study of Society-Routledge (2016) (Dragged)MuhammetNo ratings yet

- Electrical SOQ EVDocument16 pagesElectrical SOQ EVjaiNo ratings yet

- Lessons From The Successful InvestorFrom EverandLessons From The Successful InvestorRating: 4.5 out of 5 stars4.5/5 (5)

- Market Technician No 73Document12 pagesMarket Technician No 73ZhichaoWang100% (1)

- SAP New GL #9 Customise Cross Company Code Postings For Document SplittingDocument11 pagesSAP New GL #9 Customise Cross Company Code Postings For Document SplittingAlan Cheng100% (2)

- Understanding Market CyclesDocument7 pagesUnderstanding Market CyclesAndyNo ratings yet

- Larry Williams Forecast 2019 ReportDocument71 pagesLarry Williams Forecast 2019 Reportwahib msyah100% (2)

- Senior TLE Tailoring Q1 - M3 and M4 For PrintingDocument27 pagesSenior TLE Tailoring Q1 - M3 and M4 For Printingpocholo funtanillaNo ratings yet

- Repayment Schedule 12-21-23Document1 pageRepayment Schedule 12-21-23Akash MajhiNo ratings yet

- Stock Cycles: Why Stocks Won't Beat Money Markets over the Next Twenty YearsFrom EverandStock Cycles: Why Stocks Won't Beat Money Markets over the Next Twenty YearsRating: 4.5 out of 5 stars4.5/5 (3)

- The 17.6 Year Stock Market Cycle: Connecting the Panics of 1929, 1987, 2000 and 2007From EverandThe 17.6 Year Stock Market Cycle: Connecting the Panics of 1929, 1987, 2000 and 2007Rating: 4 out of 5 stars4/5 (8)

- Construction Company ListDocument21 pagesConstruction Company ListRinkesh Makawana100% (1)

- Victor Niederhoffer On Trend FollowingDocument9 pagesVictor Niederhoffer On Trend FollowingJack JensenNo ratings yet

- PW Anatomy of The BearDocument8 pagesPW Anatomy of The BeargodlionwolfNo ratings yet

- How To Invest in A Down MarketDocument21 pagesHow To Invest in A Down MarketDaniel BucurNo ratings yet

- Options Sellers vs. Buyers: Who Wins?Document4 pagesOptions Sellers vs. Buyers: Who Wins?Prasad KshirsagarNo ratings yet

- DKAM ROE Reporter April 2020Document8 pagesDKAM ROE Reporter April 2020Ganesh GuhadosNo ratings yet

- Black Monday B SectionDocument16 pagesBlack Monday B SectionMaham NadeemNo ratings yet

- Goal 651 1157724468StockIdea1Document4 pagesGoal 651 1157724468StockIdea1Raman BasuNo ratings yet

- 1999 Basic PointsDocument29 pages1999 Basic Pointspep59No ratings yet

- Macroeconomics and Stock Market TimingDocument31 pagesMacroeconomics and Stock Market Timingjl123123No ratings yet

- Stock Market CrashDocument10 pagesStock Market Crashapi-710564150No ratings yet

- 1979 (EDERINGTON) - Hedging Performance of The New Futures MarketsDocument15 pages1979 (EDERINGTON) - Hedging Performance of The New Futures MarketsGeorge máximoNo ratings yet

- July 262010 PostsDocument128 pagesJuly 262010 PostsAlbert L. PeiaNo ratings yet

- August 022010 PostsDocument150 pagesAugust 022010 PostsAlbert L. PeiaNo ratings yet

- Are Markets Efficient - NoDocument3 pagesAre Markets Efficient - Noits4krishna3776No ratings yet

- Boundaries of Technical Analysis - Milton BergDocument14 pagesBoundaries of Technical Analysis - Milton BergAlexis TocquevilleNo ratings yet

- E IBD102008Document36 pagesE IBD102008cphanhuyNo ratings yet

- LINC Week 8Document9 pagesLINC Week 8TomasNo ratings yet

- Guru LessonsDocument12 pagesGuru LessonsSergio Olarte100% (1)

- Is There Something About 40 or 39 PerhapsDocument6 pagesIs There Something About 40 or 39 PerhapsjohnbougearelNo ratings yet

- T MKC G R: HE Loba L EportDocument3 pagesT MKC G R: HE Loba L EportMKC GlobalNo ratings yet

- The Death of Equities (Business Week)Document7 pagesThe Death of Equities (Business Week)highwaysix100% (2)

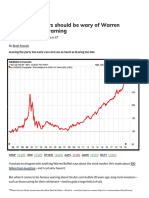

- Opinion:: Investors Should Be Wary of Warren Buffett's Crash WarningDocument5 pagesOpinion:: Investors Should Be Wary of Warren Buffett's Crash WarningNayeem RajaNo ratings yet

- X-Factor091214 - As The Fed Leaves Markets StagnateDocument17 pagesX-Factor091214 - As The Fed Leaves Markets StagnateJamesNo ratings yet

- Investment Theory #4 - Buffett's 1960 Letter - Wiser DailyDocument7 pagesInvestment Theory #4 - Buffett's 1960 Letter - Wiser DailyVladimir OlefirenkoNo ratings yet

- 20 Rules For Markets and Investing - Compound AdvisorsDocument27 pages20 Rules For Markets and Investing - Compound AdvisorsEngin VarolNo ratings yet

- Consistent Compounding 001 Cash Is Still TrashDocument2 pagesConsistent Compounding 001 Cash Is Still Trashblackmoon47No ratings yet

- Stock Market Crashes: Investment Banking & Security AnalysisDocument19 pagesStock Market Crashes: Investment Banking & Security AnalysisDanish SHakeelNo ratings yet

- Initial Public Offerings (Ipos) : Lecturer Department of Finance and AccountingDocument14 pagesInitial Public Offerings (Ipos) : Lecturer Department of Finance and AccountingSimon MutekeNo ratings yet

- The Broyhill Letter: Executive SummaryDocument3 pagesThe Broyhill Letter: Executive SummaryBroyhill Asset ManagementNo ratings yet

- KJHKHJGJHGJHGKL LokjlkjlkDocument5 pagesKJHKHJGJHGJHGKL LokjlkjlkKari WilliamsNo ratings yet

- IceCap Global Market Outlook Dec 2014Document15 pagesIceCap Global Market Outlook Dec 2014CanadianValueNo ratings yet

- 2014.12 IceCap Global Market OutlookDocument15 pages2014.12 IceCap Global Market OutlookZerohedgeNo ratings yet

- Context: How Often Does The Government Shutdown?Document2 pagesContext: How Often Does The Government Shutdown?gradnvNo ratings yet

- Friedberg 3Q ReportDocument16 pagesFriedberg 3Q Reportrichardck61No ratings yet

- Advisory PDFDocument12 pagesAdvisory PDFAnonymous Feglbx5No ratings yet

- Yardeni Stock Market Cycle - 2001 PDFDocument36 pagesYardeni Stock Market Cycle - 2001 PDFscribbugNo ratings yet

- Spot A Market BottomDocument6 pagesSpot A Market BottomArthur SantosNo ratings yet

- Wall Street Crash 1929Document9 pagesWall Street Crash 1929Adrian MazilNo ratings yet

- Most People Don't Believe It, But We Are Right On Schedule For The Next Financial CrashDocument6 pagesMost People Don't Believe It, But We Are Right On Schedule For The Next Financial CrashAnonymous00007No ratings yet

- Black Monday B SectionDocument15 pagesBlack Monday B SectionMaham NadeemNo ratings yet

- Blodget On Market History: JOHN MAULDIN - October 7, 2015Document9 pagesBlodget On Market History: JOHN MAULDIN - October 7, 2015zebulator75000111No ratings yet

- Permanence: 17th June 2013Document5 pagesPermanence: 17th June 2013tony caputi100% (1)

- Benn DoverDocument3 pagesBenn DoverZerohedge100% (2)

- Dohmen Capital Research Proving Wall Street Wrong Special Report 2021Document22 pagesDohmen Capital Research Proving Wall Street Wrong Special Report 2021aKNo ratings yet

- Tax Invoice: Original For RecipientDocument2 pagesTax Invoice: Original For RecipientMisbah Ur RehmanNo ratings yet

- IELTS 6 - 06 - 08 - Đã CH ADocument7 pagesIELTS 6 - 06 - 08 - Đã CH ANguyên Phạm ThuNo ratings yet

- Example de CV Union EuropeenneDocument4 pagesExample de CV Union EuropeenneJean Wesley ThosiacNo ratings yet

- Preeti Kumari 2022Document1 pagePreeti Kumari 2022avisinghoo7No ratings yet

- Term I Practice Examination-2021-22 Class: X Max - Marks: 40 Sub: English Time: 90 Minutes General InstructionsDocument16 pagesTerm I Practice Examination-2021-22 Class: X Max - Marks: 40 Sub: English Time: 90 Minutes General InstructionsMallipudi SphoorthiNo ratings yet

- 5QQMN937 - Week 8Document25 pages5QQMN937 - Week 8example3335273No ratings yet

- WDF 520 PadmDocument52 pagesWDF 520 PadmNahNo ratings yet

- Online Reverse AuctionsDocument17 pagesOnline Reverse AuctionsYashashvi RastogiNo ratings yet

- Trial Questions On Perfect CompetitionDocument2 pagesTrial Questions On Perfect CompetitionWise TetteyNo ratings yet

- Week 2 HousekeepingDocument15 pagesWeek 2 HousekeepingLiza Laith LizzethNo ratings yet

- MGT 504 - MidtermDocument12 pagesMGT 504 - MidtermhamzaNo ratings yet

- Akmen 5 QuizDocument5 pagesAkmen 5 QuizNabilah AdediaNo ratings yet

- Proclamation 1150 2019 Commercial Reg Business Licensing AmendDocument6 pagesProclamation 1150 2019 Commercial Reg Business Licensing AmendMuhedin HussenNo ratings yet

- Why Spiral Column Can Sustain More Load Compared To The Tied ColumnDocument2 pagesWhy Spiral Column Can Sustain More Load Compared To The Tied ColumnARIFUL ISLAMNo ratings yet

- Introduction To Operations Research 10th Edition Hillier Test BankDocument36 pagesIntroduction To Operations Research 10th Edition Hillier Test Bankdorothy100% (14)

- Operation Managemen T Assignment-II: Submitted By: Sakshi Sachdeva ROLL NO. - BM-019143 Sec-C, PGDM 1 YearDocument6 pagesOperation Managemen T Assignment-II: Submitted By: Sakshi Sachdeva ROLL NO. - BM-019143 Sec-C, PGDM 1 YearrohanNo ratings yet

- FTKF BDocument2 pagesFTKF BPads PrietoNo ratings yet

- PMSJ Pricelist - HDMF 1Document1 pagePMSJ Pricelist - HDMF 1Ren Irene MacatangayNo ratings yet

- Abangan V Abangan, 40 Phil 476 (1919)Document1 pageAbangan V Abangan, 40 Phil 476 (1919)Maria LopezNo ratings yet

- Nylbond Product InformationDocument3 pagesNylbond Product Informationrimba kencanaNo ratings yet

- Iqra University Cost Accounting PaperDocument5 pagesIqra University Cost Accounting PaperHaris KhanNo ratings yet