You might also like

- Ch01 - Introduction - To - EconomicsDocument47 pagesCh01 - Introduction - To - EconomicsTanveer AhmedNo ratings yet

- Chapter 01 IntroductionDocument33 pagesChapter 01 IntroductionTanha RupontiNo ratings yet

- Applied Economics MIDTERM REVIEWERDocument13 pagesApplied Economics MIDTERM REVIEWERKate JavierNo ratings yet

- 1.0 Definition, Nature and Scope of EconomicsDocument40 pages1.0 Definition, Nature and Scope of EconomicsahsakahNo ratings yet

- 0. IntroductionDocument15 pages0. Introductiondev.m.dodiyaNo ratings yet

- Economics 001Document35 pagesEconomics 001Win Lwin OoNo ratings yet

- Lecture 1.ADocument21 pagesLecture 1.Aabdul basitNo ratings yet

- Micro1 Introduction & PrinciplesDocument46 pagesMicro1 Introduction & Principleskshubhanshu02No ratings yet

- Week 1 - MACRODocument34 pagesWeek 1 - MACROJohn Robert ReyesNo ratings yet

- Lecture 1 Introduction To MicroeconomicsDocument18 pagesLecture 1 Introduction To Microeconomicszhanghongrui0723No ratings yet

- Ten Principles of Economics (EDIT)Document33 pagesTen Principles of Economics (EDIT)WALEED HAIDERNo ratings yet

- Module 1: Concepts: Chapters 1, 2, 7, 8 & 11:216-222Document185 pagesModule 1: Concepts: Chapters 1, 2, 7, 8 & 11:216-222Bao AnhNo ratings yet

- Introduction To EconomicsDocument14 pagesIntroduction To EconomicsKemalNo ratings yet

- Lecture 1Document24 pagesLecture 1hassanNo ratings yet

- #Bba Microeconomics 10 PrinciplesDocument31 pages#Bba Microeconomics 10 PrinciplesMadiha Umer UqailiNo ratings yet

- Ten Principles of EconomicsDocument29 pagesTen Principles of EconomicschanpeinNo ratings yet

- Topic 1: Basic Ideas in EconomicsDocument15 pagesTopic 1: Basic Ideas in EconomicsMomina AbbasiNo ratings yet

- In This Chapter, Look For The Answers To These QuestionsDocument34 pagesIn This Chapter, Look For The Answers To These QuestionsChuck UyNo ratings yet

- Chapter 1: Ten Principles of Microeconomics: Economy Households and EconomiesDocument3 pagesChapter 1: Ten Principles of Microeconomics: Economy Households and EconomiesManel KricheneNo ratings yet

- Chapter 1 - Ten Principles of EconomicsDocument22 pagesChapter 1 - Ten Principles of EconomicsLe Trinh Anh (K17 HCM)No ratings yet

- UTS Ekonomi 3 CombinepptDocument10 pagesUTS Ekonomi 3 Combineppttriaa.wulandNo ratings yet

- Principles Of: EconomicsDocument45 pagesPrinciples Of: EconomicsKiều TrangNo ratings yet

- Principles of Economics,: Powerpoint® Lecture PresentationDocument30 pagesPrinciples of Economics,: Powerpoint® Lecture PresentationuniqueMyomNo ratings yet

- Ten Principles of EconomicsDocument21 pagesTen Principles of EconomicsYvonne Llaban RangabanNo ratings yet

- Understanding the Economic EnvironmentDocument46 pagesUnderstanding the Economic EnvironmentMuhammad Munir AhmadNo ratings yet

- Ten Principles of EconomicsDocument21 pagesTen Principles of EconomicsThành PhạmNo ratings yet

- 10 Principles of EconomicsDocument18 pages10 Principles of EconomicsanujjalansNo ratings yet

- Eco 111 Notes-1Document42 pagesEco 111 Notes-1Hazel KeitshokileNo ratings yet

- Principles of EconomicsDocument21 pagesPrinciples of EconomicsJEAN KANTY A. ALVAREZNo ratings yet

- Principles of EconomicsDocument19 pagesPrinciples of EconomicsvihaanNo ratings yet

- Ssed 11 Module 1 Lesson 1Document11 pagesSsed 11 Module 1 Lesson 1Shiela IgnacioNo ratings yet

- CCS 009 Lec 1,2,3&4 CombinedDocument89 pagesCCS 009 Lec 1,2,3&4 CombinedAustin RelishNo ratings yet

- 10 Principles of Economics ExplainedDocument26 pages10 Principles of Economics ExplainedPriya Srinivasan100% (1)

- Chapter 1: Introduction To Economics: Intended Learning OutcomesDocument9 pagesChapter 1: Introduction To Economics: Intended Learning OutcomesSanuNo ratings yet

- PRINCIPLES OF MICROECONOMICS (ECON104Document66 pagesPRINCIPLES OF MICROECONOMICS (ECON104Peace PanasheNo ratings yet

- Class 1 - Principles of Economics (1introduction)Document34 pagesClass 1 - Principles of Economics (1introduction)Sourav Halder100% (8)

- Week 1 Introduction To MicroeconomicsDocument39 pagesWeek 1 Introduction To Microeconomicstissot63No ratings yet

- Lec 1 Principles EconomicsDocument57 pagesLec 1 Principles Economicshesbon akoraNo ratings yet

- Managerial Economics: Chapter One Introducing EconomicsDocument24 pagesManagerial Economics: Chapter One Introducing EconomicsRadoNo ratings yet

- CH1 - INTRODUCTION - IobmDocument34 pagesCH1 - INTRODUCTION - IobmAli AbdullahNo ratings yet

- Chapter 1 Introduction To Economics BMDocument42 pagesChapter 1 Introduction To Economics BMSKYRunner 777No ratings yet

- Ch. 1 Ten Principle of Economics MacroecoDocument31 pagesCh. 1 Ten Principle of Economics MacroecoNazeNo ratings yet

- Principles of Economics Slides 2024 - Upto ElasticityDocument127 pagesPrinciples of Economics Slides 2024 - Upto ElasticityIsaac AmankwahNo ratings yet

- CH 01Document5 pagesCH 01nisarg_No ratings yet

- Microi_mankiw Ch1 (1)Document35 pagesMicroi_mankiw Ch1 (1)Tania RodríguezNo ratings yet

- Microeconomics Exam NotesDocument11 pagesMicroeconomics Exam NotesRobin SminesNo ratings yet

- Intro to Economics PrinciplesDocument22 pagesIntro to Economics PrinciplesNuman EratNo ratings yet

- Economics Oct 30 - MergedDocument56 pagesEconomics Oct 30 - MergedRamiz Ul HasanNo ratings yet

- 10 Principles of Economics ExplainedDocument976 pages10 Principles of Economics Explainedavg_rao06No ratings yet

- Ten Principles of Economics: ConomicsDocument35 pagesTen Principles of Economics: Conomicshpl4jcNo ratings yet

- Introduction to Economics Key ConceptsDocument11 pagesIntroduction to Economics Key ConceptsJL ManabaNo ratings yet

- CH 1 Ten Principles of EconomicsDocument31 pagesCH 1 Ten Principles of EconomicsAndriiNo ratings yet

- Introduction To Economics:: Definition of Economic, Understanding Scarcity, Microeconomics IssueDocument25 pagesIntroduction To Economics:: Definition of Economic, Understanding Scarcity, Microeconomics IssueArvind GiritharagopalanNo ratings yet

- Economics For Managers - Notes-3Document23 pagesEconomics For Managers - Notes-3Phillip Gordon MulesNo ratings yet

- Fdnecon Module1-2 ReviewerDocument4 pagesFdnecon Module1-2 ReviewerscarNo ratings yet

- Ten Principles of Economics: ConomicsDocument34 pagesTen Principles of Economics: ConomicsNathtalyNo ratings yet

- Ten Principles of Economics: ConomicsDocument29 pagesTen Principles of Economics: ConomicsMazen AymanNo ratings yet

- Abu Naser Mohammad Saif: Assistant ProfessorDocument29 pagesAbu Naser Mohammad Saif: Assistant ProfessorSH RaihanNo ratings yet

- AP Microeconomics Class Notes - Chapter 1 - Ten Principles of EconomicsDocument5 pagesAP Microeconomics Class Notes - Chapter 1 - Ten Principles of EconomicshiralltaylorNo ratings yet

- Ap 2Document8 pagesAp 2Louiejane LapinigNo ratings yet

- Chapter-1 Introduction To EconomicsDocument114 pagesChapter-1 Introduction To Economicshailu tasheNo ratings yet

- Understanding the Invisible Hand and How Markets WorkDocument23 pagesUnderstanding the Invisible Hand and How Markets WorkEthelyn Cailly R. ChenNo ratings yet

- English 8 Q3 Module 3Document31 pagesEnglish 8 Q3 Module 3ringoNo ratings yet

- Q1 - M2 Applied EconDocument9 pagesQ1 - M2 Applied EconMegan Lou CamiguinNo ratings yet

- Handbook On Opensea Cage CultureDocument154 pagesHandbook On Opensea Cage CultureVijayagopal PanikkerNo ratings yet

- Foundation of Economics PDFDocument6 pagesFoundation of Economics PDFgabytjintjelaarNo ratings yet

- Understanding Economics Through Scarcity and ChoiceDocument8 pagesUnderstanding Economics Through Scarcity and ChoiceladduNo ratings yet

- Lecture 1 - Scarcity and ChoiceDocument15 pagesLecture 1 - Scarcity and ChoicetagashiiNo ratings yet

- Applied Economics-Chapter 1Document27 pagesApplied Economics-Chapter 1Becky GalanoNo ratings yet

- Grade 11 Economics TextbookDocument369 pagesGrade 11 Economics Textbookdagnachew mezgebuNo ratings yet

- Basic Economics Concepts: Value, Utility, Scarcity and Classification of Human WantsDocument4 pagesBasic Economics Concepts: Value, Utility, Scarcity and Classification of Human WantsSourav bhattacharyyaNo ratings yet

- Eco 113 Unit 1Document66 pagesEco 113 Unit 1shahigyanendra146No ratings yet

- AP Economics - Summer Assignment 2023-2024Document6 pagesAP Economics - Summer Assignment 2023-2024Sara SalemNo ratings yet

- The Big ResetDocument25 pagesThe Big ResetAgencia Nova MidiaNo ratings yet

- Economics Teacher Notes PDFDocument113 pagesEconomics Teacher Notes PDFmalik naeemNo ratings yet

- EC1101E: Introduction To Economic AnalysisDocument79 pagesEC1101E: Introduction To Economic AnalysisdineshNo ratings yet

- Microeconomic Theory and Practice: San Beda University AY 21-22Document63 pagesMicroeconomic Theory and Practice: San Beda University AY 21-22Sergio ConjugalNo ratings yet

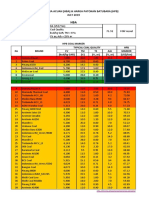

- Harga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) JULY 2019Document8 pagesHarga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) JULY 2019Adnan NstNo ratings yet

- Law On Supply and Demand ExamDocument6 pagesLaw On Supply and Demand ExamSharah Del T. TudeNo ratings yet

- SST 212 Microeconomics SIM Unit 1Document24 pagesSST 212 Microeconomics SIM Unit 1France FuertesNo ratings yet

- Basic Microeconomics Eco101Document59 pagesBasic Microeconomics Eco101Kirk Angelu Victoria AdovasNo ratings yet

- Microeconomics: Dr. Ahmed Said AhmedDocument18 pagesMicroeconomics: Dr. Ahmed Said Ahmedmariam raafatNo ratings yet

- Tutorial - Chapter 1 - Introduction - Questions 1Document4 pagesTutorial - Chapter 1 - Introduction - Questions 1NandiieNo ratings yet

- Basic Concept of EconomicsDocument7 pagesBasic Concept of EconomicsAshish DhakalNo ratings yet

- FEDERAL BUDGET AND SCARCITYDocument39 pagesFEDERAL BUDGET AND SCARCITYJoelyn RamosNo ratings yet

- Managerial Economics Activity 01Document2 pagesManagerial Economics Activity 01Anthony John BrionesNo ratings yet

- Understanding Business Activity: Contents-Section 1Document53 pagesUnderstanding Business Activity: Contents-Section 1Allan IshimweNo ratings yet

- Lecture Notes 1 Course Overview and IntroductionDocument62 pagesLecture Notes 1 Course Overview and IntroductionChloe TewNo ratings yet

- Lesson PlansDocument5 pagesLesson Plansapi-313507031No ratings yet