You might also like

- Conservative Formula by Pim Van VlietDocument21 pagesConservative Formula by Pim Van VlietEric John JutaNo ratings yet

- Assignment (Quiz) 2 ESG Controversies and Controversial ESG About Silent Saints and SmallDocument8 pagesAssignment (Quiz) 2 ESG Controversies and Controversial ESG About Silent Saints and SmallkashifalimuzzaffarNo ratings yet

- How To Measure Corporate Social Responsibility WP 11-4Document23 pagesHow To Measure Corporate Social Responsibility WP 11-4Yaqub AbdulaNo ratings yet

- CFR 19 04Document31 pagesCFR 19 04AlexNo ratings yet

- Bilbao-Terol (2012) Fuzyy Approach - A Fuzzy Multi-Objective Approach For Sustainable InvestmentsDocument12 pagesBilbao-Terol (2012) Fuzyy Approach - A Fuzzy Multi-Objective Approach For Sustainable InvestmentsGebrehanaNo ratings yet

- Corporate Sustainability First Evidence On MaterialityDocument55 pagesCorporate Sustainability First Evidence On MaterialityIm NiNo ratings yet

- ESG Controversies and Controversial ESG: About Silent Saints and Small SinnersDocument20 pagesESG Controversies and Controversial ESG: About Silent Saints and Small SinnersAmal AouadiNo ratings yet

- The Wages of Social Responsibility Where Are TheyDocument11 pagesThe Wages of Social Responsibility Where Are TheyNguyen Quang PhuongNo ratings yet

- Backtesting ESG Factor Investing StrategiesDocument9 pagesBacktesting ESG Factor Investing StrategiesLoulou DePanamNo ratings yet

- Risks: U.S. Equity Mean-Reversion ExaminedDocument14 pagesRisks: U.S. Equity Mean-Reversion ExaminedJonathan FelchNo ratings yet

- ESG Scores and Its Influence On Firm Per20160223-5154-299c3o-With-Cover-Page-V2Document33 pagesESG Scores and Its Influence On Firm Per20160223-5154-299c3o-With-Cover-Page-V2Oluwatoyin Esther AkintundrNo ratings yet

- Is ESG An Equity Factor or Just An Investment GuideDocument11 pagesIs ESG An Equity Factor or Just An Investment GuideHong DingNo ratings yet

- ESG Ratings and Indexes Are A Crucial Component of How Business Is Done in The TwentyDocument3 pagesESG Ratings and Indexes Are A Crucial Component of How Business Is Done in The TwentyShreya ChakrabortyNo ratings yet

- SZV 2Document19 pagesSZV 2sorinsilviuNo ratings yet

- ESG Factors and Risk-Adjusted Performance A New Quantitative ModelDocument10 pagesESG Factors and Risk-Adjusted Performance A New Quantitative Modelalejandro315amNo ratings yet

- García (2019) Selecting Socially Responsible Portfolios A Fuzzy MCriteria ApproachDocument14 pagesGarcía (2019) Selecting Socially Responsible Portfolios A Fuzzy MCriteria ApproachGebrehanaNo ratings yet

- Strategic Asset Allocation and The Role of Alternative InvestmentsDocument27 pagesStrategic Asset Allocation and The Role of Alternative InvestmentsMohamed hassan adamNo ratings yet

- A New Way of Seeing ValueDocument4 pagesA New Way of Seeing ValueLeeNo ratings yet

- Review of LiteratureDocument7 pagesReview of LiteratureAshish KumarNo ratings yet

- The Effectiveness of Socially Responsible Investment A ReviewDocument19 pagesThe Effectiveness of Socially Responsible Investment A Reviewwawa1303No ratings yet

- Lec 7 The Role of ESG CriteriaDocument22 pagesLec 7 The Role of ESG CriteriaSoumojit KumarNo ratings yet

- Why and How Investors Use Esg Information Evidence From A GlobalDocument41 pagesWhy and How Investors Use Esg Information Evidence From A GlobalHENI YUSNITANo ratings yet

- Corporate Governance and Financial Characteristic Effects On The Extent of Corporate Social Responsibility DisclosureDocument23 pagesCorporate Governance and Financial Characteristic Effects On The Extent of Corporate Social Responsibility DisclosurePrahesti Ayu WulandariNo ratings yet

- E Iris Global Sustain Bail It y Report 2012Document8 pagesE Iris Global Sustain Bail It y Report 2012danjwelchNo ratings yet

- Rameez Shakaib MSA 3123Document7 pagesRameez Shakaib MSA 3123OsamaMazhariNo ratings yet

- Sustainable FinanceDocument5 pagesSustainable FinanceShahad AsiriNo ratings yet

- Bekkers 2009Document33 pagesBekkers 2009Mayank JainNo ratings yet

- Jurnal InternasionalDocument47 pagesJurnal InternasionalRomario AnnurNo ratings yet

- Disclosure on sustainable development, CSR environmental disclosure and greater value recognized to the company by usersFrom EverandDisclosure on sustainable development, CSR environmental disclosure and greater value recognized to the company by usersNo ratings yet

- SSRN Id2381435Document97 pagesSSRN Id2381435TBP_Think_TankNo ratings yet

- Cardebat and SirvenDocument8 pagesCardebat and SirvenDhirendra Kumar PandaNo ratings yet

- Journal of Cleaner Production: Pablo Vilas, Laura Andreu, Jos e Luis SartoDocument14 pagesJournal of Cleaner Production: Pablo Vilas, Laura Andreu, Jos e Luis SartoCLABERT VALENTIN AGUILAR ALEJONo ratings yet

- Corporate Environmental PerformanceDocument35 pagesCorporate Environmental Performancesymphs88No ratings yet

- Beta EstimationDocument21 pagesBeta EstimationShachi RaiNo ratings yet

- Do SRI ETFs Create ValueDocument44 pagesDo SRI ETFs Create ValueMohammed ZakriyaNo ratings yet

- A Comprehensive Look at The Empirical Performance of Equity Premium PredictionDocument55 pagesA Comprehensive Look at The Empirical Performance of Equity Premium Predictionzhaofengtian123No ratings yet

- Fmi - Final Report - Ayush Kumar - Fin (B)Document5 pagesFmi - Final Report - Ayush Kumar - Fin (B)ayush kumarNo ratings yet

- It Is Not Only What You Say, But How You Say It - ESG, Corporate News, and The Impact On CDS SpreadsDocument14 pagesIt Is Not Only What You Say, But How You Say It - ESG, Corporate News, and The Impact On CDS SpreadsEdna AparecidaNo ratings yet

- 5 - 3 - Li - Dang - Tobin Q and ROA2017Document59 pages5 - 3 - Li - Dang - Tobin Q and ROA2017Harsono Edwin PuspitaNo ratings yet

- Drempetic 2019Document28 pagesDrempetic 2019Ahmadi AliNo ratings yet

- Financial Analysis On Mutual Fund Schemes With Special Reference To SBI Mutual Fund CoimbatoreDocument6 pagesFinancial Analysis On Mutual Fund Schemes With Special Reference To SBI Mutual Fund CoimbatoreCheruv SoniyaNo ratings yet

- 1 PBDocument15 pages1 PBVinicius RodriguesNo ratings yet

- 8 Equity Valuation Using MultiplesDocument40 pages8 Equity Valuation Using MultiplesHuicai MaiNo ratings yet

- LOW-CARBON INVESTING: Defending the Climate - Emphasizing PerformanceFrom EverandLOW-CARBON INVESTING: Defending the Climate - Emphasizing PerformanceNo ratings yet

- ESG Investing - A Short Guide To Implementation: 11 September 2018Document7 pagesESG Investing - A Short Guide To Implementation: 11 September 2018Abdulrahman JradiNo ratings yet

- ESG Performance and Disclosure A Cross-Country AnalysisDocument45 pagesESG Performance and Disclosure A Cross-Country Analysis111 333No ratings yet

- Voluntary Nonfinancial Disclosure and The Cost of Equity Capital PDFDocument43 pagesVoluntary Nonfinancial Disclosure and The Cost of Equity Capital PDFMark NarcisoNo ratings yet

- 02# Are Investors Willing To Sacrifice Cash or MoralityDocument16 pages02# Are Investors Willing To Sacrifice Cash or MoralityYulisnawatiAbbasNo ratings yet

- Which Corporate ESG News Does The Market React To?: George Serafeim Aaron YoonDocument34 pagesWhich Corporate ESG News Does The Market React To?: George Serafeim Aaron YoonRaúl MorenoNo ratings yet

- Life Cycle TheoryDocument14 pagesLife Cycle TheoryolapetersNo ratings yet

- International Review of Financial Analysis: Hala Abdul Kader, Mike Adams, Philip Hardwick, W. Jean KwonDocument3 pagesInternational Review of Financial Analysis: Hala Abdul Kader, Mike Adams, Philip Hardwick, W. Jean KwonTrisna Taufik DarmawansyahNo ratings yet

- Raghunandan Rajgopal 2022Document42 pagesRaghunandan Rajgopal 2022severi.a.i.salonenNo ratings yet

- ESG in Private EquityDocument45 pagesESG in Private Equitythefrederation100% (2)

- A Dea Comparison of Systematic and Lump Sum Investment in Mutual FundsDocument10 pagesA Dea Comparison of Systematic and Lump Sum Investment in Mutual FundspramodppppNo ratings yet

- EDHEC Working Paper Revisiting Mutual Fund Performance F PDFDocument23 pagesEDHEC Working Paper Revisiting Mutual Fund Performance F PDFKostas IordanidisNo ratings yet

- Difficult TimesDocument18 pagesDifficult TimesMichael Iliste von RoopNo ratings yet

- SSRN Id3816592Document76 pagesSSRN Id3816592Novi AnriNo ratings yet

- Legal vs. Normative CSR: Differential Impact On Analyst Dispersion, Stock Return Volatility, Cost of Capital, and Firm ValueDocument21 pagesLegal vs. Normative CSR: Differential Impact On Analyst Dispersion, Stock Return Volatility, Cost of Capital, and Firm ValuesinagadianNo ratings yet

- Hedge Fund Replication: A Model Combination Approach: Michael O'Doherty N. E. Savin Ashish TiwariDocument44 pagesHedge Fund Replication: A Model Combination Approach: Michael O'Doherty N. E. Savin Ashish TiwariTarun SharmaNo ratings yet

- Term Paper Insurance CompanyDocument24 pagesTerm Paper Insurance CompanyartusharNo ratings yet

- 6-Bonds Business Finance MRM (Yield Curve - Bonds)Document37 pages6-Bonds Business Finance MRM (Yield Curve - Bonds)faizy24No ratings yet

- 3 Capital MarketsDocument98 pages3 Capital Marketsvijay kumarNo ratings yet

- A Beginner's Guide To Altcoin Day TradingDocument16 pagesA Beginner's Guide To Altcoin Day Tradingblowinzips67% (6)

- Chapter 4 - Financial InstrumentsDocument17 pagesChapter 4 - Financial InstrumentsMerge MergeNo ratings yet

- Financial Management TheoryDocument4 pagesFinancial Management TheoryCMAStudyNo ratings yet

- Going Rate PricingDocument3 pagesGoing Rate PricingHarshitha RNo ratings yet

- Sample Cap TableDocument1 pageSample Cap TablenewyuppieNo ratings yet

- Collapse of Silicon Valley BankDocument4 pagesCollapse of Silicon Valley BankMohammad MirajNo ratings yet

- AAIB Money Market Fund (Juman) : Fact Sheet JuneDocument1 pageAAIB Money Market Fund (Juman) : Fact Sheet Juneapi-237717884No ratings yet

- Target Costing TutorialDocument2 pagesTarget Costing TutorialJosephat LisiasNo ratings yet

- Ratio Analysis of LICDocument31 pagesRatio Analysis of LICpareekkuldeep0% (1)

- Effect of Price Tag On Customer LoyaltyDocument50 pagesEffect of Price Tag On Customer LoyaltyJulius YarNo ratings yet

- Uv8035 Xls EngDocument9 pagesUv8035 Xls EngMadhav Chowdary TumpatiNo ratings yet

- The Way To Trade Forex by Jay LakhaniDocument98 pagesThe Way To Trade Forex by Jay LakhaniGabriella Nagy100% (1)

- 20 Chapter - 20 - Effective - Interest - Method PDFDocument25 pages20 Chapter - 20 - Effective - Interest - Method PDFSheila Grace BajaNo ratings yet

- What Is A DepositoryDocument10 pagesWhat Is A DepositoryKrishna Gopal MazumdarNo ratings yet

- Foreign Exchange RiskDocument16 pagesForeign Exchange RiskPraneela100% (1)

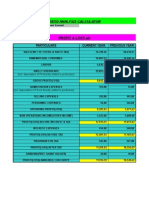

- Ratio Analysis Calculator: Particulars Current Year Previous YearDocument14 pagesRatio Analysis Calculator: Particulars Current Year Previous Yearnarasi64No ratings yet

- Top 10 Credit Rating Agencies in WorldDocument3 pagesTop 10 Credit Rating Agencies in Worldvmktpt100% (4)

- PE Interview Technical Collection - 0Document4 pagesPE Interview Technical Collection - 0Politics RedefinedNo ratings yet

- CampDocument70 pagesCampLyle RabasanoNo ratings yet

- IDSBA - Rough - DataDocument19 pagesIDSBA - Rough - DataVivek VashisthaNo ratings yet

- Training ExercisesDocument4 pagesTraining ExercisesnyNo ratings yet

- Mark McRae - Trading For Beginners PDFDocument102 pagesMark McRae - Trading For Beginners PDFAj Jota100% (4)

- IA1 Cash and Cash EquivalentsDocument20 pagesIA1 Cash and Cash EquivalentsJohn Rainier QuijadaNo ratings yet

- Interest Rate Risk in The Banking Book (IRRBB) : John N.ChalouhiDocument15 pagesInterest Rate Risk in The Banking Book (IRRBB) : John N.Chalouhijadcourbage100% (1)

- Equity ValuationDocument42 pagesEquity ValuationSrinivas NuluNo ratings yet

- QFGDocument120 pagesQFGAlexander NadolinskiNo ratings yet

- Financial Risk Management (PROJECT)Document72 pagesFinancial Risk Management (PROJECT)Vinayak Halapeti100% (2)

- LandDocument2 pagesLandTasdi AsmaraNo ratings yet