You might also like

- Case Time Value of MoneyDocument7 pagesCase Time Value of MoneyHasibul Islam80% (5)

- Answer Key To QuizzersDocument52 pagesAnswer Key To QuizzersQueen ValleNo ratings yet

- SAUDI ARABIAN SAIPEM CO REPAIR CONTRACTDocument8 pagesSAUDI ARABIAN SAIPEM CO REPAIR CONTRACTAbu UmarNo ratings yet

- Time Value of MoneyDocument21 pagesTime Value of MoneyNikhil PatilNo ratings yet

- Finance Chpter 5 Time Value of MoneyDocument11 pagesFinance Chpter 5 Time Value of MoneyOmar Ahmed ElkhalilNo ratings yet

- 3 Simple Annuity With Prob Solving Practice SetDocument34 pages3 Simple Annuity With Prob Solving Practice SetSheila Mae BautistaNo ratings yet

- TVM & CompoundingDocument8 pagesTVM & CompoundingUday BansalNo ratings yet

- Fin440 Chapter 6 v.2Document51 pagesFin440 Chapter 6 v.2Lutfun Nesa AyshaNo ratings yet

- Lecture9 - ES301 Engineering EconomicsDocument19 pagesLecture9 - ES301 Engineering EconomicsLory Liza Bulay-ogNo ratings yet

- Module 3 Math1 Ge3Document10 pagesModule 3 Math1 Ge3orogrichchelynNo ratings yet

- Civil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InterestDocument14 pagesCivil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InteresttayyabNo ratings yet

- Calculating Present and Future ValuesDocument17 pagesCalculating Present and Future Valuesየሞላ ልጅNo ratings yet

- Annuitie S: Liuren WuDocument39 pagesAnnuitie S: Liuren Wusaikumar selaNo ratings yet

- 03a 1Document5 pages03a 1ravi.gullapalliNo ratings yet

- 1349 1Document6 pages1349 1Noaman AkbarNo ratings yet

- EEE 452: Engineering Economics and Management: - Lec 9: Time Value of MoneyDocument28 pagesEEE 452: Engineering Economics and Management: - Lec 9: Time Value of MoneyTomas KhanNo ratings yet

- The Time Value of Money: Topic 3Document35 pagesThe Time Value of Money: Topic 3lazycat1703No ratings yet

- CHAPTER 6 Module Financial ManagementDocument23 pagesCHAPTER 6 Module Financial Managementgiezel francoNo ratings yet

- Time Value OfmoneyDocument23 pagesTime Value OfmoneyJason DurdenNo ratings yet

- Simple and Compound InterestDocument8 pagesSimple and Compound InterestMari Carreon TulioNo ratings yet

- The Mathematics of Finance Chapter 6 GuideDocument55 pagesThe Mathematics of Finance Chapter 6 GuideGil John Awisen100% (1)

- FA-I CHAPTER FIVE@editedDocument23 pagesFA-I CHAPTER FIVE@editedHussen AbdulkadirNo ratings yet

- Corporate Finance 1a Time Value for MoneyDocument16 pagesCorporate Finance 1a Time Value for MoneyKIMBERLY MUKAMBANo ratings yet

- Time Value of Money - MbaDocument36 pagesTime Value of Money - MbaFranchezka PegolloNo ratings yet

- Department cost allocationDocument6 pagesDepartment cost allocationmedhane negaNo ratings yet

- Emergency Fund-TVMDocument33 pagesEmergency Fund-TVMDeina ChiaroNo ratings yet

- An Hoài Thu - CHAPTER 5+6 - FIN202Document19 pagesAn Hoài Thu - CHAPTER 5+6 - FIN202An Hoài ThuNo ratings yet

- Itech Tutoring Comm 308 BookletDocument117 pagesItech Tutoring Comm 308 BookletAytekin AkolNo ratings yet

- Notes For Long Term Exam 2 FinanceDocument41 pagesNotes For Long Term Exam 2 FinancemartinNo ratings yet

- GR12 Business Finance Module 9-10Document7 pagesGR12 Business Finance Module 9-10Jean Diane JoveloNo ratings yet

- 7.-SLM Bus - Math Q1 W9Document11 pages7.-SLM Bus - Math Q1 W9Sir AronNo ratings yet

- Chapter6 Matematika BusinessDocument17 pagesChapter6 Matematika BusinessKarlina DewiNo ratings yet

- FinMan Module 5 Time Value of Money - Part 2Document13 pagesFinMan Module 5 Time Value of Money - Part 2erickson hernanNo ratings yet

- LONG TERM INVESTMENT DECISIONS: TIME VALUE OF MONEY (TVM) REPORTDocument7 pagesLONG TERM INVESTMENT DECISIONS: TIME VALUE OF MONEY (TVM) REPORTMary Ann MarianoNo ratings yet

- FNCE 220: Understanding the Time Value of MoneyDocument18 pagesFNCE 220: Understanding the Time Value of MoneyVincent KamemiaNo ratings yet

- Draft Jawapan Cases (Managerial Finance) Set9 Sem2 Sesi20222023 Bangi - YdDocument10 pagesDraft Jawapan Cases (Managerial Finance) Set9 Sem2 Sesi20222023 Bangi - YdAhmad SuffianNo ratings yet

- MODULE #2 Topic 1Document13 pagesMODULE #2 Topic 1Alen Genesis CoronelNo ratings yet

- RWJ Chapter 4Document52 pagesRWJ Chapter 4Parth ParthNo ratings yet

- Finman Modules Chapter 5Document9 pagesFinman Modules Chapter 5Angel ColarteNo ratings yet

- Microsoft Word - Week 6 Bonds Version - 1 Solution 9th 04 2019Document6 pagesMicrosoft Word - Week 6 Bonds Version - 1 Solution 9th 04 2019Mark LiNo ratings yet

- Engineering Cost Analysis: Charles V. Higbee Geo-Heat Center Klamath Falls, OR 97601Document48 pagesEngineering Cost Analysis: Charles V. Higbee Geo-Heat Center Klamath Falls, OR 97601Kwaku SoloNo ratings yet

- Lecture Time Value of MoneyDocument44 pagesLecture Time Value of MoneyAdina MaricaNo ratings yet

- Answer FIN 401 Exam2 Fall15 V1Document7 pagesAnswer FIN 401 Exam2 Fall15 V1mahmudNo ratings yet

- Tugas Manajemen Keuangan (Maulana Ikhsan Tarigan) 197007091Document5 pagesTugas Manajemen Keuangan (Maulana Ikhsan Tarigan) 197007091Maulana IkhsanNo ratings yet

- General Mathematics: LAS, Week 1 - Quarter 2Document16 pagesGeneral Mathematics: LAS, Week 1 - Quarter 2Prince Joshua SumagitNo ratings yet

- MMW Lesson 8Document10 pagesMMW Lesson 8Denver SaulonNo ratings yet

- Wednesday WK 2Document35 pagesWednesday WK 2Smriti LalNo ratings yet

- Group 6.time Value of Money and Risk and Return - FinMan FacilitationDocument95 pagesGroup 6.time Value of Money and Risk and Return - FinMan FacilitationNaia SNo ratings yet

- Finance Chapter4 AnswersDocument4 pagesFinance Chapter4 AnswersyumnaNo ratings yet

- MalaDocument5 pagesMalaAruna MadasamyNo ratings yet

- Business Finance Q3 Module 6 2Document23 pagesBusiness Finance Q3 Module 6 2krystelairaa14No ratings yet

- FIN 242 Chapter 10 (Mathematic of Finance)Document24 pagesFIN 242 Chapter 10 (Mathematic of Finance)MUHAMMAD FAUZAN ABU BAKARNo ratings yet

- AnnuityDocument6 pagesAnnuityGokul NathNo ratings yet

- Time Value of Money ExplainedDocument17 pagesTime Value of Money ExplainedShantam RajanNo ratings yet

- ACCT1002 M3 Homework SolutionsDocument7 pagesACCT1002 M3 Homework SolutionsMadeline WheelerNo ratings yet

- General Quarter 2 - Week 2: ZZZZZZDocument14 pagesGeneral Quarter 2 - Week 2: ZZZZZZJakim LopezNo ratings yet

- CHAPTER 6 Module Financial ManagementDocument20 pagesCHAPTER 6 Module Financial ManagementAdoree RamosNo ratings yet

- Annuity GuideDocument68 pagesAnnuity Guidenimra khaliqNo ratings yet

- Time Value of Money Chapter Explains Financial Concepts Like Present and Future ValueDocument38 pagesTime Value of Money Chapter Explains Financial Concepts Like Present and Future ValueLaiba KhanNo ratings yet

- Topic 3 ValuationDocument44 pagesTopic 3 Valuationbrianmfula2021No ratings yet

- Business Math: Calculating Mortgage InterestDocument8 pagesBusiness Math: Calculating Mortgage InterestLillibeth LumibaoNo ratings yet

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyFrom EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNo ratings yet

- Bret Broaddus Tips To Avoid Mistakes That Home Buyers MakeDocument3 pagesBret Broaddus Tips To Avoid Mistakes That Home Buyers MakeBret broaddusNo ratings yet

- AssignmentDocument5 pagesAssignmentMELAKU ADIMASNo ratings yet

- Fortune Com Fortune 500 Full List 1 100 TomDocument4 pagesFortune Com Fortune 500 Full List 1 100 TomVikas RNo ratings yet

- Outline - Agency & PartnershipDocument19 pagesOutline - Agency & PartnershipSaulNo ratings yet

- Digital Covid Questionnaire For Revival Approval FormatDocument2 pagesDigital Covid Questionnaire For Revival Approval Formatsouravdey3No ratings yet

- Insurance BrokersDocument4 pagesInsurance Brokersashish srivastavaNo ratings yet

- White Gold Marine Services, Inc., vs. Pioneer Insurance and Surety Corporation PDFDocument7 pagesWhite Gold Marine Services, Inc., vs. Pioneer Insurance and Surety Corporation PDFFatima TumbaliNo ratings yet

- Statement Feb 21 XXXXXXXX0851Document2 pagesStatement Feb 21 XXXXXXXX0851Robert B. WeideNo ratings yet

- How Insurance Drives Economic Growth: June 2018Document18 pagesHow Insurance Drives Economic Growth: June 2018Hamza AbidNo ratings yet

- Nyse FFG 2002Document114 pagesNyse FFG 2002Bijoy AhmedNo ratings yet

- Find Unclaimed Money and Assets GuideDocument12 pagesFind Unclaimed Money and Assets GuidePaul Zachariah GiovanniNo ratings yet

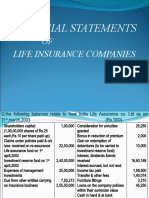

- Accounting For Insurance CompaniesDocument34 pagesAccounting For Insurance CompaniesD MNo ratings yet

- A Study On The Role of Bajaj Finserv in Consumer Durable FinanceeDocument58 pagesA Study On The Role of Bajaj Finserv in Consumer Durable FinanceeSanjeeb DuttaNo ratings yet

- Petitioner Respondent: Susan Co Dela Fuente, - Fortune Life Insurance Co., Inc.Document18 pagesPetitioner Respondent: Susan Co Dela Fuente, - Fortune Life Insurance Co., Inc.Christine Joyce SumawayNo ratings yet

- Challenges in Nursing Home CareDocument4 pagesChallenges in Nursing Home CareShaina FabitoNo ratings yet

- Pennsylvania Treasury - Bureau of Unclaimed PropertyDocument4 pagesPennsylvania Treasury - Bureau of Unclaimed PropertyJuliaNo ratings yet

- Insurance Products ENGDocument22 pagesInsurance Products ENGAndrej AndrejNo ratings yet

- Malayan vs. Phil. First Insurance (676 SCRA 268) (Digest)Document2 pagesMalayan vs. Phil. First Insurance (676 SCRA 268) (Digest)Michelle LimNo ratings yet

- 7 Most Important Principles of Insurance PDFDocument8 pages7 Most Important Principles of Insurance PDFMENGISTUNo ratings yet

- Certificate of Insurance ExampleDocument1 pageCertificate of Insurance ExampleAndrew MaasNo ratings yet

- THE MAGNA CARTA FOR PUBLIC SCHOOL TEACHERS Sec.3Document11 pagesTHE MAGNA CARTA FOR PUBLIC SCHOOL TEACHERS Sec.3Chiengkaii Gabas SanagaNo ratings yet

- Massachusetts General Power of Attorney FormDocument6 pagesMassachusetts General Power of Attorney FormarayNo ratings yet

- MBA1038 Banking & Insurance: Key ConceptsDocument3 pagesMBA1038 Banking & Insurance: Key ConceptsnanakethanNo ratings yet

- GPV Discount RatesDocument68 pagesGPV Discount Ratesmary iamNo ratings yet

- Elevation Design GuidlinesDocument124 pagesElevation Design Guidlinesarif khanNo ratings yet

- Certificate of Entry and Acceptance: "HC Jette-Marit"Document5 pagesCertificate of Entry and Acceptance: "HC Jette-Marit"WILLINTON HINOJOSANo ratings yet

- Doing Business With WillScotDocument7 pagesDoing Business With WillScotWilliamsNo ratings yet

- True/False Questions: Business Law & Ethics-Chapter 9bDocument2 pagesTrue/False Questions: Business Law & Ethics-Chapter 9bareejjooryNo ratings yet