You might also like

- Somatic TherapiesDocument170 pagesSomatic TherapiesDelyn Gamutan Millan100% (2)

- TAX3761 EXAM PACK JPJBLFDocument146 pagesTAX3761 EXAM PACK JPJBLFMonica Deetlefs0% (1)

- Procreate GuideDocument283 pagesProcreate GuideDiego D'Andrea100% (2)

- 50 Studies Every Anesthesiologist Shoud Know 2019Document305 pages50 Studies Every Anesthesiologist Shoud Know 2019pcut100% (2)

- 21 FAR460 SS SET 1 Dec21 Kel - StudentDocument9 pages21 FAR460 SS SET 1 Dec21 Kel - StudentRuzaikha razaliNo ratings yet

- FAR Problem Quiz 1 SolDocument3 pagesFAR Problem Quiz 1 SolEdnalyn CruzNo ratings yet

- Credo Auto SupplyDocument4 pagesCredo Auto SupplyShinji0% (1)

- Open World First B2 Students BookDocument257 pagesOpen World First B2 Students BookTuan Anh Bui88% (8)

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Document17 pagesMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoNo ratings yet

- 2018 - Exam 1 - Q1 - Sug SolDocument4 pages2018 - Exam 1 - Q1 - Sug SolmamitjasNo ratings yet

- Q7 Mguni LimitedDocument2 pagesQ7 Mguni Limitedamosmalusi5No ratings yet

- Chapter 5-Prob. 1Document7 pagesChapter 5-Prob. 1Rajah CalicaNo ratings yet

- Chapter 06 - AdjustmentsDocument26 pagesChapter 06 - AdjustmentsMkhonto Xulu100% (1)

- CFAS 16 and 18Document2 pagesCFAS 16 and 18Cath OquialdaNo ratings yet

- Pre-Final Exam in Audit 2-3Document5 pagesPre-Final Exam in Audit 2-3Shr BnNo ratings yet

- Acct6005 Company Accounting: Assessment 2 Case StudyDocument8 pagesAcct6005 Company Accounting: Assessment 2 Case StudyRuhan SinghNo ratings yet

- FAC 2602 - 2023 - S1 - Assessment 3 SolutionDocument9 pagesFAC 2602 - 2023 - S1 - Assessment 3 SolutionlennoxhaniNo ratings yet

- Mohammad Ilham Fawwaz - 11200820000107 - Akuntansi 2d - Aktiva TetapDocument7 pagesMohammad Ilham Fawwaz - 11200820000107 - Akuntansi 2d - Aktiva TetapMohammad Ilham FawwazNo ratings yet

- Afar JNDocument2 pagesAfar JNjasonnumahnalkelNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

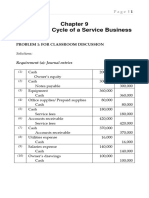

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDocument48 pagesSol. Man. - Chapter 9 - Acctg Cycle of A Service Businessrandomlungs121223No ratings yet

- Financial Planning and Control AssignmentDocument3 pagesFinancial Planning and Control AssignmentnkwatalindiweNo ratings yet

- DagohoyDocument6 pagesDagohoylinkin soyNo ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Ia Forcadela Part IIIDocument5 pagesIa Forcadela Part IIIMary Joanne forcadelaNo ratings yet

- Accounting Tutorial 2Document24 pagesAccounting Tutorial 2Fallen LeavesNo ratings yet

- Solution - Mock Exam - 240120 - 142640Document6 pagesSolution - Mock Exam - 240120 - 142640lebiyacNo ratings yet

- Accounting Worksheet 2 Answer SheetDocument31 pagesAccounting Worksheet 2 Answer Sheetzeldazitha87No ratings yet

- FAC1601-oct2013 Suggested SolutiionDocument9 pagesFAC1601-oct2013 Suggested SolutiionhlisoNo ratings yet

- Format IS and BSDocument2 pagesFormat IS and BSckyn greenleafNo ratings yet

- Group FinancialDocument8 pagesGroup FinancialNever GonondoNo ratings yet

- May 2018 Crammer's Guide Answers: Inventory To Be Removed From Inventory Because of Purchase Cutoff TestDocument14 pagesMay 2018 Crammer's Guide Answers: Inventory To Be Removed From Inventory Because of Purchase Cutoff TestJamieNo ratings yet

- Q5 Vikings LimitedDocument2 pagesQ5 Vikings Limitedamosmalusi5No ratings yet

- FAR Problem Quiz 2Document3 pagesFAR Problem Quiz 2Ednalyn CruzNo ratings yet

- Chapter 9 Accounting Cycle of A Service BusinessDocument59 pagesChapter 9 Accounting Cycle of A Service BusinessArlyn Ragudos BSA1No ratings yet

- Fa Pilot Paper AnswerDocument11 pagesFa Pilot Paper Answer刘宝英No ratings yet

- 2020 Sem 1 ACC10007 Discussion Questions (And Solutions) - Topic 2 (Part 3)Document5 pages2020 Sem 1 ACC10007 Discussion Questions (And Solutions) - Topic 2 (Part 3)Renee WongNo ratings yet

- ASS Accountingcycleofaservicebusiness FJPDocument59 pagesASS Accountingcycleofaservicebusiness FJPArlyn Ragudos BSA1No ratings yet

- FF - Karil Koiriyah - 180421621551 - Tugas 4Document92 pagesFF - Karil Koiriyah - 180421621551 - Tugas 4karinaNo ratings yet

- Ans June 2018 Far410Document8 pagesAns June 2018 Far4102022478048No ratings yet

- Cpa Review School of The Philippines.2Document6 pagesCpa Review School of The Philippines.2Snow TurnerNo ratings yet

- Gross Profit 25,450.00Document6 pagesGross Profit 25,450.00AliNo ratings yet

- ACC705 Corporate Accounting AssignmentDocument9 pagesACC705 Corporate Accounting AssignmentMuhammad AhsanNo ratings yet

- 2017 BGSS 4E5N Prelim P2 AnsDocument6 pages2017 BGSS 4E5N Prelim P2 AnsDamien SeowNo ratings yet

- Proforma StatmentsDocument4 pagesProforma StatmentsMehar AttaullahNo ratings yet

- 20solution Far460 - Jun 2020 - StudentDocument10 pages20solution Far460 - Jun 2020 - StudentRuzaikha razaliNo ratings yet

- Non-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model AnswersDocument8 pagesNon-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model Answersrwl s.r.lNo ratings yet

- FAC 3701 Exam PackDocument52 pagesFAC 3701 Exam Packartwell MagiyaNo ratings yet

- Financial Accounting N 6 Test MG 2nd Semester 2017Document8 pagesFinancial Accounting N 6 Test MG 2nd Semester 2017professional accountantsNo ratings yet

- Red Rose EnterpriseDocument3 pagesRed Rose Enterprisefatin batrisyiaNo ratings yet

- Start-Up Capital:: Particulars Taka TakaDocument5 pagesStart-Up Capital:: Particulars Taka TakaSahriar EmonNo ratings yet

- Answer Key Discussion of Sir Paul of PreweekDocument2 pagesAnswer Key Discussion of Sir Paul of PreweekElaine Joyce GarciaNo ratings yet

- Semi Final AccountingDocument8 pagesSemi Final AccountingSherryl DumagpiNo ratings yet

- Far1 Artt Ias 36 Test SolDocument2 pagesFar1 Artt Ias 36 Test SolHassan TanveerNo ratings yet

- AFA IIP.L III SolutionJune 2016Document4 pagesAFA IIP.L III SolutionJune 2016HossainNo ratings yet

- Adv Level Corporate Reporting (CR)Document24 pagesAdv Level Corporate Reporting (CR)FarhadNo ratings yet

- Memorandum Question 12 Mandlacoal LTD 2021Document8 pagesMemorandum Question 12 Mandlacoal LTD 2021NOKUHLE ARTHELNo ratings yet

- Group RepoprtingDocument3 pagesGroup RepoprtingPaulNo ratings yet

- Corporate Reporting - ND2020 - Suggested - Answers - Review by SBDocument13 pagesCorporate Reporting - ND2020 - Suggested - Answers - Review by SBTamanna KinnoreNo ratings yet

- FAF Tutorial 7 Deferred TaxationDocument2 pagesFAF Tutorial 7 Deferred Taxation嘉慧No ratings yet

- Unit-5 Final AccountsDocument7 pagesUnit-5 Final AccountsSanthosh Santhu0% (1)

- Key To Correction - Intermediate Accounting - Midterm - 2019-2020Document10 pagesKey To Correction - Intermediate Accounting - Midterm - 2019-2020Renalyn ParasNo ratings yet

- Cpa Review School of The Philippines Mani LaDocument6 pagesCpa Review School of The Philippines Mani LaSophia PerezNo ratings yet

- Group 10 - Stem 11 ST - DominicDocument34 pagesGroup 10 - Stem 11 ST - Dominicchristine ancheta100% (1)

- CMNS Week 3.2 Memo AssignmentDocument2 pagesCMNS Week 3.2 Memo AssignmentPulkit KalhanNo ratings yet

- Three Steps For Reducing Total Cost of Ownership in Pumping SystemsDocument13 pagesThree Steps For Reducing Total Cost of Ownership in Pumping SystemsJuan AriguelNo ratings yet

- Barotac Nuevo POP PDFDocument10 pagesBarotac Nuevo POP PDFJason Barrios PortadaNo ratings yet

- Laboratory Activity 1CDocument4 pagesLaboratory Activity 1CAini HasshimNo ratings yet

- Seven Elements of Effective NegotiationsDocument3 pagesSeven Elements of Effective NegotiationsKilik GantitNo ratings yet

- Fraction Selection BrochureDocument2 pagesFraction Selection Brochureapi-186663124No ratings yet

- Adding Rows Dynamically in A Table Using Interactive Adobe FormsDocument5 pagesAdding Rows Dynamically in A Table Using Interactive Adobe Formsbharath_sajjaNo ratings yet

- Sigma JsDocument42 pagesSigma JslakshmiescribdNo ratings yet

- Primax Solar Energy CatalogueDocument49 pagesPrimax Solar Energy CatalogueSalman Ali QureshiNo ratings yet

- Answer The Question According To The ListeningDocument10 pagesAnswer The Question According To The ListeningusuarioNo ratings yet

- Science Experiment Week 5 Lesson PlanDocument5 pagesScience Experiment Week 5 Lesson Planapi-451266317No ratings yet

- CRC Ace Far 1ST PBDocument9 pagesCRC Ace Far 1ST PBJohn Philip Castro100% (1)

- Model Teaching CompetenciesDocument12 pagesModel Teaching CompetenciesTeachers Without BordersNo ratings yet

- Swollen EyelidsDocument4 pagesSwollen EyelidsNARENDRANo ratings yet

- Effects of Brainstorming On Students' Achievement in Senior Secondary ChemistryDocument8 pagesEffects of Brainstorming On Students' Achievement in Senior Secondary ChemistryzerufasNo ratings yet

- Math 7 LAS W1&W2Document9 pagesMath 7 LAS W1&W2Friendsly TamsonNo ratings yet

- Rubricks For Case StudyDocument2 pagesRubricks For Case StudyMiguelito Aquino RuelanNo ratings yet

- Multiple Choice Questions: This Activity Contains 15 QuestionsDocument4 pagesMultiple Choice Questions: This Activity Contains 15 QuestionsRaman Kulkarni100% (1)

- Reading 40 Introduction To Industry and Company AnalysisDocument23 pagesReading 40 Introduction To Industry and Company AnalysisNeerajNo ratings yet

- M.S Engineering (Aerospace) Application Form: For Office UseDocument4 pagesM.S Engineering (Aerospace) Application Form: For Office Useshashasha123No ratings yet

- Indiga Indiga: Tech TechDocument32 pagesIndiga Indiga: Tech Techsunny100% (1)

- CH 7b - Shift InstructionsDocument20 pagesCH 7b - Shift Instructionsapi-237335979100% (1)

- 02 RgebDocument1,168 pages02 Rgebprožnik100% (3)

- CH 121: Organic Chemistry IDocument13 pagesCH 121: Organic Chemistry IJohn HeriniNo ratings yet

- Name - ESM 2104 Sample Final ExamDocument7 pagesName - ESM 2104 Sample Final ExamCOCO12432345No ratings yet