You might also like

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeFrom EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeRating: 5 out of 5 stars5/5 (1)

- Corporate Governance and Internal AuditDocument10 pagesCorporate Governance and Internal AuditItdarareNo ratings yet

- CHAPTER 1 Overview of Internal Auditing FazDocument22 pagesCHAPTER 1 Overview of Internal Auditing FazHanis ZahiraNo ratings yet

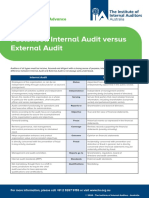

- Internal Audit V External AuditDocument1 pageInternal Audit V External AuditlkhdasouNo ratings yet

- Internal Audit Versus External AuditDocument1 pageInternal Audit Versus External AuditMahmoud ElbagouryNo ratings yet

- Risk Management and Internal AuditorDocument58 pagesRisk Management and Internal AuditorAnanda rizky syifa nabilahNo ratings yet

- Internal Control, Internal Auditor & Risk ManagementDocument58 pagesInternal Control, Internal Auditor & Risk ManagementWagimin SendjajaNo ratings yet

- 18AKJ - Sri Widya Ningsih-Audit InternalDocument5 pages18AKJ - Sri Widya Ningsih-Audit InternalTantiNo ratings yet

- Chapter 1: Internal Auditing Definition and Overview: Jovit G. Cain, CPADocument41 pagesChapter 1: Internal Auditing Definition and Overview: Jovit G. Cain, CPAJao FloresNo ratings yet

- Topic 6 (Part A)Document34 pagesTopic 6 (Part A)Amanda GuanNo ratings yet

- H001 - Intro To Internal AuditingDocument12 pagesH001 - Intro To Internal AuditingKevin James Sedurifa OledanNo ratings yet

- IA ReviewerDocument11 pagesIA ReviewerMaria Patrice MendozaNo ratings yet

- Internal and External AuditorsDocument19 pagesInternal and External AuditorsSHAMRAIZKHANNo ratings yet

- Internal Auditings Role in Corporate Governance (IIA)Document4 pagesInternal Auditings Role in Corporate Governance (IIA)Vidya IntaniNo ratings yet

- Topic 2Document10 pagesTopic 2MussaNo ratings yet

- Auditing 1: Internal AuditDocument45 pagesAuditing 1: Internal AuditChrizt ChrisNo ratings yet

- Internal Auditings Role in Corporate GovernanceDocument4 pagesInternal Auditings Role in Corporate GovernanceJawadNo ratings yet

- Fundamentals of Internal Auditing PDFDocument113 pagesFundamentals of Internal Auditing PDFCarla Jean Cuyos100% (1)

- Lesson 4 Internal Control and Risk ManagementDocument50 pagesLesson 4 Internal Control and Risk ManagementAngelica PagaduanNo ratings yet

- Internal Audit RoleDocument12 pagesInternal Audit RoleBobbyD.ResjaNo ratings yet

- Is The Freedom From Conditions That Threaten The Ability ofDocument14 pagesIs The Freedom From Conditions That Threaten The Ability ofangelica joyce caballesNo ratings yet

- Audit ProjectDocument14 pagesAudit ProjectDhara MehtaNo ratings yet

- Chapter 3 - GovernanceDocument18 pagesChapter 3 - GovernanceDeasy NoviyantiNo ratings yet

- Chapter 6-8Document10 pagesChapter 6-8DeyNo ratings yet

- Internal Auditing:: Assurance, Insight, and ObjectivityDocument12 pagesInternal Auditing:: Assurance, Insight, and ObjectivityJean CabigaoNo ratings yet

- 15 JournalDocument4 pages15 JournalJane DizonNo ratings yet

- Understanding The Entity'S InternalcontrolDocument44 pagesUnderstanding The Entity'S Internalcontrolgandara koNo ratings yet

- What Is Internal AuditDocument6 pagesWhat Is Internal AuditRaven GarciaNo ratings yet

- DASAR - Slide Fondasi Audit Internal - Hananto Widhiatmoko (PUBLISH)Document58 pagesDASAR - Slide Fondasi Audit Internal - Hananto Widhiatmoko (PUBLISH)Pingkan OmpiNo ratings yet

- Solution Manual For Internal Auditing Assurance and Consulting Services 2nd Edition by RedingDocument9 pagesSolution Manual For Internal Auditing Assurance and Consulting Services 2nd Edition by RedingBrianWelchxqdm100% (38)

- Slides - Chapter 9Document7 pagesSlides - Chapter 9Thu TrangNo ratings yet

- Internal and External Audit ComparisonDocument15 pagesInternal and External Audit ComparisonRegz TabachoyNo ratings yet

- Chapter 1 - Introduction To IA STDTDocument21 pagesChapter 1 - Introduction To IA STDTNor Syahra AjinimNo ratings yet

- Internal Control: Consideration ofDocument35 pagesInternal Control: Consideration ofMa. KristineNo ratings yet

- Internal Audit Cost Control PDFDocument16 pagesInternal Audit Cost Control PDFNMA NMANo ratings yet

- All in A Day'S Work: A Look at The Varied Responsibilities of Internal AuditorsDocument12 pagesAll in A Day'S Work: A Look at The Varied Responsibilities of Internal AuditorsRhoda Marie R. CuaresmaNo ratings yet

- Kirk Report Adtng 422Document21 pagesKirk Report Adtng 422Pritz Marc Bautista MorataNo ratings yet

- Udemy Course CIA Part 2 Focus MaterialsDocument77 pagesUdemy Course CIA Part 2 Focus MaterialsLayar KayarNo ratings yet

- Internal Auditing.2022Document19 pagesInternal Auditing.2022One AshleyNo ratings yet

- The Difference Between Internal and External AuditDocument3 pagesThe Difference Between Internal and External AuditRohit BajpaiNo ratings yet

- Internal Audit CharterDocument6 pagesInternal Audit CharterManshu PoorviNo ratings yet

- Internal Auditing Module 1Document21 pagesInternal Auditing Module 1kapaymichelleNo ratings yet

- L6 Internal ControlDocument15 pagesL6 Internal ControlMia FayeNo ratings yet

- Chapter 4 - Internal ControlDocument60 pagesChapter 4 - Internal Controlyebegashet100% (1)

- CG - 4Document4 pagesCG - 4Pillows GonzalesNo ratings yet

- Session 4 - Risk Governance & Control Environment v2 - Chris RazookDocument26 pagesSession 4 - Risk Governance & Control Environment v2 - Chris RazookEra HRNo ratings yet

- Managing The Internal Audit Function - CompDocument38 pagesManaging The Internal Audit Function - CompBea BajarNo ratings yet

- Module 4 - Nature of WorkDocument43 pagesModule 4 - Nature of WorkMichaelNo ratings yet

- 13 Introduction To Internal AuditingDocument6 pages13 Introduction To Internal AuditingShailene DavidNo ratings yet

- Corporate Governance TM6Document26 pagesCorporate Governance TM611210000015No ratings yet

- All in A Days Work BrochureDocument12 pagesAll in A Days Work BrochureRAÚL BARRADO MENDONo ratings yet

- Internal and External Audit ComparisonDocument15 pagesInternal and External Audit ComparisonRegz TabachoyNo ratings yet

- T@T November 2010 PDFDocument4 pagesT@T November 2010 PDFMauricio De La TorreNo ratings yet

- Chariza L. Colita Aud RPRDocument20 pagesChariza L. Colita Aud RPRPritz Marc Bautista MorataNo ratings yet

- OperationalDocument13 pagesOperationalAlona ColiaenNo ratings yet

- Govbusman Module 2 - Chapter 2Document7 pagesGovbusman Module 2 - Chapter 2Rohanne Garcia AbrigoNo ratings yet

- 2 Internal AuditDocument8 pages2 Internal AuditNurita A TyasNo ratings yet

- Internal Control System: Quarter 1 - Week 1Document17 pagesInternal Control System: Quarter 1 - Week 1KiermoralesNo ratings yet

- Consideration of Internal ControlDocument10 pagesConsideration of Internal ControlMAG MAGNo ratings yet

- IFRS 16: Lessor & Lessee Accounting Treatment in The Finance LeaseDocument2 pagesIFRS 16: Lessor & Lessee Accounting Treatment in The Finance LeaseboygarfanNo ratings yet

- GCC Ia Ia Rev.00.24Document3 pagesGCC Ia Ia Rev.00.24boygarfanNo ratings yet

- Data Integrity TemplateDocument4 pagesData Integrity TemplateboygarfanNo ratings yet

- 1122 482 2019-02-14 15-47-38 enDocument17 pages1122 482 2019-02-14 15-47-38 enboygarfanNo ratings yet

- Mss-Netherlands enDocument16 pagesMss-Netherlands enboygarfanNo ratings yet

- Retail Collection PolicyDocument39 pagesRetail Collection PolicyK Praveen RajNo ratings yet

- 1122 482 2019-02-14 15-47-38 enDocument16 pages1122 482 2019-02-14 15-47-38 enboygarfanNo ratings yet

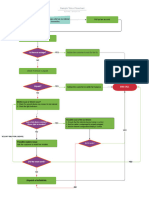

- Telco Flowchart 2Document1 pageTelco Flowchart 2p01zawjNo ratings yet

- SAP Programming LanguageDocument76 pagesSAP Programming Languagejabbar1959No ratings yet

- 2750 514-23 en Rev BDocument4 pages2750 514-23 en Rev BGuitART TVNo ratings yet

- Prevent Leaks in Heat ExchangersDocument7 pagesPrevent Leaks in Heat ExchangersNirmal SubudhiNo ratings yet

- Samsung LE-40A866 - 20081009152533312 - BN68-01701B-00Eng-0910Document72 pagesSamsung LE-40A866 - 20081009152533312 - BN68-01701B-00Eng-0910a11615870No ratings yet

- (BS EN 932-5 - 2000) - Tests For General Properties of Aggregates. Common Equipment and CalibrationDocument18 pages(BS EN 932-5 - 2000) - Tests For General Properties of Aggregates. Common Equipment and CalibrationAdelNo ratings yet

- 2019 11 20 23 41 26Document227 pages2019 11 20 23 41 26Aqua Galon0% (1)

- Itu-T G.841Document98 pagesItu-T G.841Deolindo ZanuttiniNo ratings yet

- Pestle For ToyotaDocument2 pagesPestle For ToyotaAshvin Bageeruthee100% (3)

- As Cable Etp-394 Ysly-Jz - OzDocument2 pagesAs Cable Etp-394 Ysly-Jz - OzAlicia AltamiranoNo ratings yet

- Expulsion Fuse Links For Use in High Voltage (Liston Fusible)Document36 pagesExpulsion Fuse Links For Use in High Voltage (Liston Fusible)Leon OrtegaNo ratings yet

- Calibration CertificatesDocument21 pagesCalibration Certificatesbhadresh2003cvlNo ratings yet

- ENG - Installation Manual For Sequential LPG-CNG (May 2005)Document77 pagesENG - Installation Manual For Sequential LPG-CNG (May 2005)Kar Gayee100% (1)

- SLP TX420Document2 pagesSLP TX420Estrellita BelénNo ratings yet

- Filtre TV EpcosDocument13 pagesFiltre TV Epcosparvalhao_No ratings yet

- Work Permit Systems - tcm17-13910Document16 pagesWork Permit Systems - tcm17-13910CJNo ratings yet

- Market Research Report Preparation and Presentation UpdateDocument28 pagesMarket Research Report Preparation and Presentation Updatecome2pratik33% (3)

- PIP INIH1000 SampleDocument6 pagesPIP INIH1000 SampleIvan Roco100% (1)

- Catálogo FlowserveDocument23 pagesCatálogo Flowserveanderson8657No ratings yet

- CSharp For Sharp Kids - Part 1 Getting StartedDocument10 pagesCSharp For Sharp Kids - Part 1 Getting StartedBrothyam Huaman CasafrancaNo ratings yet

- AS4324.1-1995 Standard For Design of Bulk Materials Handling MachinesDocument8 pagesAS4324.1-1995 Standard For Design of Bulk Materials Handling Machinesridzim4638100% (1)

- SQM Chapter6Document15 pagesSQM Chapter6azmastecNo ratings yet

- ELM323 OBD (ISO) To RS232 Interpreter: Description FeaturesDocument11 pagesELM323 OBD (ISO) To RS232 Interpreter: Description FeaturesAdauto Augusto Nunes FilhoNo ratings yet

- Basic Safety Plan: Aker Powergas PVT LTD Page NoDocument36 pagesBasic Safety Plan: Aker Powergas PVT LTD Page NoAbid AliNo ratings yet

- Common File Extensions PDFDocument8 pagesCommon File Extensions PDFRahul kumarNo ratings yet

- 8155 Is An Integrated RamDocument22 pages8155 Is An Integrated RamVipan SharmaNo ratings yet

- TR - Gas Appliances and Their Accessories - Version 1 - Amendment 2Document20 pagesTR - Gas Appliances and Their Accessories - Version 1 - Amendment 2陳端民No ratings yet

- TCP and UDP Ports Used by Apple Software ProductsDocument6 pagesTCP and UDP Ports Used by Apple Software ProductsEduardo CharllesNo ratings yet

- Optimized Clustering Algorithm For WBAN To WBAN CommunicationDocument13 pagesOptimized Clustering Algorithm For WBAN To WBAN CommunicationnadeemajeedchNo ratings yet

- Atm ProjectDocument18 pagesAtm Projectsujit_ranjanNo ratings yet