You might also like

- Case Briefing in Legal PracticeDocument42 pagesCase Briefing in Legal PracticeAimi AzemiNo ratings yet

- Company LawDocument18 pagesCompany LawPriya SaxenaNo ratings yet

- Assignment On Effects of Ultra Vires TransactionsDocument5 pagesAssignment On Effects of Ultra Vires Transactionssaksham ahuja100% (1)

- Doctrine of Ultra ViresDocument8 pagesDoctrine of Ultra Viresamanclkhera1585No ratings yet

- Ra 11642Document43 pagesRa 11642pureroseroNo ratings yet

- Real Estate Mortgage AgreementDocument3 pagesReal Estate Mortgage AgreementKen BaxNo ratings yet

- Sample Notice of Motion To Set Aside A Default JudgmentDocument4 pagesSample Notice of Motion To Set Aside A Default JudgmentDebbieNo ratings yet

- Doctrine of Ultra Virus Company Law - AssignmentDocument12 pagesDoctrine of Ultra Virus Company Law - Assignmentkhulesh sahu100% (1)

- Ultra Vires DoctrineDocument10 pagesUltra Vires DoctrineDEAN TENDEKAI CHIKOWO100% (2)

- Doctrine of Ultra Vires Under Company LawDocument15 pagesDoctrine of Ultra Vires Under Company Lawtharani1771_32442248No ratings yet

- Constructive Notice and Indoor MangementDocument14 pagesConstructive Notice and Indoor MangementAnkita ShuklaNo ratings yet

- Q 5 .The Doctrine of Indoor ManagementDocument5 pagesQ 5 .The Doctrine of Indoor ManagementMAHENDRA SHIVAJI DHENAK0% (2)

- Ultra ViresDocument18 pagesUltra VirespariteotiaNo ratings yet

- 7 - Residential Renovation AgreementDocument5 pages7 - Residential Renovation AgreementDondon MalaladNo ratings yet

- 1c III Doctrine of Ultra Vires CorporateDocument11 pages1c III Doctrine of Ultra Vires Corporatechetanyadutt03No ratings yet

- Doctrine of Ultra Vires-Converted (1) 5Document4 pagesDoctrine of Ultra Vires-Converted (1) 5Shri Kant CLCNo ratings yet

- Compnay Law Final11Document10 pagesCompnay Law Final11Movies ArrivalNo ratings yet

- Q .7 Ultra ViresDocument6 pagesQ .7 Ultra ViresMAHENDRA SHIVAJI DHENAK100% (2)

- Doctrine of Ultra ViresDocument8 pagesDoctrine of Ultra ViresAkash Verma100% (1)

- Doctrine of Ultra ViresDocument4 pagesDoctrine of Ultra ViresQasim PalNo ratings yet

- Doctrine of Ultra ViresDocument5 pagesDoctrine of Ultra ViresAsif Iqbal ShuvroNo ratings yet

- Ultra Vires ActDocument15 pagesUltra Vires ActHarneet KaurNo ratings yet

- Doctrine of Ultra Vires - Doc Sid 1Document14 pagesDoctrine of Ultra Vires - Doc Sid 1Angna DewanNo ratings yet

- Doctrine of Ultra ViresDocument13 pagesDoctrine of Ultra ViresAkanshaNo ratings yet

- Doctrine of Ultra Vires-Effects FalDocument11 pagesDoctrine of Ultra Vires-Effects FalFalguni ParekhNo ratings yet

- Company Law - CIA4Document12 pagesCompany Law - CIA4PranavNo ratings yet

- Company Law Assignment (Abhinav)Document8 pagesCompany Law Assignment (Abhinav)Abhinav RautelaNo ratings yet

- Incorporation of Company-MOADocument24 pagesIncorporation of Company-MOAbas 2minNo ratings yet

- Doctrine of Ultra ViresDocument10 pagesDoctrine of Ultra ViresSadhika SharmaNo ratings yet

- The Doctrine of Ultra Vires - Taxguru - in PDFDocument2 pagesThe Doctrine of Ultra Vires - Taxguru - in PDFSat SriNo ratings yet

- Claw Tute AssgnDocument11 pagesClaw Tute AssgnShreyas JainNo ratings yet

- 285 33731DoctrineofUltravirespdfDocument4 pages285 33731DoctrineofUltravirespdfxyzxyz8178181160No ratings yet

- Company Law Memorandum of Association, Contract Powers of The DirectorsDocument3 pagesCompany Law Memorandum of Association, Contract Powers of The Directorstayyaba redaNo ratings yet

- Law. Company ActDocument21 pagesLaw. Company ActSaanvi GoelNo ratings yet

- Doctrine of Ultra Vires - 17flicddn01057Document8 pagesDoctrine of Ultra Vires - 17flicddn01057Karan UpadhyayNo ratings yet

- Legal Aspect - Q 19Document4 pagesLegal Aspect - Q 19Mustafa SanchawalaNo ratings yet

- Doctrine of Ultra ViresDocument4 pagesDoctrine of Ultra ViresdivyaabaskaranNo ratings yet

- Doctrine of Ultra ViresDocument2 pagesDoctrine of Ultra ViresTony Davis0% (1)

- The Companies Act, 2013: Guarantee Company and A Company Having Share Capital. ProvisionDocument10 pagesThe Companies Act, 2013: Guarantee Company and A Company Having Share Capital. ProvisionMansimar SinghNo ratings yet

- Doctrine of Ultra ViresDocument3 pagesDoctrine of Ultra ViresTony Davis100% (1)

- 1 Company Act QA Darshan KhareDocument21 pages1 Company Act QA Darshan KhareGayatri KashyapNo ratings yet

- 1.3 Companies Act, 2013-1Document9 pages1.3 Companies Act, 2013-1sneham7400No ratings yet

- CH 1 - Companies Act NotesDocument26 pagesCH 1 - Companies Act Noteshannageorge245No ratings yet

- Introduction To Company Law 02 - Class NotesDocument72 pagesIntroduction To Company Law 02 - Class Notesaaravrajpoot12345No ratings yet

- Company LawDocument6 pagesCompany LawRiya NitharwalNo ratings yet

- Doctrine UltraviresDocument3 pagesDoctrine UltraviresD Shiva YadavNo ratings yet

- Name: Insha Fatima - Program: PGDM Ebiz (Batch 1) - Roll No.: 028 Legal and Tax Aspects of Business AssignmentDocument3 pagesName: Insha Fatima - Program: PGDM Ebiz (Batch 1) - Roll No.: 028 Legal and Tax Aspects of Business AssignmentInsha FatimaNo ratings yet

- Explain The Doctrine of Ultra VirusDocument6 pagesExplain The Doctrine of Ultra Virusjyothi g sNo ratings yet

- The Doctrine of Ultra ViresDocument2 pagesThe Doctrine of Ultra ViresAniket MishraNo ratings yet

- Company Law ExamDocument15 pagesCompany Law ExamHärîsh KûmärNo ratings yet

- Corporate Law Question BankDocument14 pagesCorporate Law Question BankswapniljainNo ratings yet

- Lecture 3 - Memorandum of AssociationDocument20 pagesLecture 3 - Memorandum of AssociationManjare Hassin RaadNo ratings yet

- Indoor Management and Constructive NoticeDocument11 pagesIndoor Management and Constructive NoticeAvinandan KunduNo ratings yet

- Doctrine of Indoor ManagementDocument4 pagesDoctrine of Indoor ManagementRavi KtNo ratings yet

- Adv. Co. LawDocument10 pagesAdv. Co. LawHazimah YusofNo ratings yet

- Memorandums: Name ClauseDocument5 pagesMemorandums: Name ClausepriyankaNo ratings yet

- Doctrine of Ultravires: by Hasibullah KhairzadaDocument7 pagesDoctrine of Ultravires: by Hasibullah KhairzadaHasibullah KhairzadaNo ratings yet

- Rule of Ultra Vires With Respect To The Power of A CompanyDocument19 pagesRule of Ultra Vires With Respect To The Power of A CompanyAbbas HaiderNo ratings yet

- Doctrine of Indoor Management and Ultra ViresDocument7 pagesDoctrine of Indoor Management and Ultra ViresPadma Gawde100% (1)

- H.P National Law University, Shimla: AssignmentDocument17 pagesH.P National Law University, Shimla: Assignmentkunal mehtoNo ratings yet

- Company LawDocument17 pagesCompany Lawkunal mehtoNo ratings yet

- Memorandum of AssociationDocument6 pagesMemorandum of AssociationPragati PrajapatiNo ratings yet

- Doctrine of Ultra ViresDocument2 pagesDoctrine of Ultra VireslukeaaronNo ratings yet

- THE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]From EverandTHE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]No ratings yet

- Swikriti Meaning and Nature of Professional EthicsDocument4 pagesSwikriti Meaning and Nature of Professional EthicsBidhan PoudyalNo ratings yet

- Durga Judicial MannerismDocument6 pagesDurga Judicial MannerismBidhan PoudyalNo ratings yet

- Aabha Legal ProfessionDocument5 pagesAabha Legal ProfessionBidhan PoudyalNo ratings yet

- Ashmita Principles of Professional EthicsDocument14 pagesAshmita Principles of Professional EthicsBidhan PoudyalNo ratings yet

- Sapana Financial ManagementDocument12 pagesSapana Financial ManagementBidhan PoudyalNo ratings yet

- Right To Social Security and DevelopmentDocument3 pagesRight To Social Security and DevelopmentBidhan PoudyalNo ratings yet

- Independent Corporate Personality of A CompanyDocument12 pagesIndependent Corporate Personality of A CompanyBidhan Poudyal100% (1)

- Development of PovertyDocument9 pagesDevelopment of Povertysuman sumanNo ratings yet

- Unit 3Document10 pagesUnit 3Bidhan PoudyalNo ratings yet

- Paternity, Surrogacy and Protection of ChildDocument23 pagesPaternity, Surrogacy and Protection of ChildBidhan PoudyalNo ratings yet

- Chief District OfficerDocument18 pagesChief District OfficerBidhan PoudyalNo ratings yet

- Writ Procedure PDFDocument38 pagesWrit Procedure PDFBidhan PoudyalNo ratings yet

- Writ Procedure PDFDocument38 pagesWrit Procedure PDFBidhan PoudyalNo ratings yet

- Legal Notice Format For Non-Payment of DividendDocument3 pagesLegal Notice Format For Non-Payment of Dividendchirayu goyalNo ratings yet

- National Law BangladeshDocument2 pagesNational Law BangladeshmunimNo ratings yet

- Nepomuceno Vs Court of AppealsDocument1 pageNepomuceno Vs Court of AppealsParis ValenciaNo ratings yet

- Assignment #1Document3 pagesAssignment #1Chad OngNo ratings yet

- Flow Chart On The Process of Registration of DealingsDocument1 pageFlow Chart On The Process of Registration of Dealings=paul=No ratings yet

- Acct 2005 Practice Exam 1Document16 pagesAcct 2005 Practice Exam 1laujenny64No ratings yet

- Arts of IncorpDocument6 pagesArts of IncorpLezama and Umadhay Law OfficeNo ratings yet

- A Company Is An Artificial Person Created by LawDocument5 pagesA Company Is An Artificial Person Created by LawNeelabhNo ratings yet

- Driot Administratif - Administrative Law of FranceDocument4 pagesDriot Administratif - Administrative Law of FranceTaimour Ali Khan MohmandNo ratings yet

- Ethics of PNPDocument6 pagesEthics of PNPZora IdealeNo ratings yet

- Audit of Public ProcurementDocument13 pagesAudit of Public ProcurementHillary MageroNo ratings yet

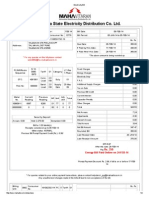

- Electricity BillDocument2 pagesElectricity Billrahuldbajaj2011No ratings yet

- Ac 12886 2020 PDFDocument8 pagesAc 12886 2020 PDFEmma DahunanNo ratings yet

- Pulleys and Tension: Engr. Princess Edynette L. PintoDocument16 pagesPulleys and Tension: Engr. Princess Edynette L. PintoJeromeNo ratings yet

- Kasai Reiko V Annie Lor Lee Fong & Ors (Public Bank BHD, Intervener)Document27 pagesKasai Reiko V Annie Lor Lee Fong & Ors (Public Bank BHD, Intervener)norleena jNo ratings yet

- TELESTAR International RMConflict ManagememntDocument2 pagesTELESTAR International RMConflict ManagememntNaveed RabbaniNo ratings yet

- Construction and InterpretationDocument8 pagesConstruction and InterpretationPPPPNo ratings yet

- Co Kim Cham vs. Tan Keh and DizonDocument2 pagesCo Kim Cham vs. Tan Keh and DizonMARIANNE DILANGALENNo ratings yet

- Vocabulary For English: Term Difinition Translati OnDocument7 pagesVocabulary For English: Term Difinition Translati OnBuzdugan NicoletaNo ratings yet

- Module 3: The Professionals and Practitioners in The Discipline of CommunicationDocument8 pagesModule 3: The Professionals and Practitioners in The Discipline of CommunicationColeen gaboy100% (2)

- ACKO Car Insurance-Jul'21Document5 pagesACKO Car Insurance-Jul'21Roman PatelNo ratings yet

- Montemayor Vs Araneta University FoundationDocument2 pagesMontemayor Vs Araneta University FoundationMac Burdeos CamposueloNo ratings yet

- Tort ProjectDocument30 pagesTort ProjectVishesh Mehrotra100% (1)

- Summer Camp & Club Registration Form: Camper InformationDocument8 pagesSummer Camp & Club Registration Form: Camper Informationzohreen shakeelNo ratings yet

- A.F Sanchez Brokerage, Inc. vs. CA, G.R. No. 147079, December 21, 2004Document15 pagesA.F Sanchez Brokerage, Inc. vs. CA, G.R. No. 147079, December 21, 2004JasenNo ratings yet

![THE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]](https://imgv2-1-f.scribdassets.com/img/word_document/702714789/149x198/ac277f344e/1706724197?v=1)