You might also like

- Hammersmith and Fulham in Sterling Interest Swap Loss of About 600 Million in 1988Document9 pagesHammersmith and Fulham in Sterling Interest Swap Loss of About 600 Million in 1988Noor Afzan AbdullahNo ratings yet

- Document PDFDocument7 pagesDocument PDFPeña MotorNo ratings yet

- Asia Monthly Outlook Mar-2023Document21 pagesAsia Monthly Outlook Mar-2023Muhammad LuthfiNo ratings yet

- Maintaining A Solid Position: Corporate PresentationDocument37 pagesMaintaining A Solid Position: Corporate Presentationtim horeNo ratings yet

- Financial Services in 2018: A Special Report From The Economist Intelligence UnitDocument12 pagesFinancial Services in 2018: A Special Report From The Economist Intelligence UnitLa_MerguezNo ratings yet

- Crisil 2023 BFSI ReportDocument58 pagesCrisil 2023 BFSI ReportChirag shahNo ratings yet

- Highlights of Federal Budget 2080 81Document30 pagesHighlights of Federal Budget 2080 81Rajulla ShresthaNo ratings yet

- Asian Consumers: Short-Term Risks May Be A Niggle This YearDocument12 pagesAsian Consumers: Short-Term Risks May Be A Niggle This YearDương Huy Chương ĐặngNo ratings yet

- Qsmef Dec 2015Document23 pagesQsmef Dec 2015WaqarNo ratings yet

- IndiaEconomicsOverheating090207 MF PDFDocument4 pagesIndiaEconomicsOverheating090207 MF PDFdidwaniasNo ratings yet

- CS PFG Asia Market Overview Presentation - February 2021Document24 pagesCS PFG Asia Market Overview Presentation - February 2021Rishika RankaNo ratings yet

- 2021 Hotel Sector Briefing PresentationDocument135 pages2021 Hotel Sector Briefing Presentationmaria sophiaNo ratings yet

- Investor Presentation Nov2018Document30 pagesInvestor Presentation Nov2018kumar adityaNo ratings yet

- Power Pack BankingDocument26 pagesPower Pack BankingDev DugarNo ratings yet

- ICSC Mall REIT Presentation 12-7-2009Document68 pagesICSC Mall REIT Presentation 12-7-2009Terry Tate Buffett100% (1)

- 2020 Budget PreviewDocument11 pages2020 Budget PreviewClaudium ClaudiusNo ratings yet

- FY21 Gaming Industry Briefing FinalDocument163 pagesFY21 Gaming Industry Briefing Finalmaria sophiaNo ratings yet

- Vietnam: Moving Toward The 3 Decade of Transition and DevelopmentDocument37 pagesVietnam: Moving Toward The 3 Decade of Transition and DevelopmentDieu xinhNo ratings yet

- MPS FY2021-22:: CPD's Reaction OnDocument49 pagesMPS FY2021-22:: CPD's Reaction OnAdnan AsifNo ratings yet

- China Policy Financial Bonds PrimerDocument39 pagesChina Policy Financial Bonds PrimerbondbondNo ratings yet

- Five Key QuestionsDocument12 pagesFive Key QuestionsInternational Business TimesNo ratings yet

- Norsk Hydro Presentation Q2 2022Document126 pagesNorsk Hydro Presentation Q2 2022M StarNo ratings yet

- 2b PEPP2015 Reliance Nayak Jun15Document33 pages2b PEPP2015 Reliance Nayak Jun15Kseniya SergeevaNo ratings yet

- Brixton Et Al - AQR Q1 2022 Capital Market AssumptionsDocument17 pagesBrixton Et Al - AQR Q1 2022 Capital Market AssumptionsStephen LinNo ratings yet

- New Approaches To SME Finance Using Bank Account Information (Big Data)Document19 pagesNew Approaches To SME Finance Using Bank Account Information (Big Data)ADBI EventsNo ratings yet

- Budget HighlightsDocument15 pagesBudget HighlightsLasya KankatalaNo ratings yet

- MD Abdullah Al Mamun - ID-17102049 - Major Accounting.Document44 pagesMD Abdullah Al Mamun - ID-17102049 - Major Accounting.Abdullah Al MamunNo ratings yet

- SBP Consolidated-ReportDocument265 pagesSBP Consolidated-ReportBilal ZaidiNo ratings yet

- Nepal Budget Highlights FY 78-79Document33 pagesNepal Budget Highlights FY 78-79Shraddha NepalNo ratings yet

- Outlook Asia Pacific Reits Past Present and FutureDocument4 pagesOutlook Asia Pacific Reits Past Present and FutureBe UNo ratings yet

- Annual Report 2022 enDocument236 pagesAnnual Report 2022 endavidbayatNo ratings yet

- JNJNBNDocument28 pagesJNJNBNrodrigo.santucciNo ratings yet

- Business Cycle: DefinitionDocument10 pagesBusiness Cycle: DefinitionSyed ArslanNo ratings yet

- InflationDocument29 pagesInflationÂshùtôsh KúmårNo ratings yet

- 2019.05 - Investor PresentationDocument20 pages2019.05 - Investor PresentationCaio MenezesNo ratings yet

- Capital Market Development in The Philippines: Victor A. AbolaDocument9 pagesCapital Market Development in The Philippines: Victor A. AbolaMilky CoffeeNo ratings yet

- Prices and Inflation: Successful Tight-Rope WalkingDocument28 pagesPrices and Inflation: Successful Tight-Rope WalkingÂshùtôsh KúmårNo ratings yet

- Lecture 1 Economic Growth Potential OutputDocument25 pagesLecture 1 Economic Growth Potential Outputshajea aliNo ratings yet

- Beverage Trends AnalysisDocument49 pagesBeverage Trends AnalysisCarlosNo ratings yet

- Banking: CHAPTER A: Brief About The Indian Banking SectorDocument63 pagesBanking: CHAPTER A: Brief About The Indian Banking SectorDevang ParabNo ratings yet

- AC IR Deck August 2018 27 Slides VF PDFDocument27 pagesAC IR Deck August 2018 27 Slides VF PDFjohn lerry loberioNo ratings yet

- FILE-20211026-121418-Mercer A-2021 Regional Compensation Trends Changing in The Context of Pandemic-RS2021Document34 pagesFILE-20211026-121418-Mercer A-2021 Regional Compensation Trends Changing in The Context of Pandemic-RS2021uyenphuongNo ratings yet

- Coking Coal: Supply, Resource Development and ImportsDocument41 pagesCoking Coal: Supply, Resource Development and ImportsGolchha GroupNo ratings yet

- Accenture Top10 Challenges 2011Document120 pagesAccenture Top10 Challenges 2011남상욱No ratings yet

- Vincom Retail Joint Stock Company 2020 Performance and 2021 OutlookDocument28 pagesVincom Retail Joint Stock Company 2020 Performance and 2021 OutlookNeil NguyenNo ratings yet

- Highlights of Monitary Policy 2020Document15 pagesHighlights of Monitary Policy 2020Raushan KumarNo ratings yet

- Coface Asia Payment Survey 2022 WEBDocument11 pagesCoface Asia Payment Survey 2022 WEBAlae JdyatNo ratings yet

- Budget Analysis: 2009-2010Document11 pagesBudget Analysis: 2009-2010Waseem IshfaqNo ratings yet

- KOTAKBANK - Investor Presentation - 26-May-22 - TickertapeDocument75 pagesKOTAKBANK - Investor Presentation - 26-May-22 - TickertapeAbirami ThevarNo ratings yet

- Report On Indonesia Financial Sector Development Q2 2023Document34 pagesReport On Indonesia Financial Sector Development Q2 2023Raymond SihotangNo ratings yet

- LiquiLoans - LiteratureDocument28 pagesLiquiLoans - LiteratureNeetika SahNo ratings yet

- Metrics MDIF Report July 2022Document2 pagesMetrics MDIF Report July 2022tolstoy1976No ratings yet

- bh1 PDFDocument15 pagesbh1 PDFSiri ConNo ratings yet

- bh1 PDFDocument15 pagesbh1 PDFSiri ConNo ratings yet

- 19 Ijmres 10012020Document12 pages19 Ijmres 10012020International Journal of Management Research and Emerging SciencesNo ratings yet

- Amey Patale 17-19 PGFinanceDocument9 pagesAmey Patale 17-19 PGFinanceAMEY PATALENo ratings yet

- High Uncertainty Weighing On Global Growth OECD Interim Economic Outlook Presentation 20 September 2018Document24 pagesHigh Uncertainty Weighing On Global Growth OECD Interim Economic Outlook Presentation 20 September 2018ngnquyetNo ratings yet

- Asia Macroeconomic Quarterly Update: Cautious Recovery Amid Geopolitical HeadwindsDocument27 pagesAsia Macroeconomic Quarterly Update: Cautious Recovery Amid Geopolitical HeadwindsWilliam TanNo ratings yet

- Sbi PPTDocument59 pagesSbi PPTmisfitmedicoNo ratings yet

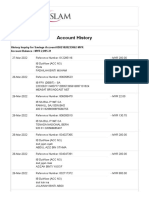

- Baseer Aslam 2047110 ProjectDocument8 pagesBaseer Aslam 2047110 ProjectBaseer AslamNo ratings yet

- World Bank East Asia and Pacific Economic Update, October 2013: Rebuilding Policy Buffers, Reinvigorating GrowthFrom EverandWorld Bank East Asia and Pacific Economic Update, October 2013: Rebuilding Policy Buffers, Reinvigorating GrowthNo ratings yet

- Braced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationFrom EverandBraced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationNo ratings yet

- Regulatory Bodies in India - RBI - 2Document38 pagesRegulatory Bodies in India - RBI - 2omesh gehlotNo ratings yet

- VA - Cashier, G12, HQ AmmanDocument3 pagesVA - Cashier, G12, HQ AmmanMohammad Al-arrabi AldhidiNo ratings yet

- Bank Account StatementDocument11 pagesBank Account StatementJohn SmitNo ratings yet

- Bimb Jan-Mac 2022Document14 pagesBimb Jan-Mac 2022Azirah Abdul AzizNo ratings yet

- Banking SectorDocument8 pagesBanking SectorSupreet KaurNo ratings yet

- Fmi Assignment Time Value of ValueDocument8 pagesFmi Assignment Time Value of ValuerajeshNo ratings yet

- Corporate Finance SyllabusDocument2 pagesCorporate Finance Syllabusshagun guptaNo ratings yet

- Tally With GST Workshop Jan 2023 QuestionDocument3 pagesTally With GST Workshop Jan 2023 QuestionAryan GuptaNo ratings yet

- SWIFT Codes & BIC Codes For All The Banks in TheDocument1 pageSWIFT Codes & BIC Codes For All The Banks in TheGhanem AlamroNo ratings yet

- AP 001 A.1 Bank Reconciliation Prob 1Document2 pagesAP 001 A.1 Bank Reconciliation Prob 1Loid Gumera LenchicoNo ratings yet

- Legal Notice (138) GurudevDocument4 pagesLegal Notice (138) Gurudevpardeep100% (1)

- Challan Form No.32-A: State Bank of PakistanDocument1 pageChallan Form No.32-A: State Bank of PakistanZubair KhanNo ratings yet

- Chapter 24-Money, The Price Level, and InflationDocument33 pagesChapter 24-Money, The Price Level, and InflationBin WangNo ratings yet

- MIS 301 Group Assignment Quesion 3Document3 pagesMIS 301 Group Assignment Quesion 3Mohammad HammadNo ratings yet

- Chapter-22 - Finance Company OperationsDocument17 pagesChapter-22 - Finance Company Operationsmohammad olickNo ratings yet

- Sample Problems On CashDocument9 pagesSample Problems On Cashcriszel4sobejanaNo ratings yet

- Factors Influencing Towards Successful Implementation of CRM Systems in Local Commercial Banks in Sri LankaDocument83 pagesFactors Influencing Towards Successful Implementation of CRM Systems in Local Commercial Banks in Sri LankaArchchana Vek SurenNo ratings yet

- Agricultural Finance and Agricultural Credit-Role of Institutional and Non - Institutional Agencies-Rural IndebtednessDocument30 pagesAgricultural Finance and Agricultural Credit-Role of Institutional and Non - Institutional Agencies-Rural IndebtednessKIRUTHIKANo ratings yet

- Fixed Income SecuritiesDocument12 pagesFixed Income SecuritiesAyana Giragn AÿøNo ratings yet

- Internship Report On A Study On SME BankDocument40 pagesInternship Report On A Study On SME BankAbu Hamzah NomaanNo ratings yet

- Engaging Activity Unit 4 Financial InstitutionDocument2 pagesEngaging Activity Unit 4 Financial InstitutionMary Justine ManaloNo ratings yet

- Chapter 2 - Recording Business TransactionsDocument6 pagesChapter 2 - Recording Business TransactionsHa Phuoc HauNo ratings yet

- Invoice Sample Low VoltageDocument4 pagesInvoice Sample Low Voltagedarlleybee1No ratings yet

- Countingup Statement 2023 07Document1 pageCountingup Statement 2023 07SophiaNo ratings yet

- Credit Risk-COVIDDocument6 pagesCredit Risk-COVIDRazaNo ratings yet

- Bankruptcy NotesDocument6 pagesBankruptcy NotesDhabitah Adriana100% (1)

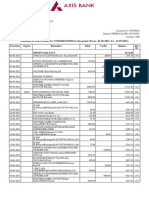

- Statement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Document6 pagesStatement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Anirban DebNo ratings yet

- Interbank GIRO (IBG) : Transaction FeesDocument4 pagesInterbank GIRO (IBG) : Transaction FeesHafizAceNo ratings yet