You might also like

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Equity Valuation ModelsDocument58 pagesEquity Valuation ModelsSarang GuptaNo ratings yet

- Share Valuation Session 11: John Burr Williams and the Dividend Discount ModelDocument52 pagesShare Valuation Session 11: John Burr Williams and the Dividend Discount ModelMinato UzumakiNo ratings yet

- Valuation of Long-Term SecuritiesDocument5 pagesValuation of Long-Term SecuritiesUsman FazalNo ratings yet

- Valuation MethodsDocument25 pagesValuation MethodsAd QasimNo ratings yet

- Equity ValuationDocument45 pagesEquity Valuationbiplav2uNo ratings yet

- Valuation Concepts & ModelsDocument18 pagesValuation Concepts & Modelssmwanginet7No ratings yet

- NISM CH 10Document13 pagesNISM CH 10Darshan JainNo ratings yet

- Market Value Per Share Earning Per Share (EPS)Document7 pagesMarket Value Per Share Earning Per Share (EPS)AmenahNo ratings yet

- 04 The Value of Common StockDocument27 pages04 The Value of Common Stockmelekkbass10No ratings yet

- Equity Valuation Explained: Why Determine a Stock's Intrinsic ValueDocument12 pagesEquity Valuation Explained: Why Determine a Stock's Intrinsic ValueRUKUDZO KNOWLEDGE DAWANo ratings yet

- STOCK VALUE CALCULATION: BOOK, MARKET, INTRINSICDocument20 pagesSTOCK VALUE CALCULATION: BOOK, MARKET, INTRINSICEfi Setia NingsihNo ratings yet

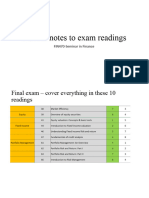

- Sem in Finance-Notes To Final Exam Readings Part 2Document82 pagesSem in Finance-Notes To Final Exam Readings Part 2hantrankha75No ratings yet

- Security Analysis and Portfolio ManagementDocument61 pagesSecurity Analysis and Portfolio ManagementpjNo ratings yet

- Equities: Understanding Common and Preferred StockDocument41 pagesEquities: Understanding Common and Preferred StockPamula SindhuNo ratings yet

- Valuation of Financial AssetDocument55 pagesValuation of Financial Assetkate trishaNo ratings yet

- Relative ValuationDocument29 pagesRelative ValuationOnal RautNo ratings yet

- Valuing Shares: Methods and ModelsDocument20 pagesValuing Shares: Methods and ModelsLim Yu ChengNo ratings yet

- Top-Down Valuation ApproachesDocument118 pagesTop-Down Valuation ApproachesseptaritaNo ratings yet

- 202003291623595167nimisha THE COST OF CAPITALDocument28 pages202003291623595167nimisha THE COST OF CAPITALAkshay sachanNo ratings yet

- Valuation of Mergers and AcquisitionsDocument41 pagesValuation of Mergers and Acquisitionscrazybobby007No ratings yet

- Value: Financial Terms Related To ValueDocument18 pagesValue: Financial Terms Related To ValueGustavoNo ratings yet

- Equity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaDocument51 pagesEquity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaSheeza AshrafNo ratings yet

- Discounted Dividend Model ValuationDocument36 pagesDiscounted Dividend Model ValuationKomal GuptaNo ratings yet

- Cost of Capital AnalysisDocument10 pagesCost of Capital AnalysisnanidoppiNo ratings yet

- Equity Valuation ModelsDocument37 pagesEquity Valuation ModelsDisha BakshiNo ratings yet

- Relative Valuation TechniquesDocument20 pagesRelative Valuation TechniquesmazazNo ratings yet

- Lecture-20 Equity ValuationDocument10 pagesLecture-20 Equity ValuationSumit Kumar GuptaNo ratings yet

- Dcf ValuationDocument74 pagesDcf ValuationCarrots TopNo ratings yet

- BM410-16 Equity Valuation 2 - Intrinsic Value 19oct05Document35 pagesBM410-16 Equity Valuation 2 - Intrinsic Value 19oct05muhammadanasmustafaNo ratings yet

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument122 pagesInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownWhy you want to knowNo ratings yet

- Investment-Ch 3Document18 pagesInvestment-Ch 3bereket nigussieNo ratings yet

- Session 10Document41 pagesSession 10Hammad KamranNo ratings yet

- An Introduction To Equity ValuationDocument37 pagesAn Introduction To Equity ValuationAamir Hamza MehediNo ratings yet

- Common Stock Valuation PDFDocument45 pagesCommon Stock Valuation PDFvignespoonganNo ratings yet

- Chp 11 Discounted Dividend ValuationDocument58 pagesChp 11 Discounted Dividend ValuationChriselle D'souzaNo ratings yet

- The Equity Cost of CapitalDocument9 pagesThe Equity Cost of CapitalMariam AlraeesiNo ratings yet

- Valuation AnalysisDocument86 pagesValuation Analysisollllllllllo100% (1)

- Investment and Portfolio Management: ACFN 3201Document16 pagesInvestment and Portfolio Management: ACFN 3201Bantamkak FikaduNo ratings yet

- Equity Valuation Using DDM and FCF MethodsDocument35 pagesEquity Valuation Using DDM and FCF Methodsts wNo ratings yet

- Valuing Residual Cash FlowDocument43 pagesValuing Residual Cash FlowEssue KediaNo ratings yet

- Merrill Lynch 2007 Analyst Valuation TrainingDocument74 pagesMerrill Lynch 2007 Analyst Valuation Trainingmehtarahul999No ratings yet

- Relative ValuationDocument29 pagesRelative ValuationCheTanBonDardeNo ratings yet

- Selection of Stocks Fundamental and Technical AnalysisDocument52 pagesSelection of Stocks Fundamental and Technical AnalysisKartikyaNo ratings yet

- KShare Dividends V001Document24 pagesKShare Dividends V001Krisha ShahNo ratings yet

- Corporate Finance II. - First Mid-Term: 1 Valuation ApproachesDocument4 pagesCorporate Finance II. - First Mid-Term: 1 Valuation ApproachesMarika KovácsNo ratings yet

- Finance BECDocument8 pagesFinance BECJon LeinsNo ratings yet

- 04 the Value of Common StocksDocument10 pages04 the Value of Common Stocksddrechsler9No ratings yet

- Valuation models and intrinsic value analysisDocument10 pagesValuation models and intrinsic value analysisImran AnsariNo ratings yet

- Introduction to Valuing Securities with DCF and Relative ModelsDocument94 pagesIntroduction to Valuing Securities with DCF and Relative ModelsRaiHan AbeDinNo ratings yet

- Financial Management 9Document23 pagesFinancial Management 9charithNo ratings yet

- BE300 Lecture 5Document31 pagesBE300 Lecture 5Rafan AhmedNo ratings yet

- Presented By: Muhammad Taimoor Baig Uzair-ul-Atiq Kashif Bashir Salman Zafar Syed Ali RazaDocument40 pagesPresented By: Muhammad Taimoor Baig Uzair-ul-Atiq Kashif Bashir Salman Zafar Syed Ali RazaSalman ZafarNo ratings yet

- Equity Valuation ModelsDocument37 pagesEquity Valuation Modelskarthik chamarthyNo ratings yet

- Stock Valuation: Legal Rights and Privileges of Common StockholdersDocument5 pagesStock Valuation: Legal Rights and Privileges of Common Stockholderssincere sincereNo ratings yet

- Equity ValuationDocument36 pagesEquity ValuationANo ratings yet

- Chapter 7: Valuing Company StockDocument36 pagesChapter 7: Valuing Company StockLinh MaiNo ratings yet

- Topic 6 WACCDocument43 pagesTopic 6 WACCsimfukwepascal812No ratings yet

- Equity Valuations & CAPMDocument5 pagesEquity Valuations & CAPMRikardasNo ratings yet

- Corporate ValuationsDocument140 pagesCorporate ValuationsAadesh ShahNo ratings yet

- Marine InsuranceDocument6 pagesMarine InsuranceJack SparrowNo ratings yet

- Climax New 123Document44 pagesClimax New 123Jack SparrowNo ratings yet

- Group 12Document25 pagesGroup 12Jack SparrowNo ratings yet

- Harley Davidson Internationalisation in The Trump EraDocument9 pagesHarley Davidson Internationalisation in The Trump EraJack SparrowNo ratings yet

- In The Double Taxation Avoidance Agreement (DTAA) Between India and IsraelDocument1 pageIn The Double Taxation Avoidance Agreement (DTAA) Between India and IsraelJack SparrowNo ratings yet

- 9th AICC Brochure - V1.10Document9 pages9th AICC Brochure - V1.10Jack SparrowNo ratings yet

- GHGDCBDocument34 pagesGHGDCBAnish Veeru AnandNo ratings yet

- Manvendra Singh International Marketing AssignmentDocument7 pagesManvendra Singh International Marketing AssignmentJack SparrowNo ratings yet

- SBI PO Notification 2021: 2056 Vacancies, Apply OnlineDocument6 pagesSBI PO Notification 2021: 2056 Vacancies, Apply OnlineRajesh K KumarNo ratings yet

- Shortlist Letter XAT22069140Document1 pageShortlist Letter XAT22069140Jack SparrowNo ratings yet

- Cut-Offs For Different Programs of Xlri Based On Xat-2022Document1 pageCut-Offs For Different Programs of Xlri Based On Xat-2022Jack SparrowNo ratings yet

- March 2021 Financial Accounting and Reporting UK GAAPDocument10 pagesMarch 2021 Financial Accounting and Reporting UK GAAPChoo LeeNo ratings yet

- Assignment Dissolution NEWERDocument3 pagesAssignment Dissolution NEWERsakshamagnihotri0No ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- Solution_to_Ch14_P13_Build_a_ModelDocument6 pagesSolution_to_Ch14_P13_Build_a_ModelALI HAIDERNo ratings yet

- Intacc Finals Sw&QuizzesDocument57 pagesIntacc Finals Sw&QuizzesIris FenelleNo ratings yet

- Cost of Goods ManufacturedDocument26 pagesCost of Goods ManufacturedAb.Rahman AfghanNo ratings yet

- CACMA Inter Class Notes NovDec 21Document890 pagesCACMA Inter Class Notes NovDec 21bharathreddykatta13No ratings yet

- F7 - QuestionsDocument10 pagesF7 - QuestionspavishneNo ratings yet

- Assignmentkarla Company Provided The Following Information For 2016 PDF FreeDocument1 pageAssignmentkarla Company Provided The Following Information For 2016 PDF FreePatrisha Carpio BeleyNo ratings yet

- Cash FlowsDocument51 pagesCash FlowsFabrienne Kate Eugenio Liberato100% (1)

- Statement of Cash Flows ChapterDocument2 pagesStatement of Cash Flows ChapterNicole TeruelNo ratings yet

- Detecting Financial Statement Fraud Using Beneish ModelDocument4 pagesDetecting Financial Statement Fraud Using Beneish ModelGeo JNo ratings yet

- Cash and Accrual BasisDocument3 pagesCash and Accrual Basisattiva jade100% (1)

- Hempstead Realty - Balance SheetDocument3 pagesHempstead Realty - Balance SheetArvin Operania TolentinoNo ratings yet

- Other Comprehensive IncomeDocument11 pagesOther Comprehensive IncomeJoyce Ann Agdippa BarcelonaNo ratings yet

- The Accounting Cycle Accruals and DeferralsDocument17 pagesThe Accounting Cycle Accruals and DeferralsDikky ZulfikarNo ratings yet

- Mahindra and Mahindra LTD Financial AnalysisDocument21 pagesMahindra and Mahindra LTD Financial AnalysisAyan SahaNo ratings yet

- Fs ExerciseDocument6 pagesFs ExerciseDIVINE GRACE ROSALESNo ratings yet

- Annual Report Non-Profit making Organizations (AR NPODocument15 pagesAnnual Report Non-Profit making Organizations (AR NPOSibaprasad DashNo ratings yet

- Business Combi TsetDocument28 pagesBusiness Combi Tsetsamuel debebeNo ratings yet

- Ast Chapter 1 MCPDocument14 pagesAst Chapter 1 MCPElleNo ratings yet

- Download ebook Financial Accounting Ii Paperback Hanif Mukherjee Pdf full chapter pdfDocument67 pagesDownload ebook Financial Accounting Ii Paperback Hanif Mukherjee Pdf full chapter pdfjulie.morrill858100% (26)

- Special Journals-Perpetual Method X WorksheetDocument11 pagesSpecial Journals-Perpetual Method X WorksheetJasmine ActaNo ratings yet

- Intro CH 4 Theory of Production and CostDocument53 pagesIntro CH 4 Theory of Production and CostEllii YouTube channelNo ratings yet

- Case 50Document13 pagesCase 50Blatta OrientalisNo ratings yet

- Chapter One: Challenge Exercise 1Document3 pagesChapter One: Challenge Exercise 1Jean Korsini Angeline Klau0% (1)

- Notes on Financial Statement Line ItemsDocument5 pagesNotes on Financial Statement Line ItemsJasmine Cruz SalvaniNo ratings yet

- Financial Section of Business PlanDocument3 pagesFinancial Section of Business PlanFLORAH WAITHERA WANJOHINo ratings yet

- Financial Accounting and Reporting-IDocument7 pagesFinancial Accounting and Reporting-IWasim SajadNo ratings yet

- Icaew Cfab Mi 2018 Sample Exam 3Document30 pagesIcaew Cfab Mi 2018 Sample Exam 3Anonymous ulFku1v100% (2)