You might also like

- Share-Based Payments With Answer PDFDocument9 pagesShare-Based Payments With Answer PDFAyaka FujiharaNo ratings yet

- 162 001Document1 page162 001Christian Mark AbarquezNo ratings yet

- Aava Case AnalysisDocument4 pagesAava Case Analysispmahale25No ratings yet

- AUDITING PROBLEMS TEST BANK 2 With AnswersDocument14 pagesAUDITING PROBLEMS TEST BANK 2 With AnswersKimberly Milante100% (3)

- Practice Problems 1Document1 pagePractice Problems 1Ma Angelica Balatucan0% (1)

- FarDocument14 pagesFarKenneth Robledo100% (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- MSc Sales & Marketing Statement of PurposeDocument1 pageMSc Sales & Marketing Statement of PurposeDaud LawrenceNo ratings yet

- Cotx302 Exam 1 Sem 2 2017Document7 pagesCotx302 Exam 1 Sem 2 2017Valeria PetrovNo ratings yet

- Financial Accounting ExamDocument19 pagesFinancial Accounting ExamMwenda MongweNo ratings yet

- Print q3 Nca Held For Salediscontinued Operation Accounting ChangeDocument4 pagesPrint q3 Nca Held For Salediscontinued Operation Accounting ChangeJenelle Acedillo ReyesNo ratings yet

- Problem 1-1 Effect of Counterbalancing and Non-Counterbalancing ErrorsDocument3 pagesProblem 1-1 Effect of Counterbalancing and Non-Counterbalancing ErrorsandreamrieNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument13 pagesCambridge International Advanced Subsidiary and Advanced LevelAR RafiNo ratings yet

- Auditing ProblemsDocument11 pagesAuditing ProblemslisaNo ratings yet

- Problems - Adjusting EntriesDocument3 pagesProblems - Adjusting EntriesaNo ratings yet

- IAS 8 TestDocument3 pagesIAS 8 TestPervaiz AkhterNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelZaid NaveedNo ratings yet

- LO5 QuestionDocument2 pagesLO5 QuestionFrederick LekalakalaNo ratings yet

- Aud Quiz 2Document6 pagesAud Quiz 2MC allivNo ratings yet

- FRK201 Nov2016Document12 pagesFRK201 Nov2016Alex ViljoenNo ratings yet

- Installment Quiz For LMSDocument1 pageInstallment Quiz For LMSSarah Del teodoroNo ratings yet

- NCR Cup 1 Final RoundDocument6 pagesNCR Cup 1 Final RoundMich ClementeNo ratings yet

- Fin Man 1BDocument12 pagesFin Man 1BMelissa KleinNo ratings yet

- C3 - Matching and Adjusting ProcessDocument12 pagesC3 - Matching and Adjusting ProcessIvy Jean Ybera-PapasinNo ratings yet

- AdvaccDocument3 pagesAdvaccAlyssa CamposNo ratings yet

- INTERMEDIATE ACCOUNTING - MIDTERM - 2019-2020 - 2nd Semester - PART5Document3 pagesINTERMEDIATE ACCOUNTING - MIDTERM - 2019-2020 - 2nd Semester - PART5Renalyn ParasNo ratings yet

- Accounts g1 MTPDocument191 pagesAccounts g1 MTPJattu TatiNo ratings yet

- 1st Quiz Afar2 Q PDFDocument2 pages1st Quiz Afar2 Q PDFAnonymous 7HGskNNo ratings yet

- 2021 FAC1A TUT Question Unit 3 Acc Equation, GJ, GL and Trial BalanceDocument2 pages2021 FAC1A TUT Question Unit 3 Acc Equation, GJ, GL and Trial BalanceDaniel OwensNo ratings yet

- AP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYDocument12 pagesAP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYjasfNo ratings yet

- QuizDocument2 pagesQuizAlyssa CamposNo ratings yet

- Discontinued Operations and Noncurrent Assets Held for SaleDocument1 pageDiscontinued Operations and Noncurrent Assets Held for SaleJedaiah CruzNo ratings yet

- Discontinued Operations and Noncurrent Assets Held for SaleDocument1 pageDiscontinued Operations and Noncurrent Assets Held for SaleRhea LalasNo ratings yet

- AFAR - Revenue Recognition, JointDocument3 pagesAFAR - Revenue Recognition, JointJoanna Rose DeciarNo ratings yet

- Intermediate Accounting Midterm Exam Problems and SolutionsDocument2 pagesIntermediate Accounting Midterm Exam Problems and SolutionsRenalyn ParasNo ratings yet

- Homework On Current Liabilities PDFDocument3 pagesHomework On Current Liabilities PDFJenneth RegalaNo ratings yet

- Acc ActivityDocument6 pagesAcc ActivityJoyce Eguia100% (1)

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelMalik AliNo ratings yet

- Pamantasan NG Lungsod NG Valenzuela: College of AccountancyDocument2 pagesPamantasan NG Lungsod NG Valenzuela: College of AccountancyPatricia Camille AustriaNo ratings yet

- Financial Accounting 3BDocument10 pagesFinancial Accounting 3BPRECIOUSNo ratings yet

- Class Example Companies 2023Document2 pagesClass Example Companies 2023NjabuloNo ratings yet

- FA Dec 2018Document8 pagesFA Dec 2018Shawn LiewNo ratings yet

- AUDI315-AUDIT-OF-LIABILITIES-EXERCISESDocument14 pagesAUDI315-AUDIT-OF-LIABILITIES-EXERCISESMeila GomezNo ratings yet

- Auditing Problems Test Bank 2 Auditing Problems Test Bank 2Document16 pagesAuditing Problems Test Bank 2 Auditing Problems Test Bank 2xjammerNo ratings yet

- Correction of ErrorDocument1 pageCorrection of ErrorElmer JuanNo ratings yet

- Mack-Cali Realty Corporation Reports Fourth Quarter and Full Year 2017 ResultsDocument10 pagesMack-Cali Realty Corporation Reports Fourth Quarter and Full Year 2017 ResultsAnonymous Feglbx5No ratings yet

- ACC100 SUPP.pdf (1)Document11 pagesACC100 SUPP.pdf (1)Lebohang NgubaneNo ratings yet

- ASS2 Q2 2018 IIB Final PDFDocument3 pagesASS2 Q2 2018 IIB Final PDFLaurenNo ratings yet

- Final Examination in Auditing Principles and Application 1Document8 pagesFinal Examination in Auditing Principles and Application 1Anie Martinez0% (1)

- Events After The Reporting Period NCA Held For Disposal Discontinued OperationsDocument2 pagesEvents After The Reporting Period NCA Held For Disposal Discontinued OperationsJeremiah DavidNo ratings yet

- FRK201 Nov2019Document11 pagesFRK201 Nov2019Alex ViljoenNo ratings yet

- Error Correction Problem 1: Lord Gen A. Rilloraza, CPADocument5 pagesError Correction Problem 1: Lord Gen A. Rilloraza, CPAMae-shane SagayoNo ratings yet

- 2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFDocument25 pages2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFMae-shane SagayoNo ratings yet

- 06 Correction of Errors PDFDocument5 pages06 Correction of Errors PDFRoxanneNo ratings yet

- ACTREV 4 Business CombinationDocument4 pagesACTREV 4 Business CombinationchosNo ratings yet

- Case 1: Use The Following Information For The Next Six ItemsDocument2 pagesCase 1: Use The Following Information For The Next Six ItemsPrankyJellyNo ratings yet

- Additionial TanongDocument28 pagesAdditionial Tanongboerd77No ratings yet

- Fa May June - 2019Document5 pagesFa May June - 2019xodic49847No ratings yet

- Lease QuestionsDocument12 pagesLease Questionszakhonalubanzi95No ratings yet

- Introduction To Accounting Mock Exam: Certificate in Accounting and Finance Stage ExaminationDocument9 pagesIntroduction To Accounting Mock Exam: Certificate in Accounting and Finance Stage ExaminationUsman WaheedNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Public Financial Management Systems—Bangladesh: Key Elements from a Financial Management PerspectiveFrom EverandPublic Financial Management Systems—Bangladesh: Key Elements from a Financial Management PerspectiveNo ratings yet

- GST101Document1 pageGST101ANKIT KUMAR IPM 2018 BatchNo ratings yet

- Optional: Service BulletinDocument8 pagesOptional: Service BulletinDaniil SerovNo ratings yet

- Assignment 1 Complete The Assignment and Submit It On Moodle. Marks Weightage - 20%Document12 pagesAssignment 1 Complete The Assignment and Submit It On Moodle. Marks Weightage - 20%Shivam SharmaNo ratings yet

- Implementing RBI and RCM to Improve Asset ReliabilityDocument56 pagesImplementing RBI and RCM to Improve Asset ReliabilityKareem RasmyNo ratings yet

- CRT 3rd Year NewDocument232 pagesCRT 3rd Year NewAkshat agrawalNo ratings yet

- Anush IpDocument24 pagesAnush IpAnsh SharmaNo ratings yet

- Chapter 2. Historical and Current ThinkingDocument5 pagesChapter 2. Historical and Current Thinkingnguyetanhtata0207k495No ratings yet

- Technical Letter StructureDocument33 pagesTechnical Letter Structuresayed Tamir janNo ratings yet

- IBS Selection Process GuideDocument24 pagesIBS Selection Process GuideApna time aayegaNo ratings yet

- Asset-V1 MITx+14.100x+2T2020+Type@Asset+Block@Lecture 9 HandoutDocument10 pagesAsset-V1 MITx+14.100x+2T2020+Type@Asset+Block@Lecture 9 HandoutcamirandamNo ratings yet

- Ecc022177 - Cristhian BasanteDocument3 pagesEcc022177 - Cristhian Basanteexportaciones.miguichoNo ratings yet

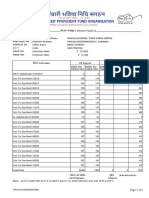

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Sustainbook PDFDocument225 pagesSustainbook PDFjNo ratings yet

- Experienced Hospitality Professional Seeking New OpportunitiesDocument2 pagesExperienced Hospitality Professional Seeking New OpportunitiesValeria SpasovaNo ratings yet

- FSA Guide 20Document16 pagesFSA Guide 20David DangNo ratings yet

- Jawad Internship ReportDocument28 pagesJawad Internship Reportjunaidyaseen442No ratings yet

- Sas#20 Bam242Document9 pagesSas#20 Bam242Everly Mae ElondoNo ratings yet

- Solved A Religious Organization Is Considering Spreading Its Message Into Illinois PDFDocument1 pageSolved A Religious Organization Is Considering Spreading Its Message Into Illinois PDFAnbu jaromiaNo ratings yet

- PEST AnalysisDocument7 pagesPEST AnalysisWaqas Ul HaqueNo ratings yet

- Sales Receipt: Company Name 123 Main Street Hamilton, OH 44416 (321) 456-7890 Email AddressDocument1 pageSales Receipt: Company Name 123 Main Street Hamilton, OH 44416 (321) 456-7890 Email AddressParas ShardaNo ratings yet

- Aditya AS 22 23 2134Document1 pageAditya AS 22 23 2134Aditya AmbwaniNo ratings yet

- reading_sample_sap_press_reporting_with_sap_s4hanaDocument32 pagesreading_sample_sap_press_reporting_with_sap_s4hanaCharles SantosNo ratings yet

- GUCCI - Case Only110910Document39 pagesGUCCI - Case Only110910sabastien_10dec5663No ratings yet

- Grameen BankDocument28 pagesGrameen Bankalpha34567No ratings yet

- Finance and Accounting - PPTX For FinalDocument18 pagesFinance and Accounting - PPTX For Finalmuqaddas bibiNo ratings yet

- Designing The Perfect Procurement Operating Model: OperationsDocument9 pagesDesigning The Perfect Procurement Operating Model: Operationspulsar77No ratings yet

- Explore and Explain:: Grade 12 - EntrepreneurshipDocument12 pagesExplore and Explain:: Grade 12 - EntrepreneurshipLatifah EmamNo ratings yet

- Training in Human Resource ManagementDocument21 pagesTraining in Human Resource ManagementAlok kumarNo ratings yet