You might also like

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 pagesCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsNo ratings yet

- Composition SchemeDocument4 pagesComposition Schemecloudstorage567No ratings yet

- Composition Levy: Presentation By: Vishal Somai Sr. Faculty of Direct & Indirect TaxDocument19 pagesComposition Levy: Presentation By: Vishal Somai Sr. Faculty of Direct & Indirect TaxTRANSFORMERS PRIMENo ratings yet

- TRAINING. NOTES Commercial TaxDocument116 pagesTRAINING. NOTES Commercial TaxVipin Thomas100% (1)

- Taxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTDocument5 pagesTaxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTTheEnigmatic AccountantNo ratings yet

- CGST Act SummaryDocument371 pagesCGST Act SummaryRohan KulkarniNo ratings yet

- IGST (Integrated GST) : Based On The IGST Act, 2017 and The CGST Act, 2017Document85 pagesIGST (Integrated GST) : Based On The IGST Act, 2017 and The CGST Act, 2017Partha BhaskarNo ratings yet

- Goods and Service Tax NoDocument5 pagesGoods and Service Tax NonitinNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Customs TMP 1Document28 pagesCustoms TMP 1ankit1007No ratings yet

- Types of Duty PDFDocument27 pagesTypes of Duty PDFfirastiNo ratings yet

- Levy & Collection CGST (11-2)Document11 pagesLevy & Collection CGST (11-2)kapuNo ratings yet

- GST Registration NotesDocument13 pagesGST Registration NotesNagashree RANo ratings yet

- Composition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Document12 pagesComposition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Tapan BarikNo ratings yet

- Chapter 8 Composition Scheme Under GSTDocument12 pagesChapter 8 Composition Scheme Under GSTDR. PREETI JINDALNo ratings yet

- GST Payment of Tax ProvisionsDocument36 pagesGST Payment of Tax ProvisionsKush BafnaNo ratings yet

- GST Unit 3 (2021)Document43 pagesGST Unit 3 (2021)Anwesha HotaNo ratings yet

- Payments To Non-ResidentsDocument8 pagesPayments To Non-Residentssmyns.bwNo ratings yet

- Health CareDocument83 pagesHealth CareKumar KNo ratings yet

- Payment of Tax: (SECTION 49 To 53A)Document36 pagesPayment of Tax: (SECTION 49 To 53A)Mehak KaushikkNo ratings yet

- Ca Suraj Satija Ssguru Charge of GSTDocument12 pagesCa Suraj Satija Ssguru Charge of GSTSunny YadavNo ratings yet

- ExportDocument25 pagesExportBala VinayagamNo ratings yet

- Misc Sections For Exams March 2022Document11 pagesMisc Sections For Exams March 2022Daniyal AhmedNo ratings yet

- Section___23__Central_Goods_And_Services_Tax_Act__2017_Persons_not_liable_for_registrationDocument2 pagesSection___23__Central_Goods_And_Services_Tax_Act__2017_Persons_not_liable_for_registrationbhaviknagoriNo ratings yet

- Tax Updates For June 2012 ExamsDocument37 pagesTax Updates For June 2012 ExamsShanky MalhotraNo ratings yet

- CGST Act 16-21Document37 pagesCGST Act 16-21Dasari NareshNo ratings yet

- Finance Act 2022Document147 pagesFinance Act 2022vikaskumar1No ratings yet

- Indirect Tax AmendmentsDocument46 pagesIndirect Tax AmendmentsCeciro LodhamNo ratings yet

- Finance Act 2023Document105 pagesFinance Act 2023sgacrewariNo ratings yet

- Amendment DirectTax FA2013Document30 pagesAmendment DirectTax FA2013Bharat LuthraNo ratings yet

- Tax HDocument15 pagesTax HDeepesh SinghNo ratings yet

- Tax Laws Updates For December 2013Document72 pagesTax Laws Updates For December 2013Archana ThirunagariNo ratings yet

- Goods and Services Tax - An Overview: Central Board of Excise & CustomsDocument10 pagesGoods and Services Tax - An Overview: Central Board of Excise & CustomsvsaraNo ratings yet

- LEVY AND COLLECTION OF GST - AbhiDocument14 pagesLEVY AND COLLECTION OF GST - AbhiAbhishek Abhi100% (1)

- Exemption From Customs DutyDocument4 pagesExemption From Customs DutyRavikumar PaNo ratings yet

- The New Income Tax Chapter 13: COLLECTION of Tax: PrintDocument4 pagesThe New Income Tax Chapter 13: COLLECTION of Tax: PrintzeeshanshahbazNo ratings yet

- GST Impact on Real Estate SectorDocument4 pagesGST Impact on Real Estate SectorjvnraoNo ratings yet

- Composition of LevyDocument6 pagesComposition of LevyYalini MeenakshiNo ratings yet

- GST TDS Provisions Under Section 51Document3 pagesGST TDS Provisions Under Section 51acm001No ratings yet

- Classification & Types of Customs DutiesDocument31 pagesClassification & Types of Customs Dutieskg704939No ratings yet

- Faq Composition Levy RevisedDocument8 pagesFaq Composition Levy Revisedbharigopan8360No ratings yet

- Excise DutyDocument4 pagesExcise DutyDigvijay LakdeNo ratings yet

- All About GST Annual ReturnsDocument9 pagesAll About GST Annual ReturnsinfoNo ratings yet

- Individual Paper Income Tax Return 2015Document23 pagesIndividual Paper Income Tax Return 2015marrukhjNo ratings yet

- Compendium of Law&Regulations For-MailDocument281 pagesCompendium of Law&Regulations For-MailAmbuj SakiNo ratings yet

- Overview of Key Amendments to the Philippine Tax Code under the TRAIN LawDocument28 pagesOverview of Key Amendments to the Philippine Tax Code under the TRAIN LawScarlette CooperaNo ratings yet

- Registration Under GSTDocument8 pagesRegistration Under GSTMahesh PawarNo ratings yet

- INCOME TAX AND CUSTOMS DUTY LAWDocument8 pagesINCOME TAX AND CUSTOMS DUTY LAWadil_lodhiNo ratings yet

- Chapter12 - VII - PDF Zero Rated SupplyDocument3 pagesChapter12 - VII - PDF Zero Rated Supplyravi.pansuriya07No ratings yet

- FBR IncomeTax Return 2016Document40 pagesFBR IncomeTax Return 2016Muhammad Awais100% (1)

- Changes in GSTDocument4 pagesChanges in GSTRanjodh KaurNo ratings yet

- Tax Laws Ns Ep June 2020Document29 pagesTax Laws Ns Ep June 2020sarvaniNo ratings yet

- GST Council 43rd Meeting Key RecommendationsDocument6 pagesGST Council 43rd Meeting Key Recommendationssuhani singhNo ratings yet

- Types of GSTDocument4 pagesTypes of GSTRuhul AminNo ratings yet

- GST Refunds and Composition SchemeDocument6 pagesGST Refunds and Composition SchemeKenny PhilipsNo ratings yet

- Topic:: Law of TaxationDocument8 pagesTopic:: Law of TaxationNeelam KejriwalNo ratings yet

- CGST LawDocument30 pagesCGST LawPranit Anil ChavanNo ratings yet

- Schedule of Rates (SOR) Tender No. Agl/231/Steel Valves/04-17Document1 pageSchedule of Rates (SOR) Tender No. Agl/231/Steel Valves/04-17Tejash NayakNo ratings yet

- Basic SolDocument3 pagesBasic SolADARSH MISHRANo ratings yet

- California Real Estate Principles, 10e - PowerPoint - CH 14Document23 pagesCalifornia Real Estate Principles, 10e - PowerPoint - CH 14tommy58No ratings yet

- Tax Return 2019Document26 pagesTax Return 2019Cash AppNo ratings yet

- Device InvoiceDocument5 pagesDevice InvoiceMohamed ZakiNo ratings yet

- SolutionDocument4 pagesSolutionFareha RiazNo ratings yet

- Salary Slip PDFDocument3 pagesSalary Slip PDFmohd aslamNo ratings yet

- Brian Bengs Pre PrimaryDocument48 pagesBrian Bengs Pre PrimaryPat PowersNo ratings yet

- MP1 - Machine Problem 1: Program 1Document7 pagesMP1 - Machine Problem 1: Program 1Mico VillanuevaNo ratings yet

- DonationS UNDE INCOME TAX ACTDocument2 pagesDonationS UNDE INCOME TAX ACTManjeet KaurNo ratings yet

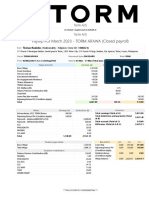

- Payslip For March 2023 - TORM ARAWA (Closed Payroll) : Torm A/S Torm A/SDocument1 pagePayslip For March 2023 - TORM ARAWA (Closed Payroll) : Torm A/S Torm A/SRodelio TomasNo ratings yet

- 03 BAINCTAX - Individual de Minimis and FringeDocument15 pages03 BAINCTAX - Individual de Minimis and FringeCarmela PeducheNo ratings yet

- Chapter 11 TaxDocument11 pagesChapter 11 Taxkp_popinjNo ratings yet

- Sebastian Desmond PO BOX 1717 West Sacramento Ca 95691 Sebastian Desmond PO BOX 1717 West Sacramento Ca 95691Document2 pagesSebastian Desmond PO BOX 1717 West Sacramento Ca 95691 Sebastian Desmond PO BOX 1717 West Sacramento Ca 95691Deborah Beth DarlingNo ratings yet

- Name: Santiago II, Cipriano Jeffrey F.: Homework 2 - Tax 1101 - Topic Income Tax - Corporation Part 2Document3 pagesName: Santiago II, Cipriano Jeffrey F.: Homework 2 - Tax 1101 - Topic Income Tax - Corporation Part 2うん こ100% (1)

- Federal Registery For 1040 and W-2 ScanDocument3 pagesFederal Registery For 1040 and W-2 ScanPhilNo ratings yet

- Cir v. Central Luzon Drug CorpDocument2 pagesCir v. Central Luzon Drug CorpLadyfirst SMNo ratings yet

- Hari Chand - October 2019 PDFDocument1 pageHari Chand - October 2019 PDFVasu GuptaNo ratings yet

- Javier vs. Commissioner Ancheta: CTA CASE NO 3393 JULY 27, 1983 Rean GonzalesDocument7 pagesJavier vs. Commissioner Ancheta: CTA CASE NO 3393 JULY 27, 1983 Rean GonzalesRean Raphaelle GonzalesNo ratings yet

- Preliminary Assessment NoticeDocument3 pagesPreliminary Assessment NoticeHanabishi RekkaNo ratings yet

- Total Invoice - State Code-09 State Code-09: - Pan No. ADIPY2538ADocument1 pageTotal Invoice - State Code-09 State Code-09: - Pan No. ADIPY2538Aramroshan712No ratings yet

- Howe Engineering Projects India PVT LTD: Earnings Amount Deductions Amount Perks/Other income/Exempton/RebatesDocument1 pageHowe Engineering Projects India PVT LTD: Earnings Amount Deductions Amount Perks/Other income/Exempton/RebatesSumantrra ChattopadhyayNo ratings yet

- Payroll TemplateDocument26 pagesPayroll TemplateAngita RaghuwanshiNo ratings yet

- Calculation of Tariffs, Taxes and FeesDocument2 pagesCalculation of Tariffs, Taxes and FeesElaNo ratings yet

- Course Syllabus AE26 - Income TaxationDocument3 pagesCourse Syllabus AE26 - Income Taxationgly escobarNo ratings yet

- The 400 Individual Income Tax Returns Reporting The Highest Adjusted Gross Incomes Each Year, 1992-2008Document13 pagesThe 400 Individual Income Tax Returns Reporting The Highest Adjusted Gross Incomes Each Year, 1992-2008GestaltUNo ratings yet

- BIR Activities and Revenue RegulationsDocument3 pagesBIR Activities and Revenue RegulationsJoshua Cabinas100% (1)

- ITR-1 Acknowledgement for AY 2022-23Document1 pageITR-1 Acknowledgement for AY 2022-23AEN TRACKNo ratings yet

- Government Pay SlipDocument1 pageGovernment Pay SlipBidhya DahalNo ratings yet

- Refer To The Data For Rijo Equipment Repair Corp inDocument2 pagesRefer To The Data For Rijo Equipment Repair Corp inMiroslav Gegoski0% (1)