You might also like

- 07.paypalDocument9 pages07.paypalNishadi LakshithaNo ratings yet

- BRAC Bank Statement 10052023 PDFDocument7 pagesBRAC Bank Statement 10052023 PDFMd Mizanur Rahman100% (1)

- Pru HI 6th Edition (4 Sets of Mock Combined)Document51 pagesPru HI 6th Edition (4 Sets of Mock Combined)thth943No ratings yet

- March-2022 Marcellus - Little-Champs - Presentation - DIRECTDocument19 pagesMarch-2022 Marcellus - Little-Champs - Presentation - DIRECTAGNo ratings yet

- Marcellus Little-Champs Presentation DIRECTDocument19 pagesMarcellus Little-Champs Presentation DIRECTBijoy RaghavanNo ratings yet

- Marcellus LittleChamps PresentationDocument15 pagesMarcellus LittleChamps PresentationPawan ShroffNo ratings yet

- Marcellus Little-Champs PresentationDocument18 pagesMarcellus Little-Champs PresentationSuyash BhiseNo ratings yet

- Little Champs PMS: An Investment Strategy For Indian Small Caps From Marcellus Investment ManagersDocument18 pagesLittle Champs PMS: An Investment Strategy For Indian Small Caps From Marcellus Investment Managerssubham mohantyNo ratings yet

- Marcellus Little-Champs PresentationDocument17 pagesMarcellus Little-Champs PresentationqwertyNo ratings yet

- Ambit Good & Clean Smallcap Fund (Emerging Giants) : Portfolio Management ServicesDocument26 pagesAmbit Good & Clean Smallcap Fund (Emerging Giants) : Portfolio Management ServicesSaurabh MukherjeeNo ratings yet

- Marcellus RisingGiants PMS DirectDocument23 pagesMarcellus RisingGiants PMS Directajay huddaNo ratings yet

- Marcellus Rising Giants PMS July-2023 Direct Final-1Document23 pagesMarcellus Rising Giants PMS July-2023 Direct Final-1Vaman ShenoyNo ratings yet

- Marcellus Rising Giants PMS June-2023 Direct Final CompressedDocument23 pagesMarcellus Rising Giants PMS June-2023 Direct Final Compressed123bingoNo ratings yet

- US Stock Bond CorrelationDocument24 pagesUS Stock Bond CorrelationSabyasachi MukherjeeNo ratings yet

- A Pair That Can Take You To Your Goal!: HDFC Large and Mid Cap FundDocument21 pagesA Pair That Can Take You To Your Goal!: HDFC Large and Mid Cap FundflplopaNo ratings yet

- Navin Agarwal Article Sep 2021Document5 pagesNavin Agarwal Article Sep 2021Smeet GopaniNo ratings yet

- Marcellus RisingGiants PMS Direct 230223 061127Document24 pagesMarcellus RisingGiants PMS Direct 230223 061127IndeevarBhattNo ratings yet

- Arcelik Beko LLC 20120314 PDFDocument100 pagesArcelik Beko LLC 20120314 PDFJane SavinaNo ratings yet

- Britannia Investment Presentation - RKDocument22 pagesBritannia Investment Presentation - RKRohit KadamNo ratings yet

- Presentation-IDFC Emerging Businesses Fund PDFDocument29 pagesPresentation-IDFC Emerging Businesses Fund PDFani dNo ratings yet

- Bridgewater ReportDocument12 pagesBridgewater Reportw_fibNo ratings yet

- 4Q 2020 Slides VFDocument56 pages4Q 2020 Slides VFAbdul HadiNo ratings yet

- 68 32 Presentasi Perusahaan Fy 2020 Indicative ResultsDocument47 pages68 32 Presentasi Perusahaan Fy 2020 Indicative ResultsIvanNo ratings yet

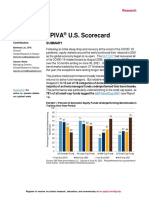

- Spiva Us Mid Year 2021Document36 pagesSpiva Us Mid Year 2021Gábor ZsédelyNo ratings yet

- Summer Internship ProjectDocument31 pagesSummer Internship ProjectAayush PasawalaNo ratings yet

- KPI Green EnergyDocument34 pagesKPI Green EnergyRJNo ratings yet

- Chapter 2Document14 pagesChapter 2Marcus HowardNo ratings yet

- NJTC X Alliance BernsteinDocument62 pagesNJTC X Alliance BernsteinAna MazumdarNo ratings yet

- Quarter 2 Market Report: The Big PictureDocument9 pagesQuarter 2 Market Report: The Big PictureMridul SharmaNo ratings yet

- India Listed Pharma Healthcare May23Document6 pagesIndia Listed Pharma Healthcare May23Vansh AggarwalNo ratings yet

- 2023 December Nick Atkeson How To Make Money in A World Where Fin Analyst Are WrongDocument60 pages2023 December Nick Atkeson How To Make Money in A World Where Fin Analyst Are WrongBob ReeceNo ratings yet

- MER - Jan - 2022 - 15 Feb - FinalDocument30 pagesMER - Jan - 2022 - 15 Feb - FinalShemeem SNo ratings yet

- November 2023 ICEA LION Income Fund Fact SheetDocument1 pageNovember 2023 ICEA LION Income Fund Fact SheetAndrew MuhumuzaNo ratings yet

- ICICI Pru Large & Mid Cap FundDocument10 pagesICICI Pru Large & Mid Cap FundRang NarayanNo ratings yet

- CH 04-05-06 Performance AnalysisDocument26 pagesCH 04-05-06 Performance Analysis2021-108960No ratings yet

- Sip Presentation - May 2020Document40 pagesSip Presentation - May 2020DBCGNo ratings yet

- AMBITGOOD&CLEAN - Midcap PMS - Jan - 2022 - PresentationDocument24 pagesAMBITGOOD&CLEAN - Midcap PMS - Jan - 2022 - Presentationbeza manojNo ratings yet

- Yield Curve Control What It Is Who Is Doing It and What It MeansDocument7 pagesYield Curve Control What It Is Who Is Doing It and What It MeansJay ZNo ratings yet

- Arup Raha - Indonesia in A Covid-19 WorldDocument10 pagesArup Raha - Indonesia in A Covid-19 WorldMikesNo ratings yet

- Infographics For The Annual Report 2018-2019Document1 pageInfographics For The Annual Report 2018-2019Violeta IlieNo ratings yet

- Personal Financial Planning: End-Term ProjectDocument12 pagesPersonal Financial Planning: End-Term ProjectPoloJ20No ratings yet

- Goldman - MA Perspectives PDFDocument9 pagesGoldman - MA Perspectives PDFPedro CastilloNo ratings yet

- Galleon - September 2009 ExposureDocument14 pagesGalleon - September 2009 Exposuremarketfolly.comNo ratings yet

- STRATEGY Nifty - Bank IT 20230327 MOSL SU PG010Document10 pagesSTRATEGY Nifty - Bank IT 20230327 MOSL SU PG010Aakash ChhariaNo ratings yet

- The Good, The Bad and The Ugly On Tech Valuations, AI, Energy and US PoliticsDocument11 pagesThe Good, The Bad and The Ugly On Tech Valuations, AI, Energy and US Politicsmuratc.cansoyNo ratings yet

- India Insurance - Bracing For A Lower Growth Environment 08jun23 - MacquarieDocument9 pagesIndia Insurance - Bracing For A Lower Growth Environment 08jun23 - MacquarieSharath JuturNo ratings yet

- Invest in Mid Cap Fund - UTI Equity Mutual FundsDocument2 pagesInvest in Mid Cap Fund - UTI Equity Mutual FundsRinku MishraNo ratings yet

- Bangladesh Economic Growth FDIs - Lightcastle Partners PresentationDocument10 pagesBangladesh Economic Growth FDIs - Lightcastle Partners PresentationMizanur RahmanNo ratings yet

- Latam Investment Banking Review q1 2021Document18 pagesLatam Investment Banking Review q1 2021Fernando Cano WongNo ratings yet

- Tracking Performance of Small Finance Banks Against Financial Inclusion GoalsDocument30 pagesTracking Performance of Small Finance Banks Against Financial Inclusion GoalsNeelanjan MaitiNo ratings yet

- The Broader View Is Brighter When You Pull Back The LensDocument3 pagesThe Broader View Is Brighter When You Pull Back The LensKOMATSU SHOVELNo ratings yet

- Market Complacency: The Risk of InactionDocument6 pagesMarket Complacency: The Risk of InactionThinh DoNo ratings yet

- Wipes in Brazil DatagraphicsDocument4 pagesWipes in Brazil DatagraphicsbabiNo ratings yet

- Industry Analysis - Property - 020919Document4 pagesIndustry Analysis - Property - 020919aly_rowiNo ratings yet

- Bridgewater - Stock-Market-Bubble - Feb21Document8 pagesBridgewater - Stock-Market-Bubble - Feb21KDEWolfNo ratings yet

- CRISIL Fund Insights Mar2020Document4 pagesCRISIL Fund Insights Mar2020Rahul SharmaNo ratings yet

- City Bank Limited, The: Update To Credit AnalysisDocument10 pagesCity Bank Limited, The: Update To Credit AnalysisJannatun NayeemaNo ratings yet

- Why and How Capitalism Needs To Be ReformedDocument21 pagesWhy and How Capitalism Needs To Be ReformedJay ZNo ratings yet

- MMYT Investor Presentation - Q4 FinalDocument27 pagesMMYT Investor Presentation - Q4 FinalvinitNo ratings yet

- Internships PGDM 2020 22 BatchDocument6 pagesInternships PGDM 2020 22 BatchSanthosh SanthuNo ratings yet

- Pessimism Overdone: Perspective On IT SectorDocument6 pagesPessimism Overdone: Perspective On IT Sectorsarvo_44No ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- IPS AIO - DSI - MWPA - 100Rs Per Day - 15LCIDocument2 pagesIPS AIO - DSI - MWPA - 100Rs Per Day - 15LCIvikas pallaNo ratings yet

- Dunlapslk PresentationDocument18 pagesDunlapslk Presentationapi-325349652No ratings yet

- Mxbar - PL - Oper: Auto Invoice Execution and Validation ReportDocument4 pagesMxbar - PL - Oper: Auto Invoice Execution and Validation ReportAntonio Arroyo SolanoNo ratings yet

- Respon Code Edc Miniatm-1Document1 pageRespon Code Edc Miniatm-1hasibuanNo ratings yet

- In-Depth Analysis of The Insolvency and Bankruptcy Code, 2016 and The Frdi Bill, 2017Document276 pagesIn-Depth Analysis of The Insolvency and Bankruptcy Code, 2016 and The Frdi Bill, 2017Venkat Deepak SarmaNo ratings yet

- Debit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedDocument1 pageDebit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedRajesh KumarNo ratings yet

- Susquehanna Equipment Rentals (Group D) - PresentationDocument13 pagesSusquehanna Equipment Rentals (Group D) - PresentationNoman ANo ratings yet

- IFRS 3 - Business Combinations: HISTORY OF IFRS 3 (Last Page)Document8 pagesIFRS 3 - Business Combinations: HISTORY OF IFRS 3 (Last Page)Mila MercadoNo ratings yet

- Challan PDFDocument1 pageChallan PDFShilesh GargNo ratings yet

- Abid Hussain: Career ObjectiveDocument2 pagesAbid Hussain: Career ObjectiveAbid HussainNo ratings yet

- Aptitude Software IFRS 17 Solution Factsheet June 2021Document4 pagesAptitude Software IFRS 17 Solution Factsheet June 2021BenjaminNo ratings yet

- Credit CardsDocument8 pagesCredit Cardsasmat ullah khanNo ratings yet

- Sorin Capital Management - Quality Rating ReportDocument6 pagesSorin Capital Management - Quality Rating ReportSorin Capital Jim HigginsNo ratings yet

- Pro Forma StatementDocument14 pagesPro Forma StatementEse Peace100% (1)

- Republic vs. First National City Bank of New YorkDocument7 pagesRepublic vs. First National City Bank of New YorkFD BalitaNo ratings yet

- Credit Union in The PhilippinesDocument4 pagesCredit Union in The PhilippinesJoyce-An Nicole MercadoNo ratings yet

- Valenzuela - Workshop 4Document3 pagesValenzuela - Workshop 4Weiyee ValenzuelaNo ratings yet

- Shahzad Yaqoob Bop Internship ReportDocument51 pagesShahzad Yaqoob Bop Internship ReportShahzad YaqoobNo ratings yet

- Materi Penilaian obligasi-LDLDocument23 pagesMateri Penilaian obligasi-LDLGustianNo ratings yet

- GPF Part Final Appendix oDocument3 pagesGPF Part Final Appendix oteja ptoNo ratings yet

- No Akun Nama Akun N Type AkunDocument5 pagesNo Akun Nama Akun N Type AkunDanishNo ratings yet

- 1178-Addendum-Change in Sponsor - HDFC LTD To HDFC Bank - July 1, 2023Document3 pages1178-Addendum-Change in Sponsor - HDFC LTD To HDFC Bank - July 1, 2023Jai Shree Ambe EnterprisesNo ratings yet

- Fa@emba 2023Document5 pagesFa@emba 2023satyam pandeyNo ratings yet

- BNL StoresDocument4 pagesBNL Storesshanul gawshindeNo ratings yet

- Tentative Rates of Return On PLSDeposits OtherDepositsDocument1 pageTentative Rates of Return On PLSDeposits OtherDepositsAliNo ratings yet

- Commerce and Accountancy Mcqs - 4Document4 pagesCommerce and Accountancy Mcqs - 4Gaurav Chandra DasNo ratings yet

- Session 3 - ACLO - Lecture PDFDocument9 pagesSession 3 - ACLO - Lecture PDFQamber AliNo ratings yet