You might also like

- Assignment On Bankinkg LawDocument14 pagesAssignment On Bankinkg LawrajaramNo ratings yet

- Banking Law Lecture 5Document19 pagesBanking Law Lecture 5hannahlouiseisobelNo ratings yet

- Practice of Banking Lecture Notes 1Document26 pagesPractice of Banking Lecture Notes 1Ganiyu TaslimNo ratings yet

- Banking Theory Law and PracticeDocument68 pagesBanking Theory Law and PracticeMasud Khan ShakilNo ratings yet

- Banking Theory, Law and Practice - CCR8C43Document68 pagesBanking Theory, Law and Practice - CCR8C43shahid3333No ratings yet

- Banking Law and PracticeDocument59 pagesBanking Law and PracticeThanga Durai100% (2)

- Banking RelationshipsDocument68 pagesBanking RelationshipsHage Matin0% (1)

- Firm C7 Workshop One (Banking)Document22 pagesFirm C7 Workshop One (Banking)MUBANGIZI ABBYNo ratings yet

- Banking Theory Law and Practice: Directorate of Distance & Continuing EducationDocument76 pagesBanking Theory Law and Practice: Directorate of Distance & Continuing Educationbackupsanthosh21 dataNo ratings yet

- Banking Law and Customer RelationshipsDocument8 pagesBanking Law and Customer RelationshipsAbdul basitNo ratings yet

- The Banking and Financial Institutions Act 1989Document4 pagesThe Banking and Financial Institutions Act 1989Rita LakhsmiNo ratings yet

- Banker-Customer - Relationship: Nature, Types-General and Special Including Legal AspectsDocument61 pagesBanker-Customer - Relationship: Nature, Types-General and Special Including Legal AspectsSaiful IslamNo ratings yet

- Banker and Customer RelationshipDocument71 pagesBanker and Customer RelationshipMani 0000No ratings yet

- Banker - Customer RelationshipDocument18 pagesBanker - Customer Relationshipjoel minaniNo ratings yet

- Chapter Four The Bank - Customer RelashinshipDocument11 pagesChapter Four The Bank - Customer RelashinshipNigus MollaNo ratings yet

- Banking Theory and Practice Chapter TwoDocument40 pagesBanking Theory and Practice Chapter Twomubarek oumerNo ratings yet

- Banking ProjectDocument69 pagesBanking Projectठलुआ क्लब100% (1)

- Banker Customer RelationshipDocument25 pagesBanker Customer Relationshiprajin_rammstein100% (1)

- BANKER-CUSTOMER RELATINSHIP DEFINEDDocument5 pagesBANKER-CUSTOMER RELATINSHIP DEFINEDFun DietNo ratings yet

- Chapter2 PDFDocument9 pagesChapter2 PDFnurulkhairunnajahNo ratings yet

- Fiduciary Duties of BanksDocument8 pagesFiduciary Duties of BanksTimothy Nshimbi0% (1)

- Banking 2Document13 pagesBanking 2Abhishek SharmaNo ratings yet

- Payyyyyying Banker and Collllllecting Banker by Chu PersonDocument59 pagesPayyyyyying Banker and Collllllecting Banker by Chu PersonSahirAaryaNo ratings yet

- Banking Law and OperationsDocument35 pagesBanking Law and OperationsViraja GuruNo ratings yet

- Law of Banking and Negotiabl InsrumentsDocument23 pagesLaw of Banking and Negotiabl Insrumentsfocus moreNo ratings yet

- Sjec Theory & Practices of Banking CPDocument20 pagesSjec Theory & Practices of Banking CPgastro8606342No ratings yet

- Banker Customer RelationshipDocument65 pagesBanker Customer RelationshipNeeta SharmaNo ratings yet

- Banking & Business Laws GuideDocument8 pagesBanking & Business Laws GuideRoqaia AlwanNo ratings yet

- Banker NotesDocument134 pagesBanker NotesEdward MokweriNo ratings yet

- Admass University: Chapter Four Bank Customer RelationshipDocument7 pagesAdmass University: Chapter Four Bank Customer RelationshipMk FisihaNo ratings yet

- Banker - Customer RelationshipDocument42 pagesBanker - Customer Relationshipashutosh srivastavaNo ratings yet

- Sjec Theory & Practices of Banking Mansoor C PDocument20 pagesSjec Theory & Practices of Banking Mansoor C PShams TabrezNo ratings yet

- BLO Unit 1-1Document24 pagesBLO Unit 1-1Mohammad MAAZNo ratings yet

- Banker-Customer Relationship: Rights and ResponsibilitiesDocument33 pagesBanker-Customer Relationship: Rights and ResponsibilitiesFerdous AlaminNo ratings yet

- Banking Business DefinitionDocument6 pagesBanking Business Definitiontai JtNo ratings yet

- Acca Fundamentals of Accounting (FA1)Document24 pagesAcca Fundamentals of Accounting (FA1)Paredes FlozerenziNo ratings yet

- Banker Customer RelationshipDocument7 pagesBanker Customer Relationshipvivekananda RoyNo ratings yet

- FIRM A2-WORKSHOP 1-Corporate & Commercial Practice-Term 3-Week 2Document43 pagesFIRM A2-WORKSHOP 1-Corporate & Commercial Practice-Term 3-Week 2MUBANGIZI ABBYNo ratings yet

- Types of BankingDocument2 pagesTypes of BankingplmokmNo ratings yet

- Bank - CustomerDocument17 pagesBank - CustomerPremah BalasundramNo ratings yet

- Chapter 3 - CustomerDocument2 pagesChapter 3 - CustomerJoanne J. NgNo ratings yet

- Relationship Between Banker and CustomerDocument16 pagesRelationship Between Banker and CustomeraliishaanNo ratings yet

- Unit-Iv: Meaning of A Banking CompanyDocument39 pagesUnit-Iv: Meaning of A Banking CompanyVandana SharmaNo ratings yet

- Banking Law week 2Document3 pagesBanking Law week 2jonathannightingale2003No ratings yet

- Banking Law Unit 3Document38 pagesBanking Law Unit 3RHEA VIJU SAMUEL 1850355No ratings yet

- Legal Aspect of Banker Customer RelationshipDocument26 pagesLegal Aspect of Banker Customer RelationshipPranjal Srivastava100% (10)

- Firm C6 Workshop 1 Banking Term 3Document29 pagesFirm C6 Workshop 1 Banking Term 3MUBANGIZI ABBYNo ratings yet

- The Banker-Customer RelationshipDocument31 pagesThe Banker-Customer RelationshipStefan Adrian VanceaNo ratings yet

- 1 Commercial BKG BasicsDocument21 pages1 Commercial BKG BasicsRAHUL GUPTANo ratings yet

- Understanding the Relationship Between Bankers and CustomersDocument9 pagesUnderstanding the Relationship Between Bankers and CustomersAbiyNo ratings yet

- Banker-Customer Relationship: M A H Sazzad ShikderDocument14 pagesBanker-Customer Relationship: M A H Sazzad ShikderManish KumarNo ratings yet

- 02B Banker-Customer RelationshipDocument34 pages02B Banker-Customer RelationshipHend JawiNo ratings yet

- Banking Theory Law and PracticeDocument29 pagesBanking Theory Law and Practicereshma100% (2)

- Summary On The Law On Banking and Negotiable InstrumentsDocument48 pagesSummary On The Law On Banking and Negotiable InstrumentsJACKIE MUGABENo ratings yet

- Banker Customer Relationship: Nature, Type - General and SpecialDocument59 pagesBanker Customer Relationship: Nature, Type - General and Specialrajin_rammsteinNo ratings yet

- Fundamental f Banking Law-1Document88 pagesFundamental f Banking Law-1ramadhanamos620No ratings yet

- Banking Handouts CH - 4Document7 pagesBanking Handouts CH - 4Kamal SirsjNo ratings yet

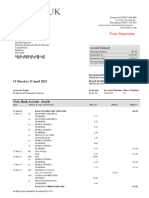

- 2023 04 12 - StatementDocument6 pages2023 04 12 - StatementRay JouwenaNo ratings yet

- Commissions Received by A GuarantorDocument18 pagesCommissions Received by A GuarantorMoud KhalfaniNo ratings yet

- XI Revision Notes On BRSDocument6 pagesXI Revision Notes On BRSJay muthaNo ratings yet

- Chapter - 1 Working Capital Management - Introduction 1.1Document41 pagesChapter - 1 Working Capital Management - Introduction 1.1ChetanNo ratings yet

- Assignment 2 PGDMDocument2 pagesAssignment 2 PGDMniftamNo ratings yet

- Study on Financial Services of HDFC BankDocument71 pagesStudy on Financial Services of HDFC BankNeha PassiNo ratings yet

- Honda Analysis of Cash ManagementDocument74 pagesHonda Analysis of Cash Managementnishikantsingh647No ratings yet

- Datuk Jagindar Singh & Ors V Tara Rajaratnam, (1983) 2Document18 pagesDatuk Jagindar Singh & Ors V Tara Rajaratnam, (1983) 2ainur syamimiNo ratings yet

- Auto Debit Form (60801026)Document2 pagesAuto Debit Form (60801026)Hanafi AminNo ratings yet

- Fortis Microfinance Bank Credit Policy Manual Update SummaryDocument99 pagesFortis Microfinance Bank Credit Policy Manual Update SummaryBattogtokh AzjargalNo ratings yet

- Premier Account Welcome PackDocument122 pagesPremier Account Welcome PackericNo ratings yet

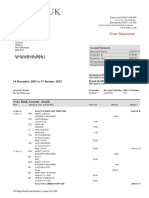

- 2022 01 13 - StatementDocument8 pages2022 01 13 - StatementToni MirosanuNo ratings yet

- Commercial BankDocument11 pagesCommercial BankVaibhavi BorhadeNo ratings yet

- +functions of Commercial BanksDocument15 pages+functions of Commercial Banksredarrow05No ratings yet

- Bank Account Management SimulatorDocument3 pagesBank Account Management Simulatorbik0009No ratings yet

- Loan Application Form: Personal DetailsDocument8 pagesLoan Application Form: Personal DetailsNihar KNo ratings yet

- Your Business Advantage Relationship Banking Preferred Rewards For Bus PlatinumDocument12 pagesYour Business Advantage Relationship Banking Preferred Rewards For Bus PlatinumUsm am50% (2)

- Debt Recovery Management of SBIDocument12 pagesDebt Recovery Management of SBIDipanjan DasNo ratings yet

- TdBank EditavelDocument4 pagesTdBank Editaveltudo doidoNo ratings yet

- NegoDocument201 pagesNegoRonna Faith MonzonNo ratings yet

- Financial Management Lecture NoteDocument50 pagesFinancial Management Lecture NoteTuryamureeba JuliusNo ratings yet

- Business Lending TCs For Juristic in Out NCA 032018Document10 pagesBusiness Lending TCs For Juristic in Out NCA 032018Jade FrostNo ratings yet

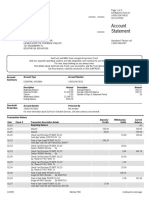

- Bank Statement LanayaDocument3 pagesBank Statement LanayashrondaNo ratings yet

- Writing 2Document19 pagesWriting 2babyNo ratings yet

- Survey - Financial Products For MSME 1Document10 pagesSurvey - Financial Products For MSME 1Mira A KumarNo ratings yet

- 111 A Level Accounting P1 MCQs TopicalDocument27 pages111 A Level Accounting P1 MCQs TopicalRead and Write Publications80% (5)

- Carol Coye Benson - Scott J Loftesness - Payments Systems in The U.S. - A Guide For The Payments Professional-Glenbrook Partners (2013)Document149 pagesCarol Coye Benson - Scott J Loftesness - Payments Systems in The U.S. - A Guide For The Payments Professional-Glenbrook Partners (2013)Chico TonhosoNo ratings yet

- Chapter One Institutional OverviewDocument66 pagesChapter One Institutional OverviewLayal HasanNo ratings yet

- Terms and Conditions Governing Accounts PDFDocument13 pagesTerms and Conditions Governing Accounts PDFlontong4925No ratings yet

- CC GiroDocument1 pageCC GirohjwhtfvttrvakjjchoNo ratings yet