You might also like

- 11 - Chapter 8 PDFDocument21 pages11 - Chapter 8 PDFJugal ThakkarNo ratings yet

- A Study On Housing Finance Scheme and Its Tax Benefits With Special Reference To HDFC BankDocument99 pagesA Study On Housing Finance Scheme and Its Tax Benefits With Special Reference To HDFC BankDipesh KumarNo ratings yet

- INTRODUCTIONDocument29 pagesINTRODUCTIONDostar ChuNo ratings yet

- The Major Challenges Faced by Housing Finance Company in IndiaDocument6 pagesThe Major Challenges Faced by Housing Finance Company in IndiaAARYA SATAVNo ratings yet

- Competitive Dynamics of Indian Housing Finance Industry-LibreDocument28 pagesCompetitive Dynamics of Indian Housing Finance Industry-LibreSaket GokhaleNo ratings yet

- Comparative Study On Home Loan SBI Vs ICICI BankDocument78 pagesComparative Study On Home Loan SBI Vs ICICI BankDostar Chu100% (1)

- UntitledDocument75 pagesUntitledDostar ChuNo ratings yet

- Housing Finance: Submitted By: Submitted ToDocument20 pagesHousing Finance: Submitted By: Submitted ToAayush KoolwalNo ratings yet

- Project Report: Submitted by Namrata Makhija College Roll No.: 195 Shri Ram College of Commerce University of DelhiDocument30 pagesProject Report: Submitted by Namrata Makhija College Roll No.: 195 Shri Ram College of Commerce University of DelhiDhruv KapoorNo ratings yet

- Improving The Life of MassesDocument6 pagesImproving The Life of MassesAnish NarulaNo ratings yet

- 1.1 Background of The Study: Housing Finance EvaluationDocument22 pages1.1 Background of The Study: Housing Finance Evaluationapurva guldagadNo ratings yet

- 1.1 Home LoanDocument36 pages1.1 Home LoanRishi BhatnagarNo ratings yet

- Housing Finance SystemsDocument45 pagesHousing Finance SystemsPriyanka100% (1)

- Understanding Home Loans in India: A Comprehensive GuideDocument22 pagesUnderstanding Home Loans in India: A Comprehensive GuideDostar ChuNo ratings yet

- A Study On Credit Appraisal: Mes Institute of ManagementDocument7 pagesA Study On Credit Appraisal: Mes Institute of ManagementnageshsamNo ratings yet

- English বাং লা हिहंदी मराठी Follow UsDocument13 pagesEnglish বাং লা हिहंदी मराठी Follow UsMohammad Khurram QureshiNo ratings yet

- A Study On Role of Financial Institutions in Providing Housing Loans To Middle Income Group in Bangalore City.Document72 pagesA Study On Role of Financial Institutions in Providing Housing Loans To Middle Income Group in Bangalore City.Nadeem Naddu100% (1)

- Chapter 2 Literature ReviewDocument24 pagesChapter 2 Literature Reviewcoolpeer91No ratings yet

- In-Depth Study of Housing Finance SectorDocument134 pagesIn-Depth Study of Housing Finance SectorSnehraj AmburleNo ratings yet

- HDFC's Role in India's Housing Finance SectorDocument103 pagesHDFC's Role in India's Housing Finance SectorBhawna Singh100% (1)

- Housing NotesDocument59 pagesHousing Notessaahasitha 14No ratings yet

- Home Loan - ProjectDocument35 pagesHome Loan - ProjectSachin Prakash100% (1)

- IMPLEMENTING INDONESIA'S NEW HOUSING POLICY:THE WAY FORWARD. DraftDocument77 pagesIMPLEMENTING INDONESIA'S NEW HOUSING POLICY:THE WAY FORWARD. DraftOswar MungkasaNo ratings yet

- Lecture 1-CHALLENGES IN HOUSINGDocument25 pagesLecture 1-CHALLENGES IN HOUSINGWesley SuguitanNo ratings yet

- Study Credit Appraisal Systems of HDFC and SBI Home LoansDocument72 pagesStudy Credit Appraisal Systems of HDFC and SBI Home LoansSimreen HuddaNo ratings yet

- A Study On Home Loans - SbiDocument57 pagesA Study On Home Loans - Sbirajesh bathulaNo ratings yet

- IntroductionDocument57 pagesIntroductionPrakash JoshuaNo ratings yet

- Literature ReviewDocument3 pagesLiterature ReviewBiswadeep Das0% (1)

- Financial ServicesDocument18 pagesFinancial ServicesRohit SoniNo ratings yet

- Growth of Housing Finance in IndiaDocument13 pagesGrowth of Housing Finance in IndiaVaibhav1508No ratings yet

- Housing AgenciesDocument21 pagesHousing AgenciesAsin AntoNo ratings yet

- Housing Overview - Shortage and Development: Chapter-IDocument41 pagesHousing Overview - Shortage and Development: Chapter-ICHALLA MOUNICANo ratings yet

- A Study On Home Loans - SbiDocument69 pagesA Study On Home Loans - Sbirajesh bathula100% (1)

- Lic Housing Finance-1Document44 pagesLic Housing Finance-1Abdul RasheedNo ratings yet

- Study On The Role of Financial Institutions in Providing Housing Loans To Middle Income Group in Mumbai CityDocument7 pagesStudy On The Role of Financial Institutions in Providing Housing Loans To Middle Income Group in Mumbai Cityneenad lopesNo ratings yet

- Indian Real Estate Sector - Handbook 2011Document37 pagesIndian Real Estate Sector - Handbook 2011Shaikh Abdur RahmanNo ratings yet

- Project Report On Financial InstitutionDocument86 pagesProject Report On Financial Institutionarchana_anuragi83% (6)

- IntroductionDocument1 pageIntroductionAsmita PatilNo ratings yet

- Fundamental Analysis Economy Analysis: TaxationDocument54 pagesFundamental Analysis Economy Analysis: Taxationvivek0020100% (1)

- Indian Mortgages IndustryDocument16 pagesIndian Mortgages IndustryChintan SharmaNo ratings yet

- Housing Finance System in India and China - An Exploratory InvestigationDocument18 pagesHousing Finance System in India and China - An Exploratory InvestigationatuljndalNo ratings yet

- Update #13 Current Affairs Topic Listing 3: National IssuesDocument18 pagesUpdate #13 Current Affairs Topic Listing 3: National IssuesMayank GoswamiNo ratings yet

- Housing FinanceDocument18 pagesHousing FinanceSanket AiyaNo ratings yet

- Chapters - 2,3,4.Document28 pagesChapters - 2,3,4.R.Siddharth ReddyNo ratings yet

- 1V Housing Finance Schemes in India An AnalysisDocument50 pages1V Housing Finance Schemes in India An AnalysisKishan KumarNo ratings yet

- Final SIPDocument5 pagesFinal SIPSonali ChaudharyNo ratings yet

- Housing Finance Industry in India During CovidDocument108 pagesHousing Finance Industry in India During CovidLaksh BansalNo ratings yet

- Report On Trend and Progress of Housing in India 2013Document15 pagesReport On Trend and Progress of Housing in India 2013Nihar NanyamNo ratings yet

- Objective: Fundamental Analysis of Real Estate Sector in IndiaDocument44 pagesObjective: Fundamental Analysis of Real Estate Sector in IndiaDnyaneshwar DaundNo ratings yet

- Housing Finance: Presented by Sulekha Beri I.D.NO .43847Document46 pagesHousing Finance: Presented by Sulekha Beri I.D.NO .43847mehakdadwalNo ratings yet

- India Housing Report 2002Document56 pagesIndia Housing Report 2002sgjatharNo ratings yet

- NHB's Way Forward for Housing FinanceDocument13 pagesNHB's Way Forward for Housing FinancepvenkyNo ratings yet

- Table of ContentDocument19 pagesTable of ContentRohit ShahNo ratings yet

- The Indian Housing Finance Market - Going FlatDocument17 pagesThe Indian Housing Finance Market - Going FlatAbhishek NambiarNo ratings yet

- Study of Housing Finance Sectors in Pre and Post Pandemic Situation in INDIA IntroDocument17 pagesStudy of Housing Finance Sectors in Pre and Post Pandemic Situation in INDIA IntroSharanya ShettyNo ratings yet

- Comparative Study Housing Loans SBI UBIDocument4 pagesComparative Study Housing Loans SBI UBINaresh HariyaniNo ratings yet

- India Budget 2011Document8 pagesIndia Budget 2011Dinesh SharmaNo ratings yet

- Me Research Paper Pes1202202920Document11 pagesMe Research Paper Pes1202202920The Desi TrevorNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Managing Business Finances: Section 17.1Document18 pagesManaging Business Finances: Section 17.1Thiên TíuNo ratings yet

- NAME: Jimenez, Ross John C. Year-Course-Section: 3-BSMA-A: InstrumentsDocument2 pagesNAME: Jimenez, Ross John C. Year-Course-Section: 3-BSMA-A: InstrumentsRoss John JimenezNo ratings yet

- 01 Quiz 1Document3 pages01 Quiz 1Emperor SavageNo ratings yet

- RHBM 0034 RHB Card Application Forms - Generic - Rev12 - FINAL PDFDocument11 pagesRHBM 0034 RHB Card Application Forms - Generic - Rev12 - FINAL PDFTina0% (1)

- January February Ta 2023Document40 pagesJanuary February Ta 2023ManuelNo ratings yet

- Acumen's Vision for the Future of Impact InvestingDocument51 pagesAcumen's Vision for the Future of Impact InvestingBassel HassanNo ratings yet

- Nippon Paint Group Medium-Term Plan (FY2021-2023) Update ReportDocument36 pagesNippon Paint Group Medium-Term Plan (FY2021-2023) Update ReportRahiNo ratings yet

- Lesson 17 PDFDocument36 pagesLesson 17 PDFNelwan NatanaelNo ratings yet

- 2 - Secrecy of Bank DepositsDocument14 pages2 - Secrecy of Bank Depositsrandyblanza2014No ratings yet

- Fed Statements Side by SideDocument1 pageFed Statements Side by SideTaylor CottamNo ratings yet

- Role of Sebi - As A Regulatory AuthorityDocument4 pagesRole of Sebi - As A Regulatory Authoritysneha sumanNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document7 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961AshishNo ratings yet

- 62 - 71 Lecture Notes SOCF (1-10)Document5 pages62 - 71 Lecture Notes SOCF (1-10)manadish nawazNo ratings yet

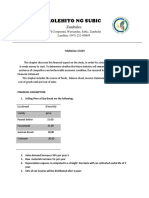

- Kolehiyo NG Subic: ZambalesDocument3 pagesKolehiyo NG Subic: ZambalesRodeliza DuncanNo ratings yet

- ACC622 Assignment 2021Document5 pagesACC622 Assignment 2021Nosisa SithebeNo ratings yet

- International Business Management: AssignmentDocument16 pagesInternational Business Management: AssignmentkeshavNo ratings yet

- Greenlam IndustriesDocument8 pagesGreenlam Industriesvikasaggarwal01No ratings yet

- Families That Rule The WorldDocument5 pagesFamilies That Rule The WorldAries0104No ratings yet

- A Project Report On: "Research On Capital Market With Indiainfoline LTDDocument94 pagesA Project Report On: "Research On Capital Market With Indiainfoline LTDgauravNo ratings yet

- Federal Deposit Insurance Corporation, A United States Corporation, Plaintiff v. Bank of Boulder, A Colorado Corporation, 865 F.2d 1134, 10th Cir. (1988)Document24 pagesFederal Deposit Insurance Corporation, A United States Corporation, Plaintiff v. Bank of Boulder, A Colorado Corporation, 865 F.2d 1134, 10th Cir. (1988)Scribd Government DocsNo ratings yet

- Bank of America Mortgage Settlement DocumentsDocument317 pagesBank of America Mortgage Settlement DocumentsFindLaw100% (1)

- Nepal Accounting Standard 24 Related Party DisclosureDocument2 pagesNepal Accounting Standard 24 Related Party Disclosurebinu0% (1)

- Order in The Matter of Pailan Agro India Limited and Its DirectorsDocument14 pagesOrder in The Matter of Pailan Agro India Limited and Its DirectorsShyam SunderNo ratings yet

- Dicionário - Pinheiro NetoDocument167 pagesDicionário - Pinheiro NetoBernardo CruzNo ratings yet

- SEC Form 17-C Dito CME Re Change in Officers and Directors (11 October 2023)Document3 pagesSEC Form 17-C Dito CME Re Change in Officers and Directors (11 October 2023)judy jace thaddeus AlejoNo ratings yet

- Bill Gates Profile and Milestone AchievementsDocument72 pagesBill Gates Profile and Milestone AchievementsvaibhavNo ratings yet

- Chase 1099int 2013Document2 pagesChase 1099int 2013Srikala Venkatesan100% (1)

- Balance Sheet TemplateDocument16 pagesBalance Sheet TemplateRyou ShinodaNo ratings yet

- Hedging PDFDocument6 pagesHedging PDFIraiven ShanmugamNo ratings yet

- Gitman 4e Ch. 2 SPR - SolDocument8 pagesGitman 4e Ch. 2 SPR - SolDaniel Joseph SitoyNo ratings yet